Why Indexing Small-Growth Stocks Hasn't Worked

Bad luck is only half the reason.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

A Notable Exception

It’s an axiom of index investing that the practice uniformly succeeds, if given enough time. The belief is sound. For example, although emerging markets are commonly thought to be relatively inefficient, and thus fertile ground for active management, the MSCI Emerging Markets Index has outgained the average diversified emerging-markets stock fund over the past 15 years.

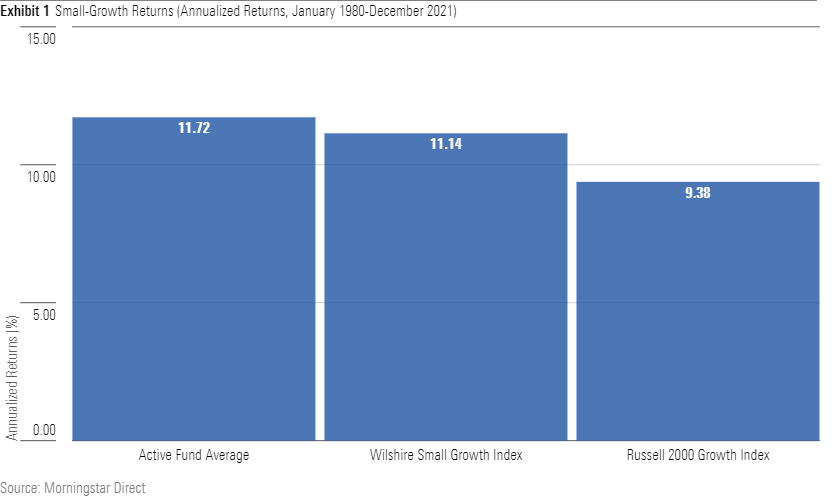

However, that claim has not held for U.S. small-growth stocks--at least not since Jimmy Carter’s presidency. For the 42 years from January 1980 through December 2021, the two small-growth indexes (from Russell and Wilshire) that have sufficiently long histories have trailed the average actively run small-growth fund.

This result is not affected by survivorship bias. Frequently, fund averages are overstated because they include only the funds that operated throughout the period, overlooking the deadbeats that perished along the way. This column’s calculation avoids that problem, as it uses monthly figures, which contain every small-growth fund that existed during those months. Thus, the chart accurately reflects shareholders’ experiences.

Style Impurity

Small-growth indexes have disappointed because small-growth companies have disappointed. This statement initially seems senseless. When discussing the relative performance of small-growth stocks, why bring up the rest of the stock market? However, in this instance, relative outcomes very much matter, because they highlight a key difference between indexes and active mutual funds: single-mindedness of purpose.

An index consists solely of securities that match its label. Every holding within the Wilshire U.S. Small Growth Total Market Index is a small-growth stock, as the company defines the term. If it were not, Wilshire would move it elsewhere. The same applies to other index providers. Their businesses depend upon delivering exactly what they declare. Should they stray from that promise, their customers will go elsewhere.

Mutual funds invest otherwise. Funds that are called “small growth” routinely invest in other styles, either because their managers fancy stocks that lie outside their funds’ putative boundaries, or because they retain positions that once fit the small-growth description but no longer qualify. Either way, actively run small-growth funds are less style-pure than their indexed competitors.

That impurity has helped active funds, as small-growth stocks were the lowest-returning sector of the U.S. stock market from 1980 through 2021. (Their risk-adjusted performance was even worse, as they also were the most volatile.) By diversifying outside their theoretical boundaries, small-growth fund managers were able to beat their benchmarks, even though their funds tended to be costly.

Considering the Reverse

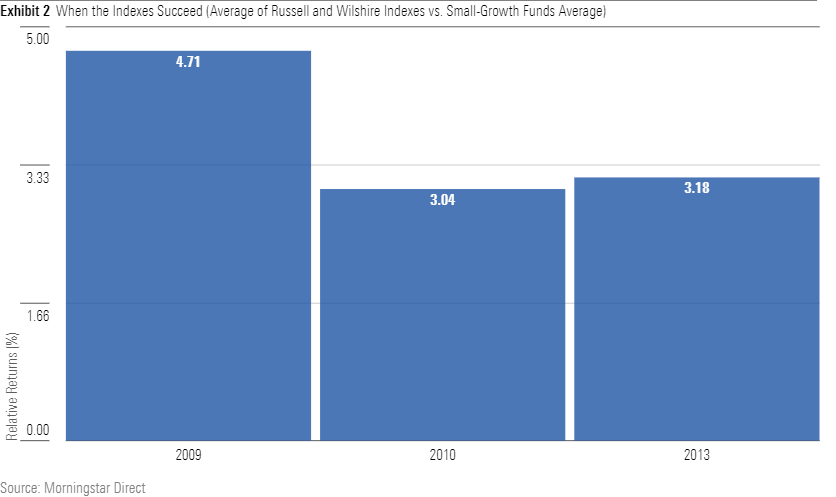

If small-growth stocks were to thrive, rather than flail, this condition would reverse. The next chart illustrates the point. It compares the average return of the two previously mentioned indexes (the Russell 2000 Growth and Wilshire U.S. Small-Cap Growth Total Market indexes) against that of active small-growth funds, during the three most recent years when small-growth was the top-performing corner of the Morningstar Style Box. A positive figure indicates that indexes bested the funds.

That they did. The indexes thrashed the active funds all three times. As each of those years was a bull market, the indexes benefited by being fully invested. But the cash drag cost funds only about 1.5 percentage points of return. The rest of index funds’ advantage owed to their style purity. When investing in the strongest section of the marketplace, diversification offers no benefit.

