Tax-Deferred Retirement-Bucket Portfolios for ETF Investors

These portfolio mixes are geared toward retirees with different time horizons and risk tolerances/capacities.

/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

Editor’s Note: A version of this article previously appeared on Jan. 4, 2024.

The Bucket approach to retirement portfolio planning isn’t designed to generate the best possible investment returns. It won’t—almost by definition. Instead, the Bucket strategy is geared toward real retirees, to help them source their needed cash flows regardless of what’s going on with their long-term holdings.

By maintaining an ongoing allocation to cash alongside a balanced portfolio, the Bucket approach enables retirees to withdraw funds from those liquid reserves when stock and/or bond values are in a trough. That allocation provides a psychological benefit, too, in that having cash on hand can help retirees cope with the volatility that will inevitably accompany their long-term holdings. In better market environments, retirees can source their cash flow needs from appreciated equity or bond holdings and not touch the cash.

These model portfolios are geared toward the tax-sheltered accounts, like IRAs, of people who are actively drawing upon their investments for a component of their living expenses.

About the Portfolios

These model portfolios are geared toward retired investors who are drawing upon their tax-sheltered accounts to meet a portion of their living expenses. Bucket 1 of each portfolio is to provide money for cash needs for a year or two, so we’re not taking any risks with it; investors can use some combination of certificates of deposit, high-yield savings accounts, or money market mutual funds for this portion of the portfolio. Bucket 2 covers another eight years’ worth of cash flow needs. It’s designed to deliver slightly more income than Bucket 1, as well as a dash of inflation protection and capital appreciation; thus, it consists mainly of high-quality short- and intermediate-term bonds. Bucket 3 is the growth engine of each of the portfolios, geared toward years 11 and beyond of retirement. Because of an anchor position in Vanguard Dividend Appreciation ETF VIG, which focuses on companies with a history of growing their dividends, the portfolio has a high-quality tilt that’s appropriate for a retirement portfolio.

The portfolios consist almost exclusively of exchange-traded funds that rate as Morningstar Medalists, meaning our analysts think they’re likely to outperform their peers over a full market cycle. I’ll make changes to the holdings only if their fundamentals change or they no longer rate as medalists.

How to Use Them

These portfolios are designed to help retirees and pre-retirees visualize what a long-term, strategic total-return portfolio would look like. Thus, a newly retired investor could follow the basic Bucket concept without completely upending existing favorite holdings.

Investors should take care to customize their portfolios to suit their own situations—risk tolerance and capacity, of course, but also planned spending. An investor’s own cash bucket, and in turn the allocations to the other two buckets, will depend on their portfolio spending rate. If an investor is using a lower starting withdrawal rate—say, 3% in the first years of retirement—Bucket 1 would accordingly be smaller (6% versus 8% in my Aggressive portfolio).

