Good Value Can Be Found Among Hard-Hit Real Estate Subsectors

We expect malls, hotels, and healthcare subsectors to rebound.

/s3.amazonaws.com/arc-authors/morningstar/b9459b20-3908-4448-a36c-b728946ddbe5.jpg)

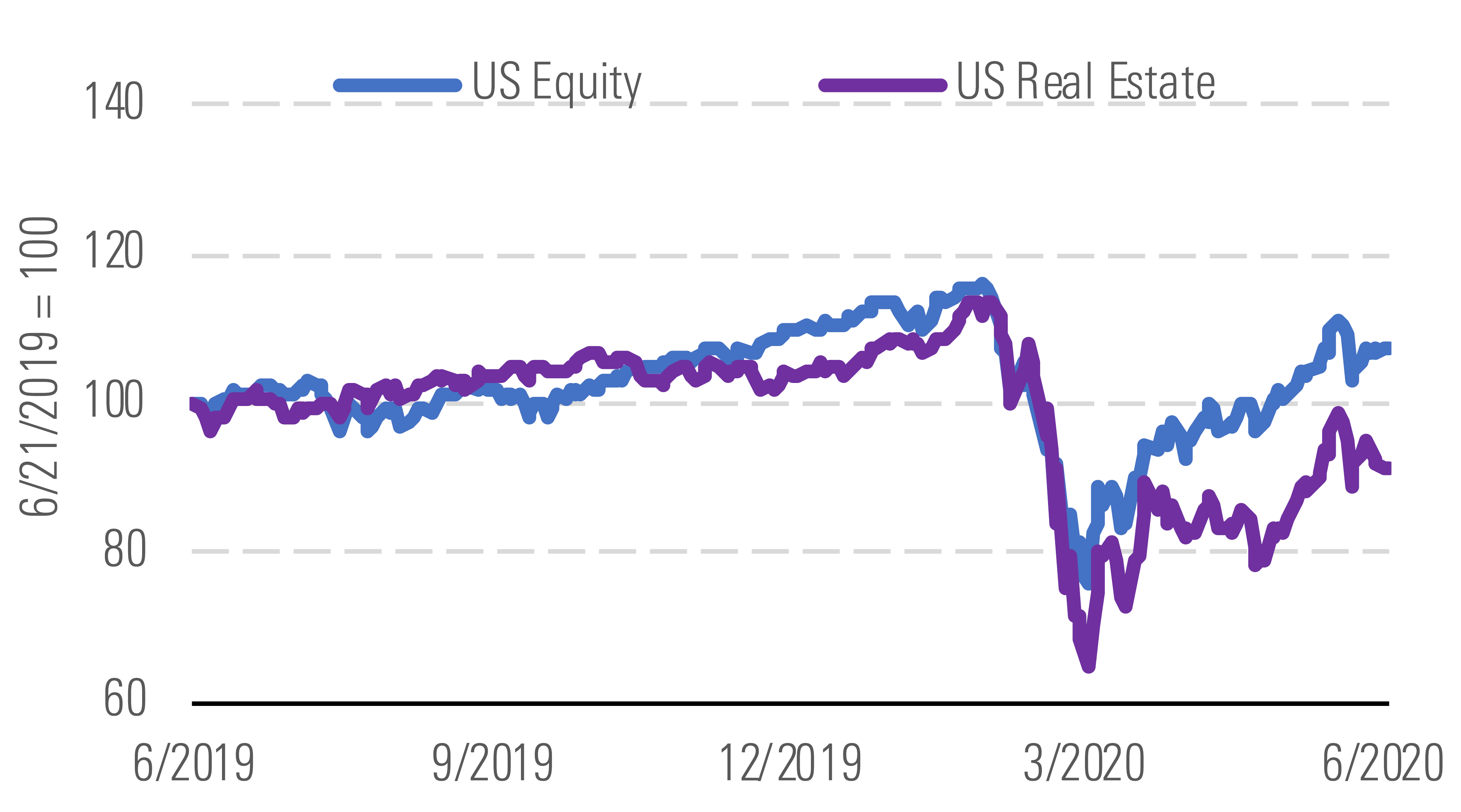

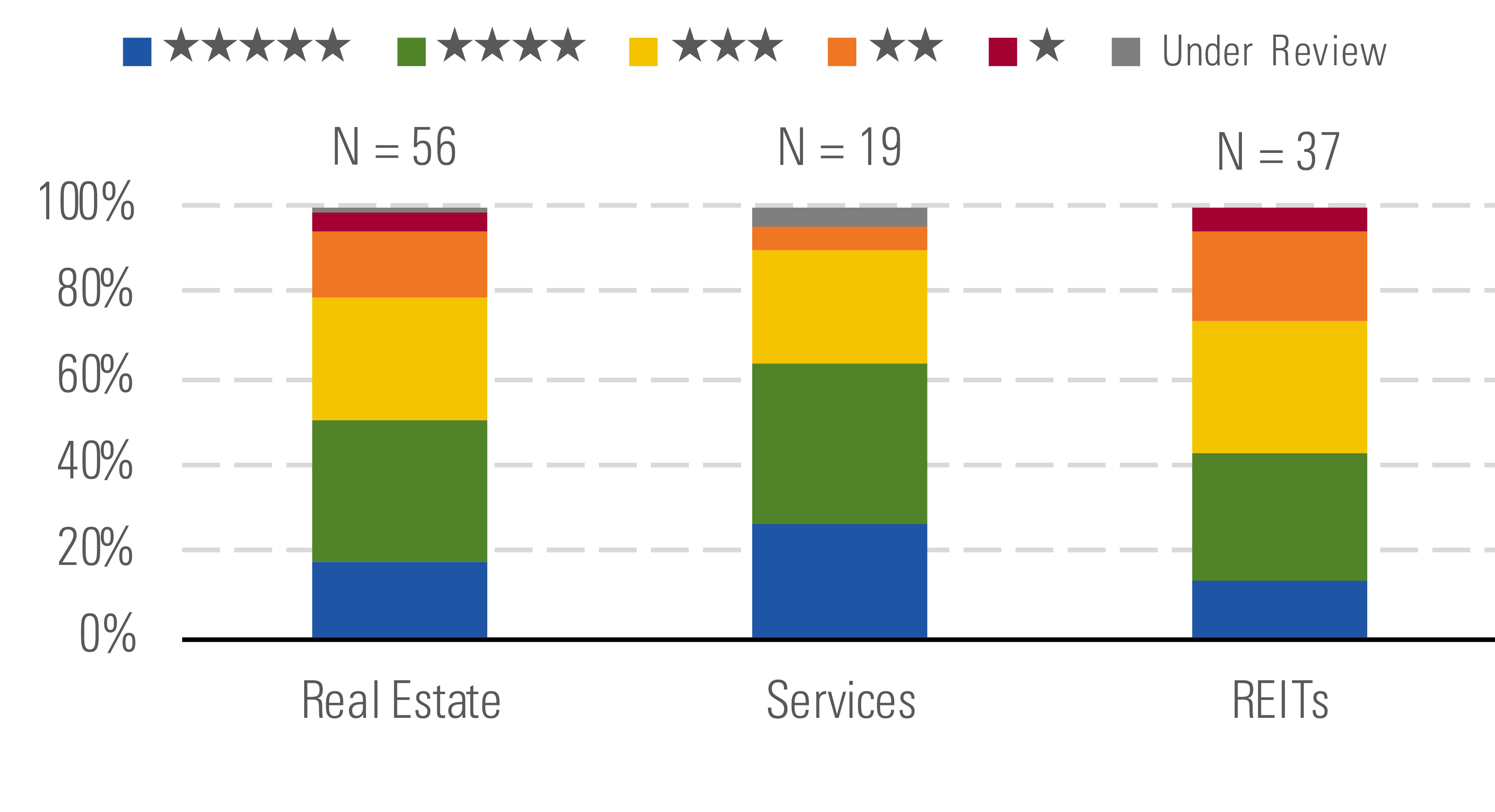

The Morningstar US Real Estate Index fell 8.7% over the trailing 12 months and is underperforming the broader U.S. equity market by 16.4%, as the sector has not shown the same recovery in the second quarter as the broader equity market. However, real estate performance has diverged significantly by subsector. The real estate sector is currently trading at a significant discount. Our coverage currently trades at a 19% discount to our estimate of intrinsic value compared with a 3% premium on average at the end of the fourth quarter. Currently, the real estate sector is 18% 5-star and 32% 4-star, with only 18% of the total sector trading in either a 1-star or 2-star range.

