5 min read

US Refiners Benefit From Oil Market Disruptions, but Expectations Are High

Refining margins are likely to remain elevated in the near term, but valuations are still stretched.

Key Takeaways

- The conflict in the Middle East abruptly tightened global oil and product supply, driving a sharp rise in refining margins led by diesel.

- Refiner stocks have rallied on expectations for stronger earnings, but current valuations suggest investors are betting elevated margins will last longer than history would indicate.

- Near-term market conditions remain favorable for US refiners, though sustained high fuel prices could eventually pressure demand.

Expectations Are High, and That’s Starting to Show in Valuations

The second quarter is typically one of the strongest periods of the year for refiners. This year, seasonal tailwinds have become hurricane-strength winds thanks to disruptions in the Middle East.

US refiners are especially well positioned because they have access to alternative crude supplies and continue to benefit from relatively low domestic natural gas prices. That combination has allowed them to capture stronger refining margins without seeing a comparable increase in operating costs.

While a recent deal suggests that the Strait of Hormuz will fully open shortly, we expect effects from the disruption to linger. Fuel markets will likely need time to rebalance, supporting elevated margins through the remainder of the year.

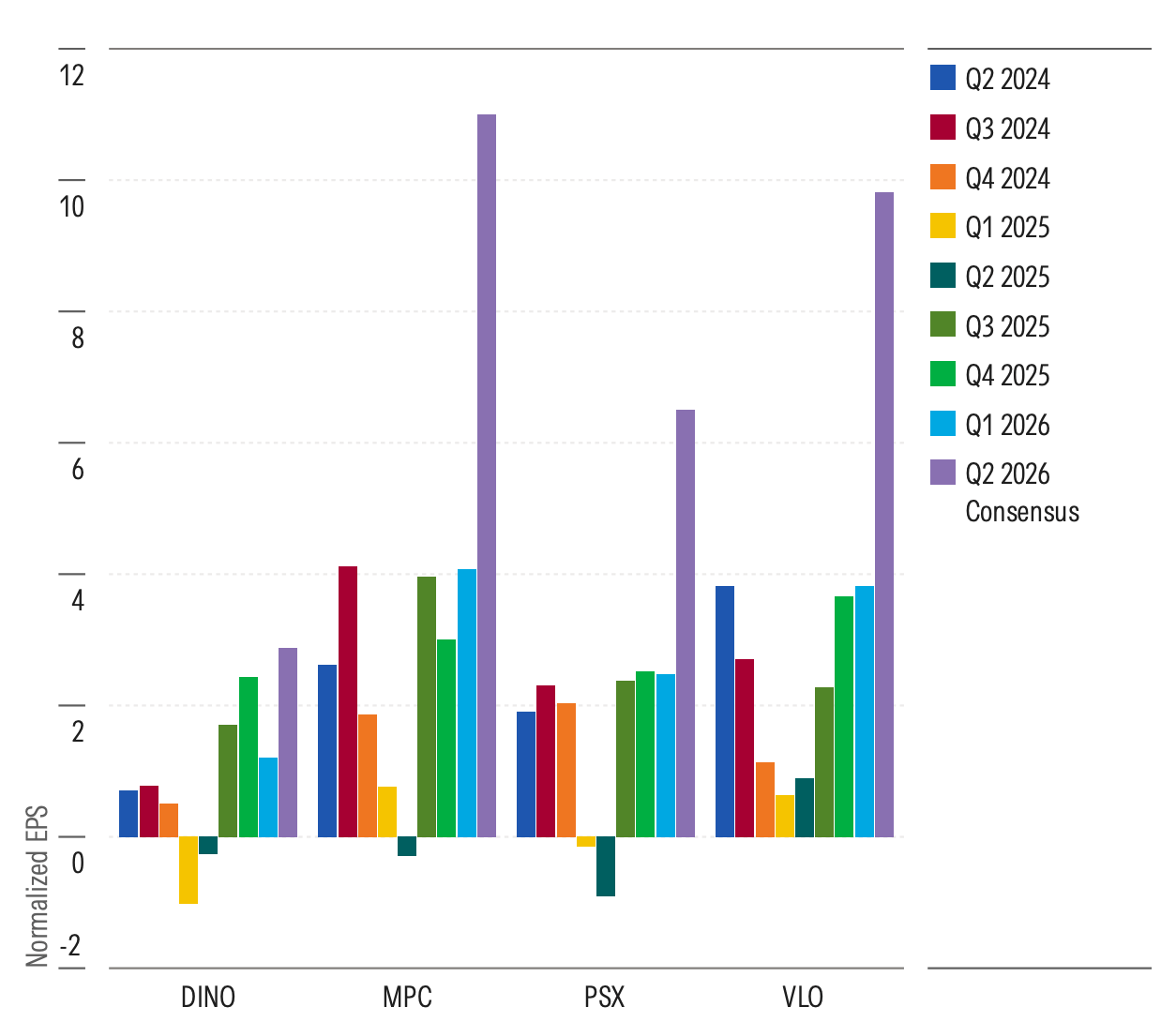

Earnings Are Expected to Soar in Q2 After a Full Quarter of Middle East Disruptions

Source: Pitchbook.

