Between enabling account holders to reap investment gains on a tax-free basis (so long as they are spent on education) and, in some cases, offering tax benefits as an additional incentive to save for college, 529 plans have proven to be a popular way for families to stretch their college savings. And advisors play an important role in helping people maximize the benefits of these plans.

Despite the popularity and usefulness of 529 plans, many could be improved. Plan quality, measured by the Morningstar Analyst Rating™, varies from state to state: Only 11.6% of the population in the United States lives in a state that provides a Gold-rated plan, and 27.8% lives in a state where the best-rated plan earns a Neutral or Negative rating.

Against this backdrop, Morningstar’s policy research team surveyed the landscape of 529 policy and plans for the study, “ Bigger Is Probably Better: How Policymakers Can Improve 529 Savers’ Experiences.”

We focused on identifying variables potentially associated with higher-quality plans and whether state tax incentives are useful policy tools to support higher education. Below, take a look at our findings.

Plans in bigger states tend to be better

Our 529 policy research analysis examined several variables for potential association with higher-quality plans: a state’s population, per capita income, and tax policies.

Our research found the only significant variable was a state’s population, as more populous states are associated with providing higher-quality plans. There are outliers—Nevada and Utah, for instance, both have small populations and support Gold-rated plans—but on the whole, we found a statistically significant link between population and plan quality.

Our interpretation of this evidence is that it is easier for a state with more assets to attract a high-quality program manager, improve plan oversight, and lower investment fees for account holders.

None of the other variables we investigated—a state’s per capita income, tax deductions for 529 contributions, or the presence of state income tax—had a statistically significant association with plan quality.

Alluring tax incentives may lead savers to subpar plans

Next, we examined the interplay of state tax policies and 529-plan quality. In some states, maximizing the benefits of a 529 plan requires some households to calculate the trade-offs between tax incentives—which usually come in the form of deductions from state taxes—and plan quality. It’s important to note that not all households face this trade-off, since 529 policies vary from state to state. For instance:

- California, along with some other states, does not offer residents the ability to deduct 529 contributions from state income taxes.

- Residents of states without income taxes, like Nevada and Florida, wouldn’t receive a state income tax deduction in the first place.

- Some states, like Utah and Virginia, offer highly rated plans in addition to tax benefits.

However, this patchwork of tax regimes precludes one-size-fits-all advice about whether it’s more sensible to forgo tax incentives and invest in a higher-quality, out-of-state 529 plan, or to realize the tax benefits from a lower-performing or more expensive in-state option.

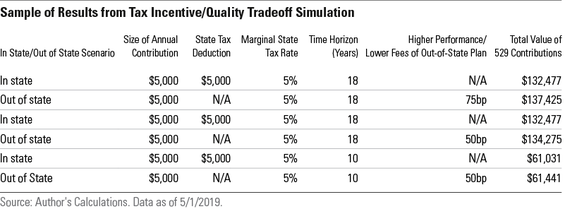

Morningstar’s policy research team built a simplified, highly stylized model to compare the impact of a higher-quality, out-of-state plan with a more expensive in-state plan that offers tax benefits. In the chart below, we consider a hypothetical household facing a 5% marginal tax rate and living in a state that offers a $5,000 deduction on state income taxes for 529 contributions.

This illustrative model shows that in this case, it may be advantageous for households starting to save for college early to forgo in-state tax benefits in favor of investing their savings in high-quality, out-of-state 529 plans. Those plans allow stronger performance, lower fees, or both, to compound over time.

However, if tax credits encourage 529 savers to keep their money in state, even if they begin putting money away for college when the beneficiary is born, they could ultimately end up with less money saved.

Alternatively, if a household has a shorter time horizon—say, starting to save for college when the prospective student is eight years old—then it may be advantageous to invest in a lower-quality, in-state 529 plan while reaping the immediate benefits of deductions and tax credits.

Our 529 policy recommendations

Given the evidence, our recommendations for how policymakers can improve the experiences of college savers include:

- Smaller states should consider consolidating their 529 plans. Our analysis found that states with larger populations were associated with providing higher-quality 529 plans. Consolidation would eliminate duplicative plan infrastructure and allow states to leverage a larger asset base, which would reduce management fees and pass those savings on to account holders.

- Policymakers should reconsider their approach to encouraging and supporting higher education. State tax incentives might encourage 529 savers to keep their money in state, even if they would be best served by investing in an out-of-state plan.