7 Undervalued Stocks With Healthy Yields

We expect these high yielders to sustain their dividends in the future. Plus, they're cheap.

/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)

It's the eternal question for dividend seekers: How can you be sure the dividend stock you own today won't slice its payout tomorrow?

Dan Lefkovitz, a strategist in Morningstar's indexes group, argues that two particular factors can lead investors to stocks with solid dividends: economic moats and distance-to-default scores.

Companies with moats are able to successfully sustain their profits and fend off competitors; distance to default, meanwhile, measures balance-sheet strength and the likelihood of bankruptcy.

"We found that the wider the economic moat and the better the distance-to-default score, the less likely for a firm to cut its dividend," says Lefkovitz.

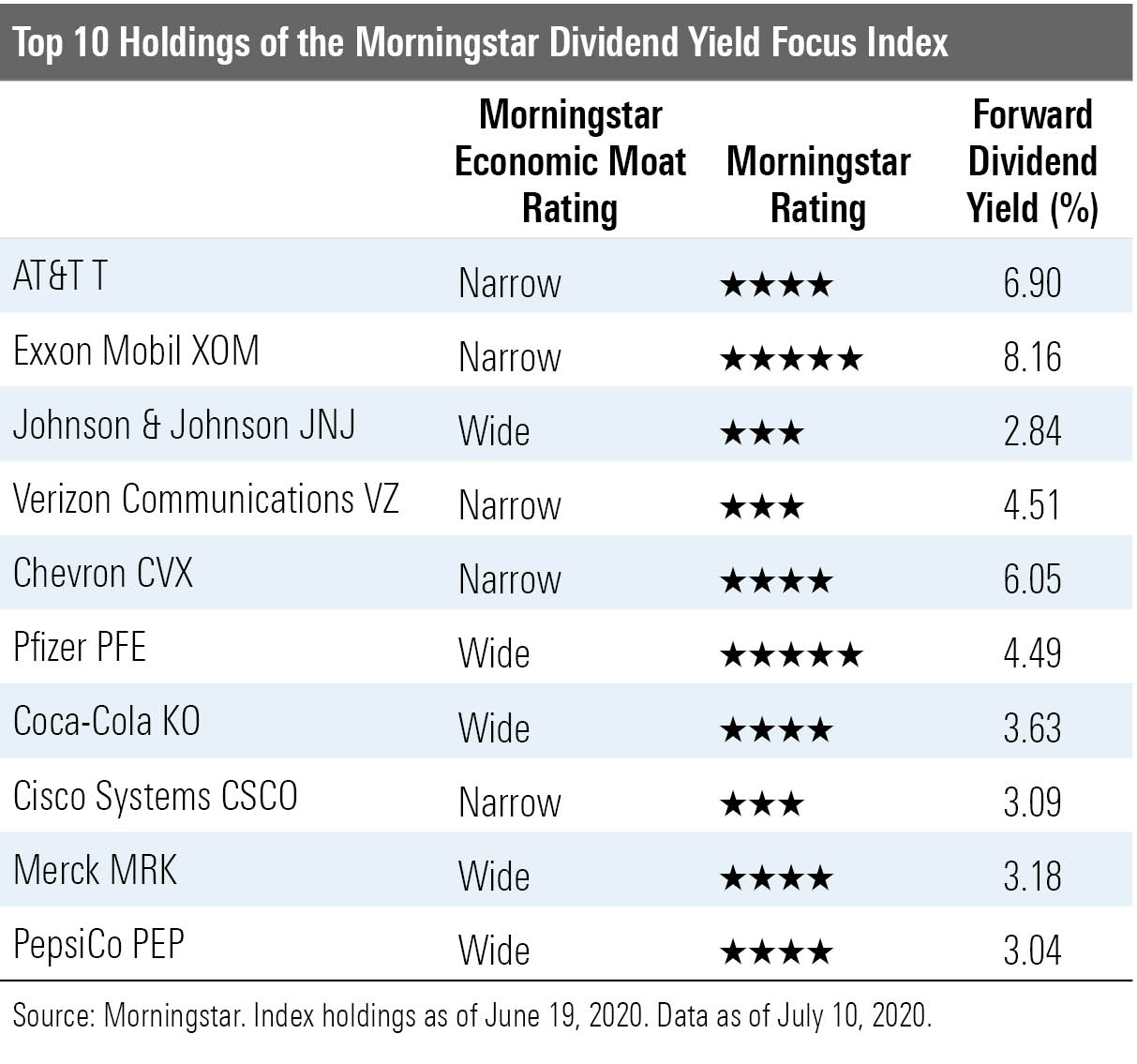

Morningstar blends those two factors when constructing the Morningstar Dividend Yield Focus Index. A subset of the Morningstar US Market Index (which represents 97% of equity market capitalization), this index tracks the top 75 high-yielding stocks that meet our screening requirements for quality and financial health.

How are the index constituents chosen? For starters, only securities whose dividends are qualified income are included; real estate investment trusts are tossed out. Companies are then screened for quality using the Morningstar Economic Moat and Morningstar Uncertainty ratings. Specifically, companies must earn a moat rating of narrow or wide and an uncertainty rating of low, medium, or high; companies with very high or extreme uncertainty ratings are excluded. We then screen for financial health using our distance-to-default measure, which uses market information and accounting data to determine how likely a firm is to default on its liabilities. The 75 highest-yielding stocks that pass the quality screen are included in the index, and constituents are weighted according to the total dividends paid by the company to investors.

Here are the index's top 10 holdings as of the latest reconstitution in June 2020. Seven of the stocks are undervalued by our metrics as of this writing.

Here's a little bit from our analysts about the strength of the moats--and therefore the quality--for the seven undervalued names.

AT&T T "Following the Time Warner acquisition, AT&T is truly a behemoth, with roughly $480 billion of invested capital employed in the business, or about $335 billion excluding goodwill. Its operations are now diversified across several distinct but interrelated businesses. AT&T's grand strategy is to meld its consumer-facing telecom and media businesses into cohesive service offerings that attract and retain customers. We're doubtful this plan will yield significant benefits. The telecom and media businesses are simultaneously mature and rapidly changing. We believe most consumers are generally aware of the wireless carriers' strengths and weaknesses, choosing providers primarily based on service quality and price rather than add-ons or bundle options. We