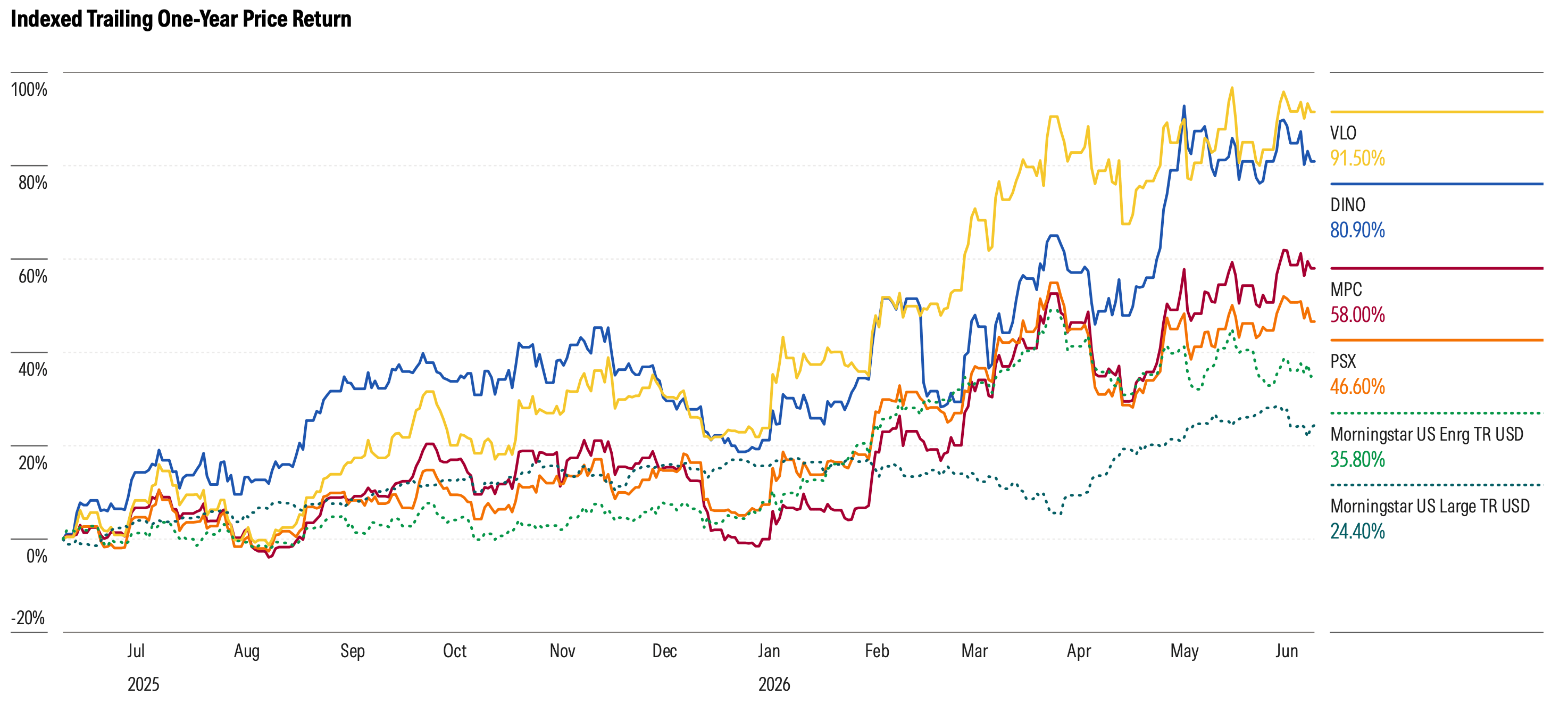

Stocks have rallied on the strong outlook

Refining stocks were already performing well before the conflict escalated, up over 18% on average through late February, reflecting confidence in a strong earnings year. After the war began, shares surged further, leaving the group up roughly 44% by late March. Even after accounting for the latest rise in near-term margins, we still largely see the group as overvalued.

We don’t dispute the notion of a very strong earnings year for the group, with the potential to set new records. However, our valuation approach assumes profits eventually return to more typical midcycle levels. While near-term earnings expectations have improved, we haven’t seen enough evidence to justify permanently higher valuations.

Valuations at a Glance

At first glance, many refiners appear inexpensive based on projected 2026 earnings. The challenge is that today’s unusually strong conditions are unlikely to persist as the Strait of Hormuz reopens and product markets normalize. We don’t think current share prices are being extrapolated beyond 2026. The low multiples on 2026 earnings seem to confirm this.

However, we do think the market is expecting higher-than-midcycle conditions for longer, especially for Marathon and Valero. Our discounted cash flow-derived fair value estimates suggest that those are the most overvalued, even as they are the biggest beneficiaries of the current market conditions.

Market Conditions

Strong conditions are likely to fade as Middle East exports normalize.

Margins are coming off their peaks but should stay elevated

Diesel margins surged after disruptions in the Middle East tightened supplies of the heavier crude grades needed to produce diesel. Gasoline margins soon followed as inventories declined and demand remained resilient.

