When Are Managed Portfolio Services Right for Your Clients?

Managed portfolio services have gotten cheaper by embracing passive approaches.

The cost of managed portfolio services continues to fall faster than that of mutual funds. Are the time savings and expertise for advisors worth the management fees?

With around 1,475 live portfolios in the Morningstar database, the sector offers advisors access to a wide range of offerings. In a new report, the Morningstar research team breaks down trends in portfolio composition, cost, and performance.

We cover the highlights here—download the UK Managed Portfolios Landscape report to read in full.

What Are Managed Portfolio Services?

On-platform managed portfolio services handle asset allocation, investment selection, and trade execution for wealth managers and advisors on behalf of their clients.

A managed portfolio is a collection of holdings, typically funds and ETFs, held in a client account and managed in line with a model. When the portfolio manager changes or rebalances the model, the investment platform executes the trades automatically.

Managed portfolio services are aimed at advised clients seeking portfolios suited to their attitude toward risk, but who don’t require a bespoke discretionary service.

UK Managed Portfolios—Breakdown by Global Category

Source: Morningstar Direct. Data as of Sept. 30, 2025.

Benefits of Managed Portfolios

Portfolio Management Expertise

Managed portfolio services allow wealth managers and advisors to offer asset allocation, investment selection, and trade execution to investors. By outsourcing portfolio management to investment professionals, advisors can dedicate more time to client relationships and financial planning.

Falling Costs

Total costs have trended downward faster for managed portfolios than for UK mutual funds. Management fees have remained stable, but the “look-through” cost of portfolio holdings is in decline, meaning that providers are saving costs by investing in cheaper funds.

Holding types have a big influence on costs. Underlying holding costs come in more than 3 times higher for managed portfolios that mainly use active funds, compared with competitors that mainly use passive funds.

While it’s not the only consideration for advisors, the similarity of offerings means that cost is an area of competition and potential differentiation.

Different Tax Treatment Compared to Funds

Tax treatment for managed portfolios is different to funds, which is important if investing outside a tax wrapper. With funds, tax is handled inside the fund itself. In a managed portfolio each individual asset can separately realize taxable capital gains, so every rebalance or trade could have tax consequences.

