There Is Nothing Special About Dividends

Why they’re not a tax-efficient way to return capital to shareholders.

/s3.amazonaws.com/arc-authors/morningstar/8c5d95ea-6364-418e-82fc-473134024ece.jpg)

In my role as head of financial and economic research at Buckingham Wealth Partners, I am often asked by investors about dividend growth strategies—strategies that are popular among retail investors who, for behavioral reasons, have been found to have a preference for dividends. I’ll review the financial theory about dividends and then the empirical evidence on the performance of dividend growth strategies.

A Dollar Is a Dollar

In their 1961 paper “Dividend Policy, Growth, and the Valuation of Shares,” Merton Miller and Franco Modigliani famously established that dividend policy should be irrelevant to stock returns. As they explained it, at least before frictions like trading costs and taxes, investors should be indifferent to $1 in the form of a dividend (causing the stock price to drop by $1) and $1 received by selling shares. This must be true, unless you believe that $1 isn’t worth $1. This theorem has not been challenged since.

Moreover, historical evidence supports this theory—stocks with the same exposure to common factors (such as size, value, momentum, and profitability/quality) have the same returns whether or not they pay a dividend. Yet, many investors ignore this information and express a preference for dividend-paying stocks.

Dividend Aristocrats

One popular dividend strategy is to invest in the “dividend aristocrats.” For example, the S&P 500 Dividend Aristocrats measures the performance of S&P 500 companies that have increased dividends for the last 25 consecutive years. And there is an exchange-traded fund based on that index, the ProShares S&P 500 Dividend Aristocrats NOBL. In a January 2019 blog post titled “Dividend Growth Strategies and Downside Protection,” S&P’s Phillip Brzenk, global head of multi-asset indexes, examined the performance of dividend growth strategies, specifically during periods of negative market performance. He found: “Since year-end 1989, there have been six calendar years of negative performance for the S&P 500—and in all six years, the S&P 500 Dividend Aristocrats outperformed the equity benchmark by an average of 13.28%. In fact, the S&P 500 Dividend Aristocrats produced a positive total return in three of those years.”

Examining the performance on a monthly basis, he found: “The S&P 500 Dividend Aristocrats outperformed the S&P 500 53% of the time, by an average of 0.16%. When isolated to down markets, the S&P 500 Dividend Aristocrats outperformed over 70% of the time and by an average of 1.13%. In up markets, the S&P 500 Dividend Aristocrats underperformed 56% of the time, but at a lower average magnitude (-0.34%). This shows that the S&P 500 Dividend Aristocrats has delivered downside protection in months when the S&P 500 lost ground.” Of course, markets tend to be up more than they are down, so an advantage in down markets doesn’t necessarily translate into an advantage overall.

Brzenk also found that “the lower the return of the S&P 500, the better the relative performance was for the S&P 500 Dividend Aristocrats. We see the batting average was typically better for the more negative months than the less negative months. Additionally, we observe that the average excess return over the S&P 500 was higher in the most negative months. Since 1989, the S&P 500 has lost 5% or more in 31 out of 348 months (~9% of the time). In these months, the average excess return for the S&P 500 Dividend Aristocrats was 2.46%, with a hit rate of 81%. The median excess return was of similar magnitude (2.32%); therefore, the results were not skewed by only a few months—rather, there was consistent outperformance.”

Is It Dividends or the Quality Factor?

The evidence seems to conflict with financial theory that says dividends don’t matter, which raises the question of whether a focus on dividend growth adds value, especially in down markets: Is there something unique about companies with growing dividends? Or can the returns of the stocks with growing dividends be explained by exposure to common factors that have been found to explain the vast majority of equity returns—market beta, size, value, momentum, and quality? In other words, do companies with the same exposure to these factors have the same performance whether or not they have growing dividends or even pay dividends at all?

