Tax-Deferred Retirement-Saver Portfolios for T. Rowe Price Investors

It’s not the cheapest of the cheap, but it’s still possible to use the firm as a one-stop shop.

/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

T. Rowe Price is one of a fairly small handful of firms where one could reasonably stick exclusively with the “house brand” of funds. Although its US equity funds are the most widely recognized in the lineup, its international-equity and fixed-income offerings are solid. And while T. Rowe fund expenses aren’t Vanguard-low, most have Morningstar Fee Levels of Below Average or even Low.

This article highlights model T. Rowe Price portfolios for investors who are accumulating assets for retirement in tax-deferred accounts such as IRAs.

About the Portfolios

I’ve used Morningstar’s Lifetime Allocation Indexes to inform the portfolios’ asset allocations and the exposures to subasset classes. To populate the portfolios, I employed no-load, open mutual funds, most of which received Morningstar Medalist Ratings of Gold, Silver, or Bronze from Morningstar’s analyst team. The firm’s funds don’t rank as highly in a few core bond categories, so I had to settle for funds that earned Medalist Ratings of Neutral.

The portfolios are geared toward investors’ tax-sheltered accounts, so I didn’t consider the holdings’ tax efficiency when populating the portfolios.

How to Use Them

My key goal with these portfolios is to depict sound asset-allocation and portfolio-management principles rather than to shoot out the lights with performance. That means that investors can use them to help size up their own portfolios’ asset allocations and suballocations. Alternatively, investors can use the portfolios as a source of ideas in building out their own portfolios. As with the Bucket portfolios, I’ll employ a strategic (that is, long-term and hands-off) approach to asset allocation; I’ll make changes to the holdings only when individual holdings encounter fundamental problems or changes, or if they no longer earn Gold, Silver, or Bronze ratings.

The portfolios vary in their amounts of stock exposure and in turn their risk levels. The Aggressive portfolio is geared toward someone with many years until retirement and a high tolerance/capacity for short-term volatility. The Conservative portfolio is geared toward people who are just a few years shy of retirement. The Moderate portfolio falls between the two in terms of its risk/return potential.