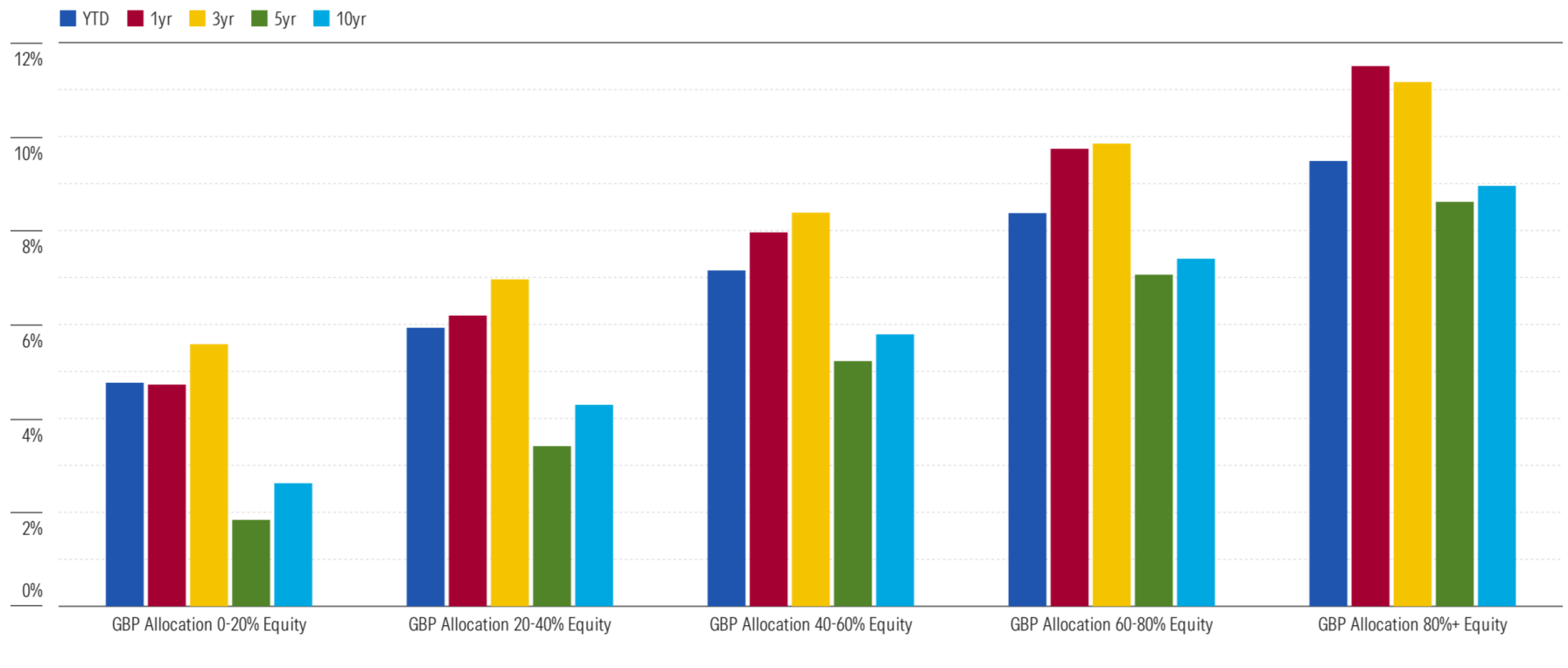

How Have Managed Portfolios Performed?

The most cautious categories have fared relatively well against their respective Morningstar indexes over the five-year period to the end of September 2025. However, the index becomes a more challenging yardstick in the more adventurous categories.

This chimes with Morningstar research indicating higher success rates for active management in fixed income than in equities.

Multi-asset funds and managed portfolios typically share the same drivers of underperformance.

- Costs: Management fees and the costs of underlying holdings all detract from investors’ returns.

- Allocation differences: Portfolios with an equity underweighting compared with the index, or those making untimely allocation shifts, faced a performance headwind as equities significantly outperformed bonds.

- Security selection: The outperformance of giant US companies has made portfolio construction decisions—such as at a geographical, sector, or stock level— particularly important for equity-heavy allocation strategies.

- Market-timing attempts: Only a handful win at market timing – most lose to a steady, static portfolio.

Model Portfolio Morningstar Category Average Trailing Returns, Annualized

Source: Morningstar Direct. Data as of Sept. 30, 2025.

What’s in Managed Portfolios?

About 85% of managed portfolios in the Morningstar database label themselves “open architecture.” That means they can invest in nonproprietary managed investments with a wide choice of possible holdings.

The remaining 15% stick to in-house funds.

Passive and blended offerings are on the rise across asset classes

The proportion of offerings with primarily actively managed holdings is in steady decline. Cost considerations are a key driver of the trend, with most recent launches using greater passive content and styling themselves “Passive” or “Blended.”

Open-end funds dominate

Open-end funds account for over 92% of total allocations. They provide advantages such as:

- Platform availability

- Scalability and liquidity

- Ease of execution

ETFs play a supporting role, making up about 7.5% of total allocations. Their advantages—such as low costs and access to specific passive exposures—also come with the drawback of more complex execution on platforms.

The most popular equity funds are passive

Many of the most held funds are passive funds providing cheap, straightforward, market-cap-weighted index exposure to geographical regions or major country markets. The most popular options span the United States, United Kingdom, Europe, Japan, and global emerging markets, as well as listed real estate and listed infrastructure.

The Fidelity Index US Fund was the most-held equity fund in our study, invested in by 364 portfolios. The report also covers the top 10 most popular active equity funds.

Widely held fixed-income funds feature core exposures

Passive funds also dominate the list of top 10 most-held fixed-income funds. Core exposures like US and UK government bonds, and global aggregate bonds, feature most heavily.

The Vanguard US Government Bond Index Fund was the most-popular fund as of September 30, 2025, held by 321 managed portfolios. For active fixed income funds, ethical and sustainable strategies are among the most owned.

Alternatives use remains modest

Managed portfolios stick mainly to equity, bond, and cash allocations. Alternatives allocations are lower than we find in the equivalent multi-asset fund categories.

The diversification benefits of alternatives come with a cost trade-off. As liquidity is critical for managed portfolios, alternatives use is chiefly through liquid alternatives funds. Some providers are prepared to use listed, closed-end vehicles for access to direct assets, but this tends to be in small doses because liquidity and premiums/discounts to NAV need to be monitored.

What Are the Best Managed Portfolio Options?

Morningstar’s UK Managed Portfolio Database is the first independently collected market database of UK managed portfolios implemented on platforms. As of October 2025, it covered 1,475 live portfolios from 70 provider firms.

The comprehensive data includes:

- Asset allocation

- Complete portfolio holdings

- Costs

- Independently calculated performance and risk reporting