also expect the best content creators, including writers and actors, will migrate toward media firms that deliver the best mix of audience size and monetization potential over time. This dynamic should limit AT&T's ability to overly restrict access to or discount the content it produces. Finally, AT&T's scope should enable it to improve advertising yields, but we also expect changing consumer demands will force an offsetting reduction in ad loads across the traditional television market.

"Looking at AT&T's businesses individually, we believe the firm still deserves a narrow moat based primarily on cost advantages within the wireless business and intangible assets acquired with Time Warner. These advantages should enable the firm to maintain relationships with customers and increase free cash flow. However, recent capital-allocation decisions have sharply lowered returns on invested capital. In aggregate, AT&T is a collection of businesses that should produce double-digit ROICs, but high acquisition prices will likely leave ROICs roughly in line with the firm's cost of capital, as we calculate it, despite significant competitive advantages."

--Mike Hodel, director

Exxon Mobil XOM "We continue to rate Exxon Mobil as one of the higher-quality integrated firms, given its ability to capture economic rents along the oil and gas value chain. While its peers operate a similar business model with the same goal, they fail to do so as successfully, as evidenced in the lower margins and returns compared with Exxon. Exxon generates its superior returns from the integration of low-cost assets (an intangible asset that we consider to be part of its moat source) combined with a low cost of capital; this combination produces excess returns greater than those of its peers. However, given our outlook for lower long-term oil and natural gas prices, we expect Exxon's returns to be lower than they have been in the past. Additionally, its decision to increase investment relative to peers during the next five years is also likely to narrow the gap in returns with peers. Consequently, our confidence that it can continue to deliver excess returns for longer is diminished, resulting in the company earning a narrow moat."

--Allen Good, strategist

Chevron CVX "Although Chevron is an integrated energy company, its narrow economic moat rests on the quality of its upstream portfolio. Chevron's upstream segment holds a low-cost position based on an evaluation of its oil- and gas-producing assets, using our exploration and production moat framework. Its greater exposure to liquids and liquids-linked natural gas production has produced peer-leading cash margins during the past five years and resulted in returns on capital employed of nearly 20%, among the highest of the group. New production from its LNG projects Gorgon and Wheatstone, offshore oil developments in the Gulf of Mexico and West Africa, and tight oil growth should preserve this exposure. We forecast that Chevron can deliver a midcycle cash operating margin of nearly $30 per barrel of oil equivalent, the highest in its peer group."