Aggressive Tax-Deferred Retirement-Bucket Portfolio for ETF Investors

Anticipated Time Horizon in Retirement: 25-plus years

Risk Tolerance/Capacity: High

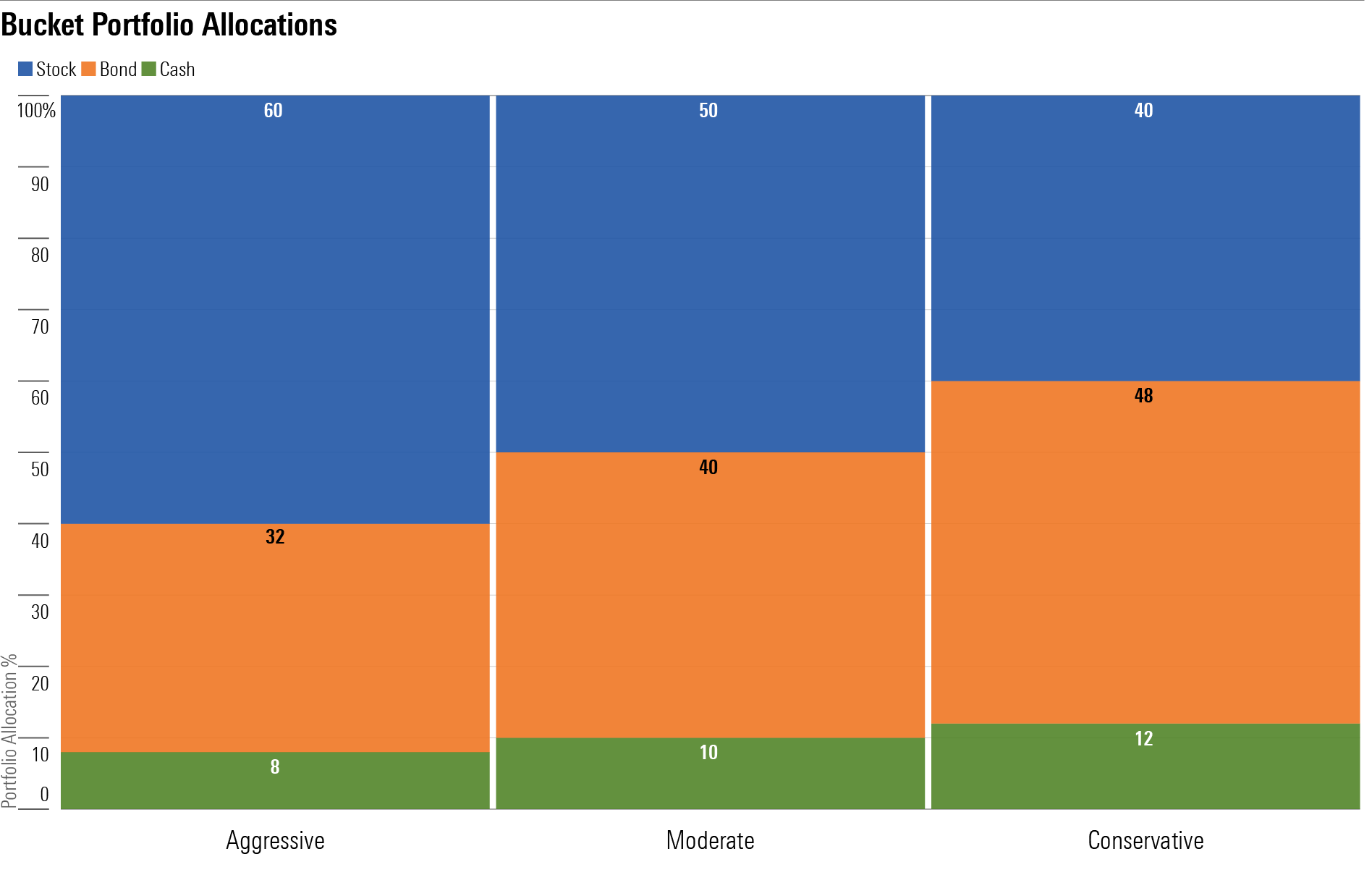

Target Stock/Bond/Cash Mix: 60/32/8

Bucket 1: Years 1-2

- 8%: Cash (certificates of deposit, money market accounts, and so on)

Bucket 2: Years 3-10

- 8%: Vanguard Short-Term Bond ETF BSV

- 7%: Vanguard Short-Term Inflation-Protected Securities ETF VTIP

- 10%: iShares Core Total USD Bond Market ETF IUSB

- 4%: Vanguard High-Yield Corporate VWEHX

- 3%: iShares J.P. Morgan USD Emerging Markets Bond ETF EMB

Bucket 3: Years 11 and Beyond

- 25%: Vanguard Dividend Appreciation ETF VIG

- 15%: Vanguard Total Stock Market ETF VTI

- 20%: Vanguard FTSE All-World ex-US ETF VEU

Moderate Tax-Deferred Retirement-Bucket Portfolio for ETF Investors

Anticipated Time Horizon in Retirement: 15–25 years

Risk Tolerance/Capacity: Moderate

Target Stock/Bond/Cash Mix: 50/40/10

Bucket 1: Years 1-2

- 10%: Cash (certificates of deposit, money market funds, and so on)

Bucket 2: Years 3-10

- 10%: Vanguard Short-Term Bond ETF BSV

- 10%: Vanguard Short-Term Inflation-Protected Securities ETF VTIP

- 12%: iShares Core Total USD Bond Market ETF IUSB

- 3%: Fidelity Floating Rate High Income FFRHX

- 2.5%: Vanguard High-Yield Corporate VWEHX

- 2.5%: iShares J.P. Morgan USD Emerging Markets Bond ETF EMB

Bucket 3: Years 11 and Beyond

- 20%: Vanguard Dividend Appreciation ETF VIG

- 15%: Vanguard Total Stock Market ETF VTI

- 15%: Vanguard FTSE All-World ex-US ETF VEU

Conservative Tax-Deferred Retirement-Bucket Portfolio for ETF Investors

Anticipated Time Horizon in Retirement: Less than 20 years

Risk Tolerance/Capacity: Low

Target Stock/Bond/Cash Mix: 40/48/12

Bucket 1: Years 1-2

- 12%: Cash (certificates of deposit, money market accounts, and so on)

Bucket 2: Years 3-10

- 10%: Vanguard Short-Term Bond ETF BSV

- 10%: Vanguard Short-Term Inflation-Protected Securities ETF VTIP

- 20%: iShares Core Total USD Bond Market ETF IUSB

- 3%: Fidelity Floating Rate High Income FFRHX

- 2.5%: Vanguard High-Yield Corporate VWEHX

- 2.5%: iShares J.P. Morgan USD Emerging Markets Bond ETF EMB

Bucket 3: Years 11 and Beyond

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZOMUI7V4LVD37GYFMSENZFH3GM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HCVXKY35QNVZ4AHAWI2N4JWONA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EC7LK4HAG4BRKAYRRDWZ2NF3TY.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)