The What, Why, and How of Quality

Quality may or may not stand on its own, but it seems to bring out the best in value stocks and small caps.

/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)

A version of this article was published in the February 2016 issue of Morningstar ETFInvestor. Download a complimentary copy of ETFInvestor here.

Quality may be the fuzziest factor you will find in the investing world. There is no one agreed-upon definition for it, nor is there clear consensus that it is a true stand-alone factor. What's more, it is missing the risk story, the basic economic intuition, and the readily discernible behavioral underpinnings that explain the existence and persistence of the value factor. Here, I'll address what quality is, why it may or may not yield superior risk-adjusted returns, and how investors can harness it with exchange-traded funds.

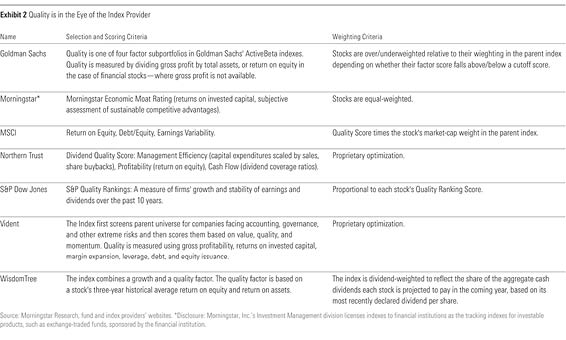

The What What is quality? The answer to this question will vary depending on who you ask. Common criteria that asset managers and index providers use to define quality stocks include measures of profitability (such as gross margins, return on equity, return on invested capital), stability (for example, earnings variability), growth (such as earnings growth or dividend growth), and financial health (for example, debt/equity ratios). Generally speaking, high-quality firms are consistently profitable, growing, and have solid balance sheets.

In their 2013 paper "Quality Minus Junk," [1] AQR's Cliff Asness, Andrea Frazzini, and Lasse Pedersen demonstrated that stocks meeting many of the criteria described above, and thus fitting the high-quality mold, produced significant risk-adjusted returns in the United States and 24 other global stock markets. The trio found that investors tend to pay premium prices for these high-quality firms. That said, they are not quite sure how to explain the returns to quality:

Our results present an important puzzle for asset pricing: We cannot tie the returns of quality to risk ... ... At this point the returns to quality must be either an anomaly, data mining (incredibly robust data mining--including across countries, size and time periods, and encompassing the strong consistent U.S. and global correlations of quality to size), or the results of a still-to-be-identified risk factor ...

So while we have a better-than-vague sense of what quality is, we are left with the very important question of why high-quality firms become mispriced to the extent that they can offer superior long-run returns.

The Why

"It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price." This sentence, taken from Warren Buffett's 1989 letter to

The importance of assessing the price paid for high-quality stocks cannot be understated. While quality matters, price arguably matters more. Vitali Kalesnik and Engin Kose of Research Affiliates provided a history lesson on this topic in their June 2014 research note, "The Moneyball of Quality Investing." [2] In it, they tell the tale of a once-storied group of high-quality stocks, the "Nifty Fifty":

In the late 1960s and early 1970s, institutional investors became enamored of 50 large, stable, fast-growing companies including such household names as General Electric, Xerox, Polaroid, and IBM. They were popularly called the Nifty Fifty. Because of their strong record of growth, valuation ratios seemed irrelevant; investors found them attractive at 50, 80, and even 100 times earnings. At the end of 1972, when the S&P 500 Index traded at a P/E of 20, the Nifty Fifty were trading at a P/E of 40. The popularity of the Nifty Fifty spurred a shift from value investing to a "growth at any price" paradigm. Sadly for many investors, company popularity did not translate into investment performance. The late 1960s and early 1970s were a period of remarkable growth in the U.S. economy. In 1973–1974, however, the S&P 500 fell by 39%, and the basket of Nifty Fifty stocks fell by 47%. The broad market regained confidence; around the end of 1976, the S&P 500 investors broke even with their initial 1973 investment. It took the Nifty Fifty investors nearly a decade to recoup their losses, and they never caught up with the broad market. Forty-one years later, the S&P 500 investors of 1973 would have earned about 23% more than the Nifty Fifty investors.

Asness and his co-authors also emphasize the importance of price in their work. Their QMJ factor is price-agnostic; it's based exclusively on non-price-related fundamental measures. The authors suggest that QMJ can be paired with the value factor, which is quality-agnostic, in a quality-at-a-reasonable-price, or QARP, strategy. In doing so, they find that controlling for quality actually enhances the value effect.

Kalesnik and Kose would agree with the QARP concept. They found that high-quality U.S. value stocks produced better risk-adjusted returns relative to low-quality U.S. value stocks from July 1963 through January 2014. However, the pair recommends a healthy degree of skepticism with regard to quality's status as a stand-alone factor. As they see it, the risk story just isn't there.

I'm not convinced that quality works in isolation. Price matters--perhaps more than anything else. I think quality is best thought of as an enhancer, an ingredient. Much as the value effect is more pronounced among small-cap stocks, I believe quality has the potential to amplify the gains from value. After all, buying good companies at good prices just makes sense.

(

)

The How

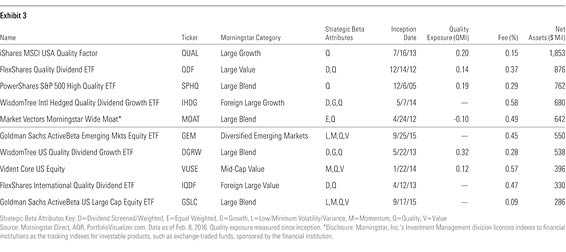

There are a slew of ETFs that either look to zero in on the quality factor or blend it into a combination of other factors. The table I've included shows the 10 largest ETFs that have quality criteria built into their benchmark indexes' methodology. Only two of the 10 funds I've included here look to isolate firms based exclusively on some measure of quality. The first is

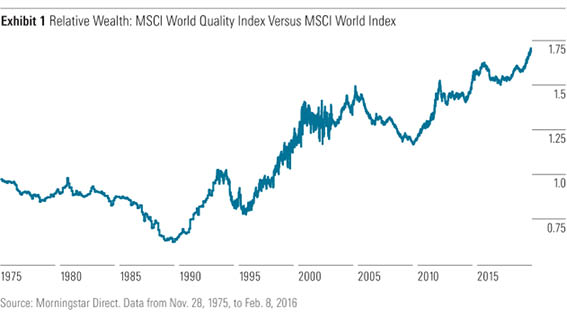

I'd suggest looking at a multifactor fund that adds quality to the mix. Blending quality with value, momentum, and other uncorrelated factors has the potential to smooth out the cyclicality associated with owning any single factor in isolation (see Exhibit 1 to get a sense of the feast/famine cycles that quality has experienced versus the broad stock market) and reduce the odds of self-defeating investor behavior.

(Click to see larger image)

[1] Asness, C. Frazzini, A., & Pedersen, L. 2014. "Quality Minus Junk." Working paper. [2] Kalesnik, V. & Kose, E. 2014. "The Moneyball of Quality Investing". Research Affiliates paper.

Disclosure: Morningstar, Inc.'s Investment Management division licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)