The moral of this story, therefore, is not that small-company growth indexing is intrinsically flawed. Had small-growth stocks posted the strongest post-1980 returns rather than than the weakest, small-company growth indexing would be celebrated. The sector was simply in the wrong place at the wrong time. Indexing usually wins--but not always. The strategy struggles to succeed when applied to the market’s laggards.

The Second Drawback

Regrettably, small-growth indexes suffer from more than mere bad luck. They have an additional problem that cannot be solved by a small-growth bull market: inconsistency. One large-blend index is very much like another; their returns rarely vary by more than a couple of percentage points. Not so with small-growth stock indexes. One is a terrier, another a golden retriever, a third a beagle. As a result, investing in a small-growth index is not easier than buying an active fund.

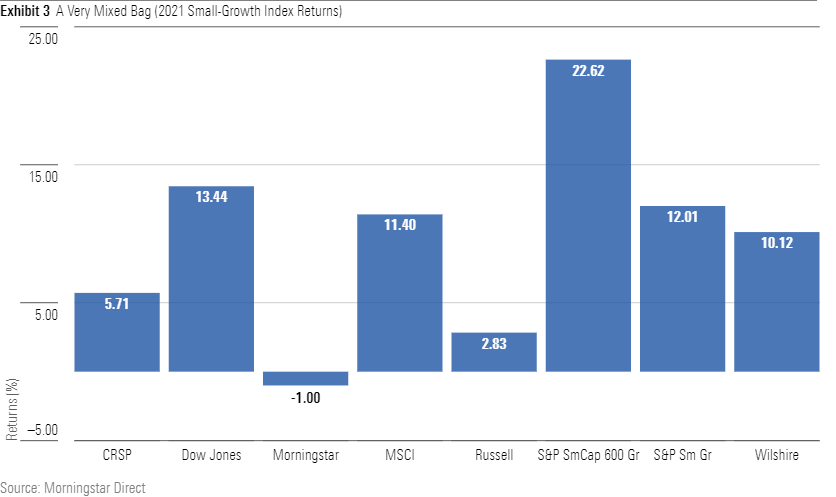

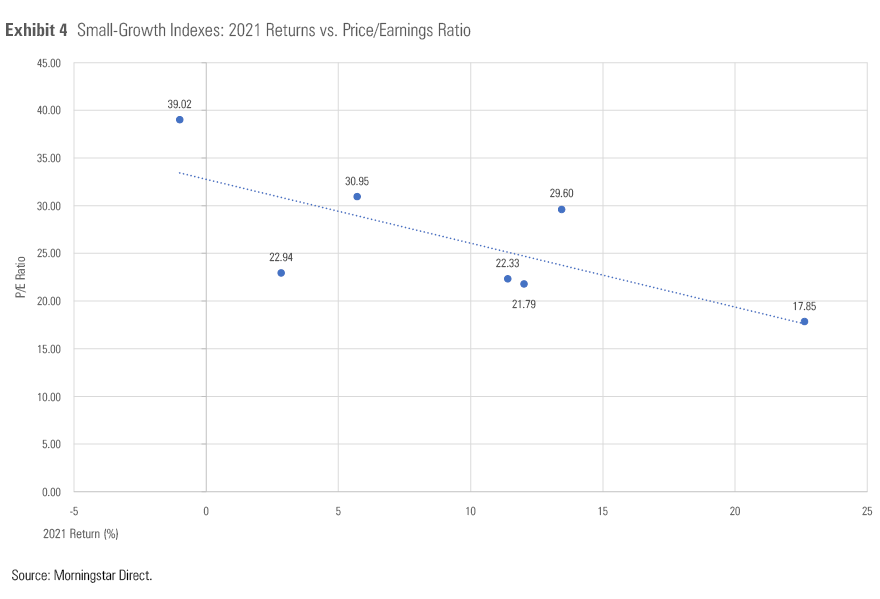

For example, consider the 2021 results for eight small-growth indexes. (The index field has expanded since 1980.) As shown in Exhibit 3, their returns span 23 percentage points, ranging from negative 1% for the Morningstar Small Growth Index--which had the highest gain among the group during the previous year--to almost 23% for the S&P SmallCap 600 Growth Index. Note that S&P offers two such indexes, and even they diverged by more than 10 percentage points.

Understanding why those indexes performed as they did requires a great deal of research. I devoted two hours to the task, with little to show for my efforts. In other words, investors in small-growth indexes are almost certainly flying blind. If their index fund were to sharply trail rival index funds--or, for that matter, the typical active fund--they are unlikely to know why. Nor can they be expected to discern why their fund succeeded, should it lead the index-fund rankings.

(That said, I did discover a link between 2021 small-growth index returns and the price/earnings ratios of those indexes, as measured when entering the year. That information isn’t directly relevant to this article, but as I spent time compiling the numbers, and the picture is rather elegant, I decided to show it anyway. Last year, the sun melted the wings of the highest fliers.)

Wrapping Up

Indexing small-growth stocks isn’t unwise. The reduced cost of index funds is always helpful, and if small-growth stocks improve their relative fortunes, so will small-growth indexing. Neither, though, should indexing be regarded as the clearly superior approach. Small-growth indexes vary so widely that choosing one involves either guesswork or substantial research--as with, for example, selecting an actively run fund.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MFL6LHZXFVFYFOAVQBMECBG6RM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HCVXKY35QNVZ4AHAWI2N4JWONA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EGA35LGTJFBVTDK3OCMQCHW7XQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

{kind=link}