Aggressive Tax-Deferred Retirement-Saver Portfolio for T. Rowe Price Investors

Anticipated Time Horizon to Retirement: 35-40 years

Risk Tolerance/Capacity: High

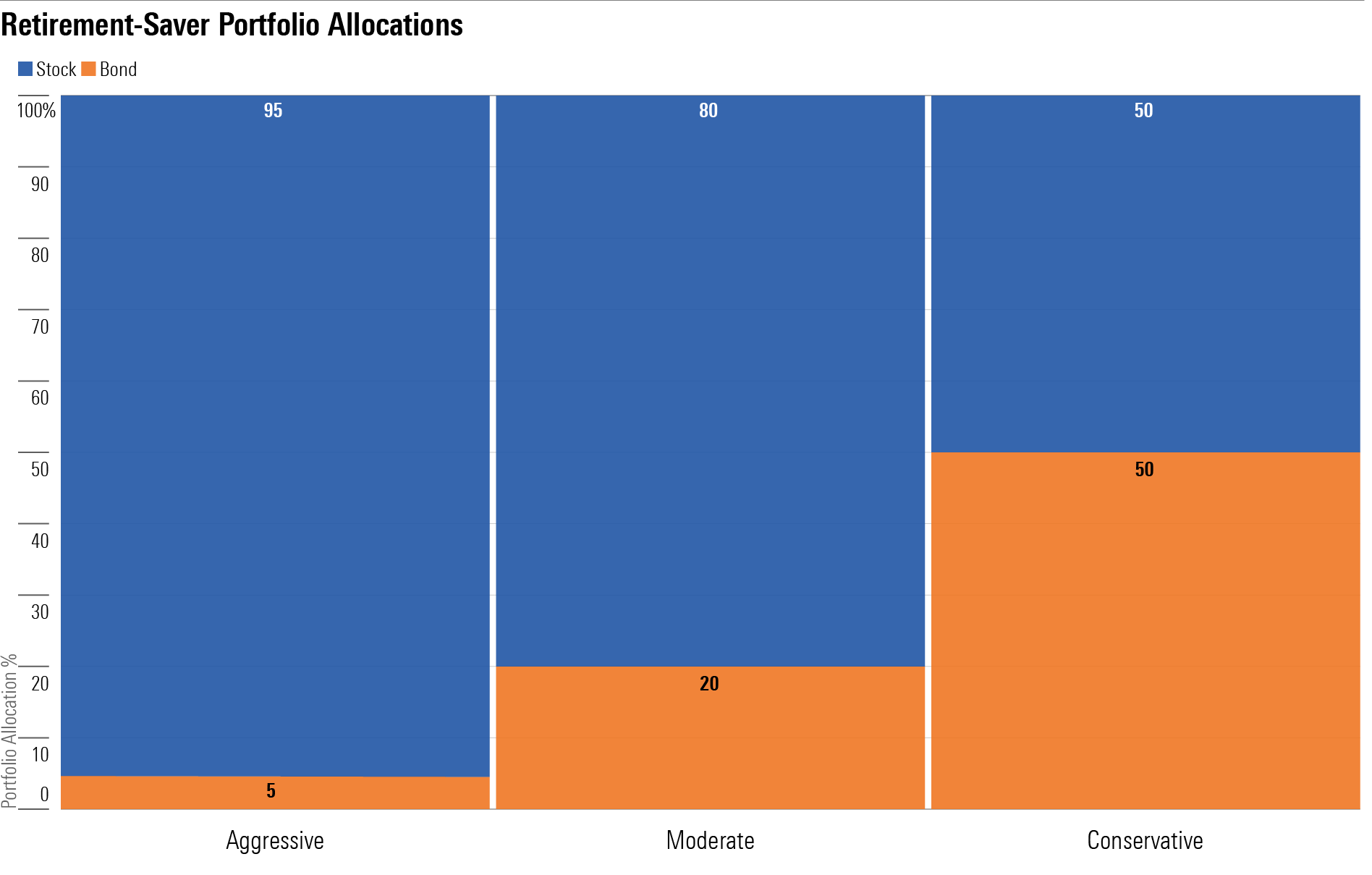

Target Stock/Bond Mix: 95/5

- 20%: T. Rowe Price Dividend Growth PRDGX

- 15%: T. Rowe Price Equity Index 500 PREIX

- 10%: T. Rowe Price All-Cap Opportunities PRWAX

- 10%: T. Rowe Price Small-Cap Value PRSVX

- 40%: T. Rowe Price Overseas Stock TROSX

- 5%: T. Rowe Price New Income PRCIX

Moderate Tax-Deferred Retirement-Saver Portfolio for T. Rowe Price Investors

Anticipated Time Horizon to Retirement: 20-25 years

Risk Tolerance/Capacity: Moderate

Target Stock/Bond Mix: 80/20

- 15%: T. Rowe Price Dividend Growth

- 15%: T. Rowe Price Equity Index 500

- 8%: T. Rowe Price All-Cap Opportunities

- 10%: T. Rowe Price Small-Cap Value

- 32%: T. Rowe Price Overseas Stock

- 20%: T. Rowe Price New Income

Conservative Tax-Deferred Retirement-Saver Portfolio for T. Rowe Price Investors

Anticipated Time Horizon to Retirement: 2-5 years

Risk Tolerance/Capacity: Low

Target Stock/Bond Mix: 50/50

- 15%: T. Rowe Price Dividend Growth

- 15%: T. Rowe Price Equity Index 500

- 5%: T. Rowe Price Small-Cap Value

- 15%: T. Rowe Price Overseas Stock

- 30%: T. Rowe Price New Income

- 10%: T. Rowe Price Short-Term Bond PRWBX

- 10%: T. Rowe Price Inflation-Protected Bond PRIPX

A version of this article was published on March 31, 2023.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZOMUI7V4LVD37GYFMSENZFH3GM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HCVXKY35QNVZ4AHAWI2N4JWONA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EC7LK4HAG4BRKAYRRDWZ2NF3TY.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)