The reopening of the Strait of Hormuz should ease some pressure, but inventories still need to be rebuilt and trade flows normalized. As a result, margins are likely to remain above historical averages into next year, even if they gradually move lower from current levels.

Demand has held in the face of higher prices

Despite higher prices across all products, US demand remained relatively stable, further supporting margins. Strong export markets, particularly for diesel, gave additional support.

Heading into the summer driving season, demand should benefit from the recent decline in oil prices, even as strong margins continue to push prices higher. The lower prices also remove a key risk of demand destruction that would offset the otherwise favorable conditions.

US refiners still hold a cost advantage

One of the biggest advantages for US refiners is access to lower-cost natural gas. Valero estimates US refiners realized a cost advantage of about $3.87/barrel in 2023, $2.70/bbl in 2024, and $2.60/bbl in 2025. Although lower than the peak of $9/bbl in the first quarter of 2022, it’s well above the $1/bbl in 2019.

The Iran war resulted in another spike in European prices, albeit not to 2022 levels, increasing US refiners’ advantage. A peace deal is unlikely to result in a quick reversion of prices to prewar levels, as prices are likely to remain high to ensure that low storage levels are refilled by winter.

Long-term, Europe remains reliant on liquefied natural gas imports as its marginal supplier, meaning the region is always at risk from colder-than-expected weather in Europe or Asia or global supply disruptions, which could send prices higher.

Complex gulf coast refiners continue to benefit

Heavy crude differentials widened considerably as US light sweet crude was increasingly diverted to Asia and Venezuelan barrels returned to the market. At the same time, planned and unplanned refinery outages added further pressure to heavy crude markets.

Those conditions have created a meaningful tailwind for complex refiners that can process a broader range of crude types. Increased flows from the Middle East should eventually help narrow those differentials, but it will take time for markets to rebalance. In the meantime, complex refiners remain well positioned.

The long-term supply outlook still favors US refiners

While the reopening of the Strait of Hormuz will remove some of the temporary support currently boosting margins, normalization won't happen overnight. The closure effectively disrupted flows tied to roughly 11% of global refining capacity. Even after normal transit resumes, inventories need to be rebuilt and trade flows reestablished—a process that could take several months.

The longer-term outlook also remains constructive. Global refining capacity additions are expected to slow, while additional closures are likely across Europe and North America. Ongoing disruptions at Russian refineries and delays at major projects in Mexico and Nigeria further support the competitive position of US refiners.

Refining Valuations

Valuations still reflect a stronger-for-longer outlook.

Refining Stocks Pulled Back Slightly, but Remain Near Highs

Source: Pitchbook. Data as of June 12, 2026.

Asset valuations suggest refining valuations are unreasonable

One way to gauge how aggressively the market is valuing refiners is through market-implied asset values, or adjusted enterprise value per complexity barrel.

While these measures aren't precise valuation tools, they can provide a useful relative comparison over time. By that standard, most refiners are trading above their average valuation levels from 2014–19.

That lines up with our discounted cash flow analysis, which also suggests the market is pricing in profitability that remains above midcycle levels for longer than we expect. In fact, valuation levels are now back around—or above—the levels reached in April 2024, just before the sector experienced a significant pullback.

Debt to fall and payouts set to rise in 2026

Balance sheets weakened in 2025 but should improve in 2026, given the current extraordinary conditions, resulting in very strong cash flow. Phillips 66 has an explicit target to reduce debt by 2027. Payouts should also increase, reversing the declines in 2025, as most refiners have set return targets as a percentage of earnings or cash flow, which will be much higher. Yields look relatively low compared with recent history, given the strong share price performance.

Margins in Q1 don’t reflect strength of Q2

Investors should be careful about using first-quarter results to assess the current earnings environment. Refining profitability is determined by various factors—output mix, capture rate, and crude slate—that differ across refiners.

Given a heavy turnaround schedule and the fact that the Iran war didn’t begin until late in the period, first-quarter gross margins are not reflective of what will be reported in the second quarter. We expect materially stronger second-quarter margins based on company-reported indicators. However, a severely backwardated crude curve may weigh on capture rates.

Beyond that, margins will likely remain elevated but lower than current levels as Middle East supplies return to the market.

Expect lower costs in Q2 as volumes rise and natural gas prices fall

First-quarter costs were negatively affected by turnarounds and higher gas prices. Both should reverse in the second quarter, bringing lower operating costs per barrel.

Marathon Petroleum and Valero remain the low-cost leaders. HF Sinclair is executing on its plans to improve reliability and reduce costs. Operating costs fell to $8.04/bbl, still higher than the full-year 2025 figure of $7.67/bbl. Turnarounds played a role, and we remain confident that the company will achieve its $7.25/bbl medium-term goal. Despite the CEO’s departure, we expect management to maintain its focus on cost reduction. Phillips 66’s costs increased due to higher gas prices, but management is still targeting a cost of $5.50/bbl by 2027.

Beyond the quarterly volatility, US refiners maintain some of the lowest operating costs among global refiners, thanks to lower natural gas prices and high utilization and reliability.