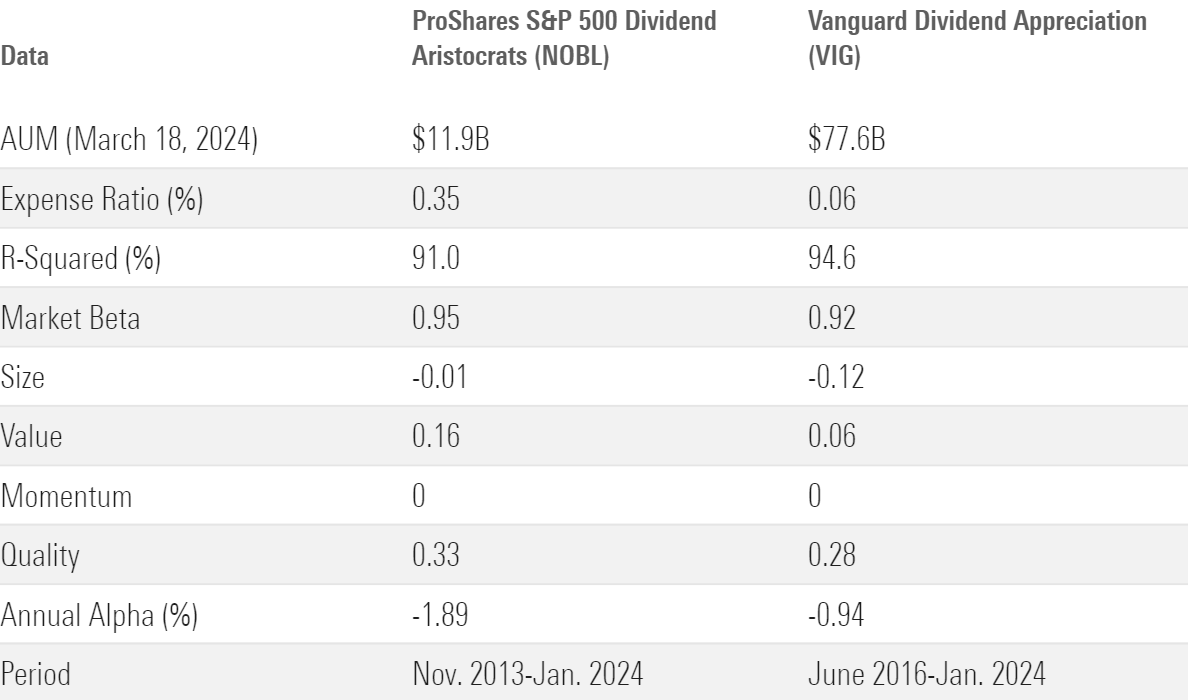

To answer the question, I’ll examine the performance of the two largest dividend-growth ETFs (with a total of more than $89 billion in assets) demonstrating that investors believe the strategy adds value. I used the regression tool available at Portfolio Visualizer. The table below shows the loadings (how much exposure the funds have to each factor) as well as the funds’ annual alpha.

Performance of Two Largest Dividend-Growth ETFs

What do we learn from the above data? First, the high R-squareds (especially in the case of Vanguard Dividend Appreciation VIG) demonstrate that the returns of the two funds are well explained by their exposure to these well-documented common factors. Second, some of the outperformance in down markets is explained by the fact that the market betas of the two funds are below 1—they have less exposure to market beta than the market does. Third, the funds also have negative exposure to the size factor—their holdings are larger than those of the market. And large stocks tend to outperform riskier small stocks in bear markets. Fourth, the two funds have large and highly statistically significant (t-stat of at least 5) exposure to the quality factor. Quality stocks are “defensive,” tending to outperform in down markets. And finally, and perhaps most importantly, the two ETFs both have economically significant negative alphas (negative 1.89% for NOBL and negative 0.94% for VIG), far greater than their expense ratios. That means the funds were subtracting value, not adding value.

The evidence is consistent with economic theory: There is nothing special about dividends, with the returns of dividend-paying stocks well explained by exposure to common factors. Dividends are neither positive nor negative, at least from a pretax perspective. For taxable investors, dividends have negative implications relative to share repurchases. In addition, a focus on dividends reduces diversification because about 60% of US stocks and about 40% of international stocks don’t pay dividends. Thus, any screen that includes dividends results in portfolios that are far less diversified than they would be if dividends were not included in the portfolio design. Less-diversified portfolios are less efficient because they have a higher potential dispersion of returns without any compensation in the form of higher expected returns (assuming the exposure to common factors is the same). And finally, a focus on dividends often leads to investing in US equities, creating a home-country bias and a less diversified portfolio.

The bottom line is that dividend-growth strategies are basically quality strategies. The good news about the quality factor is that the premium (about 4.8% a year since 1958) has been persistent and pervasive around the globe. However, there are no generally accepted, logical, risk-based explanations for the quality premium because quality stocks are, by definition, safer investments. And safer investments should have lower returns. Thus, the quality premium is a behavioral anomaly. And without a risk-based explanation, it’s possible that the premium could shrink or even disappear, especially because the premium has become well known since the publication of research such as the 2013 studies “Global Return Premiums on Earnings Quality, Value, and Size” and “Buffett’s Alpha.” The popularity of the strategy could cause the trade to be “crowded,” driving valuations higher and expected returns lower.

Investor Takeaways

First, there is nothing special about dividends except that they are a tax-inefficient way to return capital to shareholders, and they are certainly not income (except from a tax perspective); they are just a return of capital. Second, investors are better served by focusing on investing in strategies that provide exposure to the factors they want to invest in. A focus on dividends, whether dividend growth or high-dividend yield, is not likely to add value.

Larry Swedroe has authored or co-authored 20 books on investing. All opinions expressed are solely his opinions and do not reflect the opinions of Buckingham Strategic Wealth or its affiliates. This information is provided for general information purposes only and should not be construed as financial, tax or legal advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third-party information is deemed reliable, but its accuracy and completeness are not guaranteed. Mentions of specific securities are for informational purposes only. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy or adequacy of this article.

Larry Swedroe is a freelance writer. The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/URSWZ2VN4JCXXALUUYEFYMOBIE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CGEMAKSOGVCKBCSH32YM7X5FWI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/8c5d95ea-6364-418e-82fc-473134024ece.jpg)