--Allen Good, strategist

Pfizer PFE "Patents, economies of scale, and a powerful distribution network support Pfizer's wide moat. Pfizer's patent-protected drugs carry strong pricing power that enables the firm to generate returns on invested capital in excess of its cost of capital. Further, the patents give the company time to develop the next generation of drugs before generic competition arises. Additionally, while Pfizer holds a diversified product portfolio, there is some product concentration, with the company's largest product Prevnar representing just over 10% of total sales. However, we don't expect typical generic competition for the vaccine because of complex manufacturing and relatively low prices for the product. Further, we expect new products will mitigate the eventual generic competition of other key drugs. Also, Pfizer's operating structure allows for cost-cutting following patent losses to reduce the margin pressure from lost high-margin drug sales. Overall, Pfizer's established product line creates the enormous cash flows needed to fund the average $800 million in development costs per new drug. In addition, the company's powerful distribution network sets up the company as a strong partner for smaller drug companies that lack Pfizer's resources. Pfizer's entrenched consumer and vaccine franchises create an added layer of competitive advantage, stemming from brand power in consumer healthcare and manufacturing cost advantages in the vaccines division. Pfizer recently created a consumer healthcare joint venture with GlaxoSmithKline that could lead to an eventual divestment of the unit, but the potential divestment shouldn't have a material impact on the firm's moat."

--Damien Conover, director

Coca-Cola KO "Numerous structural advantages should allow Coca-Cola to extract economic rents from the markets in which it competes, giving us confidence in awarding the firm a wide economic moat rating. At a high level, we believe there are characteristics endemic to the nonalcoholic beverage industry more generally, as well as Coca-Cola's specific positioning within this industry, that result in a competitively advantaged business. While the company is disproportionately exposed to beverage categories that are in secular decline, we believe it has the brand equity to induce demand for reformulated variants of its most popular trademarks, the resources to reorient its portfolio toward drink categories that are more consistent with the consumer ethos, and the scale to fulfill these endeavors profitably."

--Nicholas Johnson, analyst

Merck MRK "Patents, economies of scale, and a powerful intellectual base buoy Merck's business and keep it well shielded from the competition. As the bedrock of Merck's wide moat, patent protection should continue to keep competitors at bay while the company strives to introduce the next generation of drugs. Further, the company's enormous cash flows support a powerful salesforce that not only sells currently marketed drugs but also serves as a deterrent for developing drug companies seeking to launch competing products. As a result, Merck offers a powerful partnership opportunity for externally developed drugs. The cash flows also put the company in the rare position of supporting the approximately $800 million in research and development needed on average to bring each new drug to the market. While not as powerful as in the 1990s, Merck's research laboratories still hold a vast database of knowledge that should help the company to maintain its leadership positions in drug discovery and development. Also, the company's entrenchment in the emerging immuno-oncology area should strengthen Merck's competitive position with drugs that carry very strong pricing power in areas of unmet medical need. Lastly, Merck's strong entrenchment in vaccines adds a layer of competitive protection from intellectual property and cost advantages, as the firm's large-scale production enables a lower cost base."

--Damien Conover, director

PepsiCo PEP "We believe several structural dynamics, centered on cost advantages and intangible assets, have solidified PepsiCo's competitive positioning and secured it a wide economic moat. At a high level, we see characteristics of the snack and beverage categories where Pepsi competes, and its positioning within these categories, that should allow the company to continue to glean economic profits. While the firm's integrated business models across food and beverages have pros and cons, we think the combination of diversity, synergy, and flexibility that they facilitate will allow Pepsi to maintain its standing even as its core categories face secular headwinds."

--Nicholas Johnson, analyst

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WC6XJYN7KNGWJIOWVJWDVLDZPY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HHSXAQ5U2RBI5FNOQTRU44ENHM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/737HCNGRFLOAN3I7RKGB7VPEKQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)