We've published new research. Read highlights from our latest Markets Observer.

Every quarter, Morningstar’s quantitative research team reviews the most recent global market trends in finance and evaluates the performance of individual asset classes. Then, we share our findings in the Morningstar Markets Observe r, a publication that draws on quantitative analysts’ careful research and market insights.

5 trends from our latest quarterly market update:

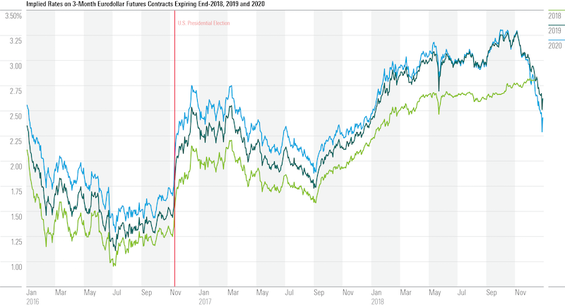

- Expectations for future rates sharply decline in 2018. Implied rates on three-month Eurodollar futures act as a market prediction for U.S. interest rates at the expiration date of the contract. In the fourth quarter of 2018, the implied rates on futures expiring in 2019 and 2020 sharply declined, which implies a decreasing outlook for interest rates in the future. This is in contrast with the stability of the implied rates on the 2018 contracts owing to their pending expiry and convergence to the current interest rates targeted by the Federal Reserve.

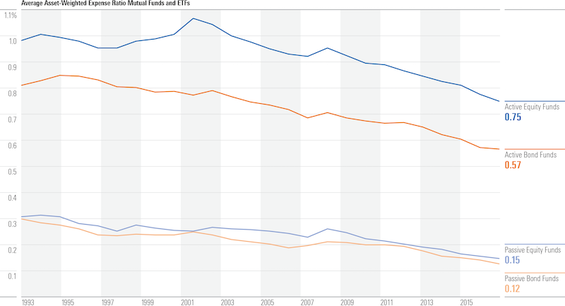

- Competition from passive funds pushes active-fund expenses lower. Asset-weighted average fees for both active and passive funds have been declining for the past two decades. The real driver of the decline has been investors selling high-fee funds and buying less expensive ones. In recent years, both active and passive funds have continued on a downward trajectory, but the decline has been slower for passive funds because their fees are already near zero. In the past year, however, the rate of decline for active bond funds has slowed.

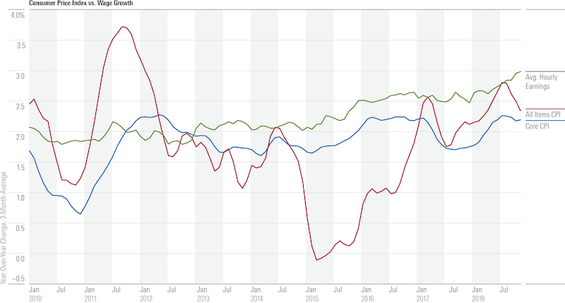

- Much ado about something. There has been much ado about wage growth hitting a nine-year high. Given its decade-long sluggishness, there’s good reason to cheer. However, when adjusted by the Consumer Price Index, real earnings, which get eaten by inflation, don’t look quite as plump. All the more reason to applaud the recent dip in the CPI. Given the strong retail sales, it’s good to see people spreading the holiday cheer.

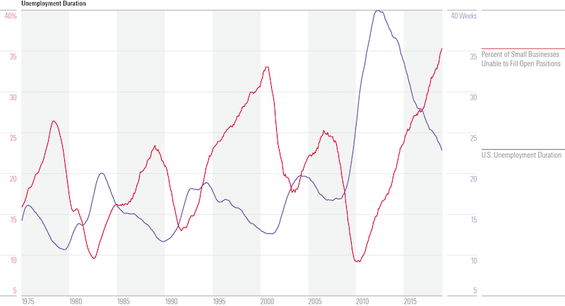

- Wait ... just a little bit longer. After the last recession, unemployment duration skyrocketed to levels never observed previously and has remained tenaciously high. At 23 weeks, the current average duration is still longer than maximum durations in previous recessions. Weak labor demand can only explain so much given the current unemployment rates. But the percentage of small businesses not able to fill open positions offers a clue. A mismatch in qualifications for open positions is leading to the longer durations.

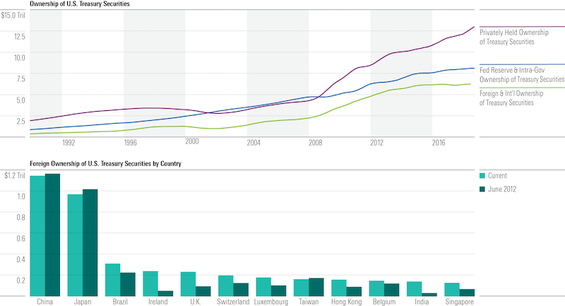

- Look who’s buying. Ever since the Federal Reserve stopped buying U.S. Treasuries in 2014, private investors have picked up the deficit slack, increasing ownership by over $2.5 trillion in the past three years. In the meantime, the two largest international investors, China and Japan, have backed off. Overall foreign ownership stayed flat, however, because Europe and Brazil have made up the gap since 2012.

This blog post is adapted from research that was originally published in the Morningstar Direct℠ Research Portal. If you’re a user, you have access. If not, take a free trial.