Real estate is down and has underperformed the global equity index. - source: Morningstar

4-star and 5-star companies currently represent half of the sector. - source: Morningstar

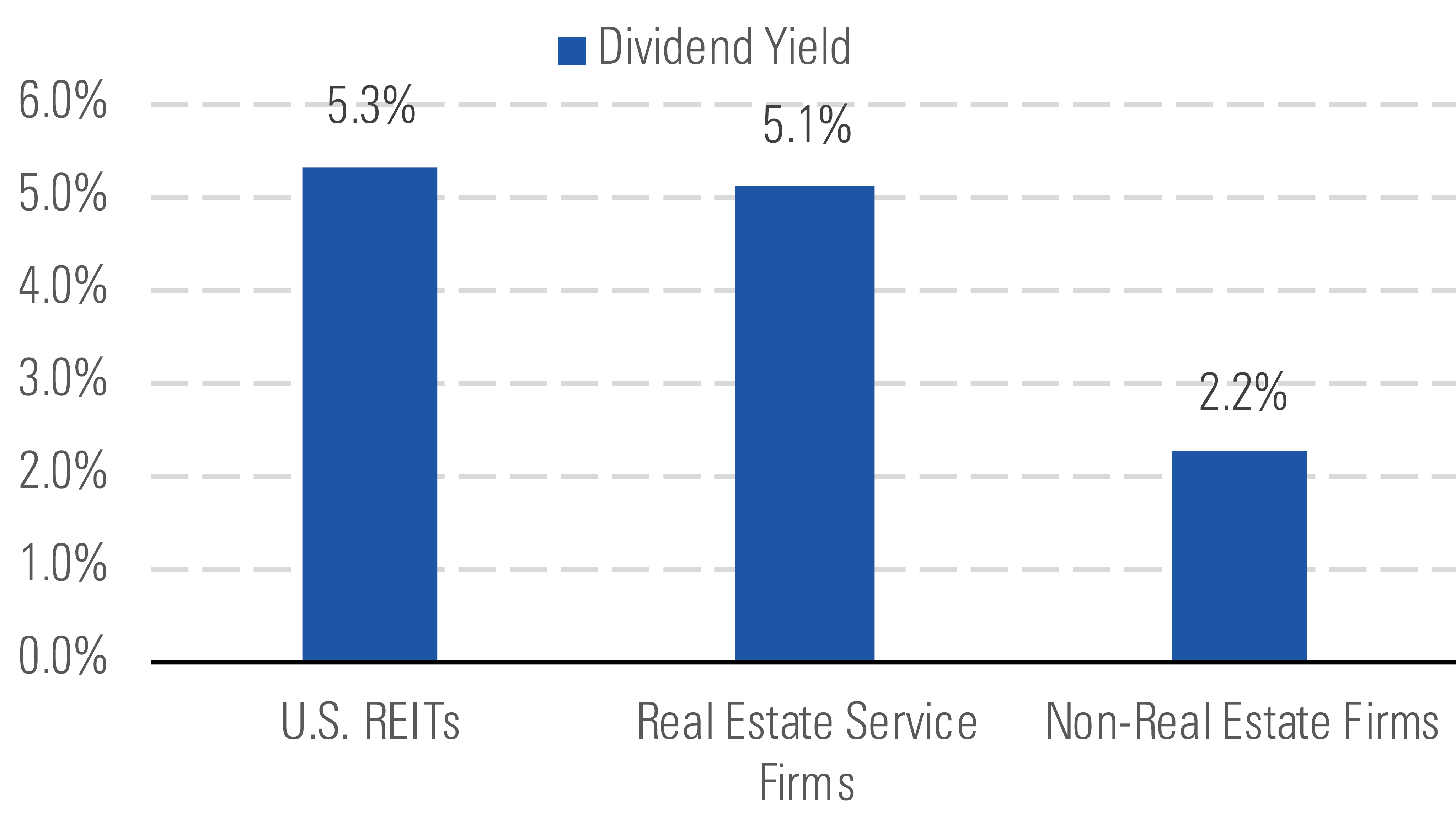

The average dividend for real estate firms is higher than the rest of our coverage. To receive tax-free status, REITs are required to pay out most of their net income as dividends to shareholders, so these companies are frequently included in portfolios of income-oriented investors. As a result of the recent equity sell-off, dividend yields have dramatically increased. We currently believe that most REITs will continue to pay their dividend, making these high yields very attractive to investors.

REITs have higher dividend yields than service firms and other sectors. - source: Morningstar

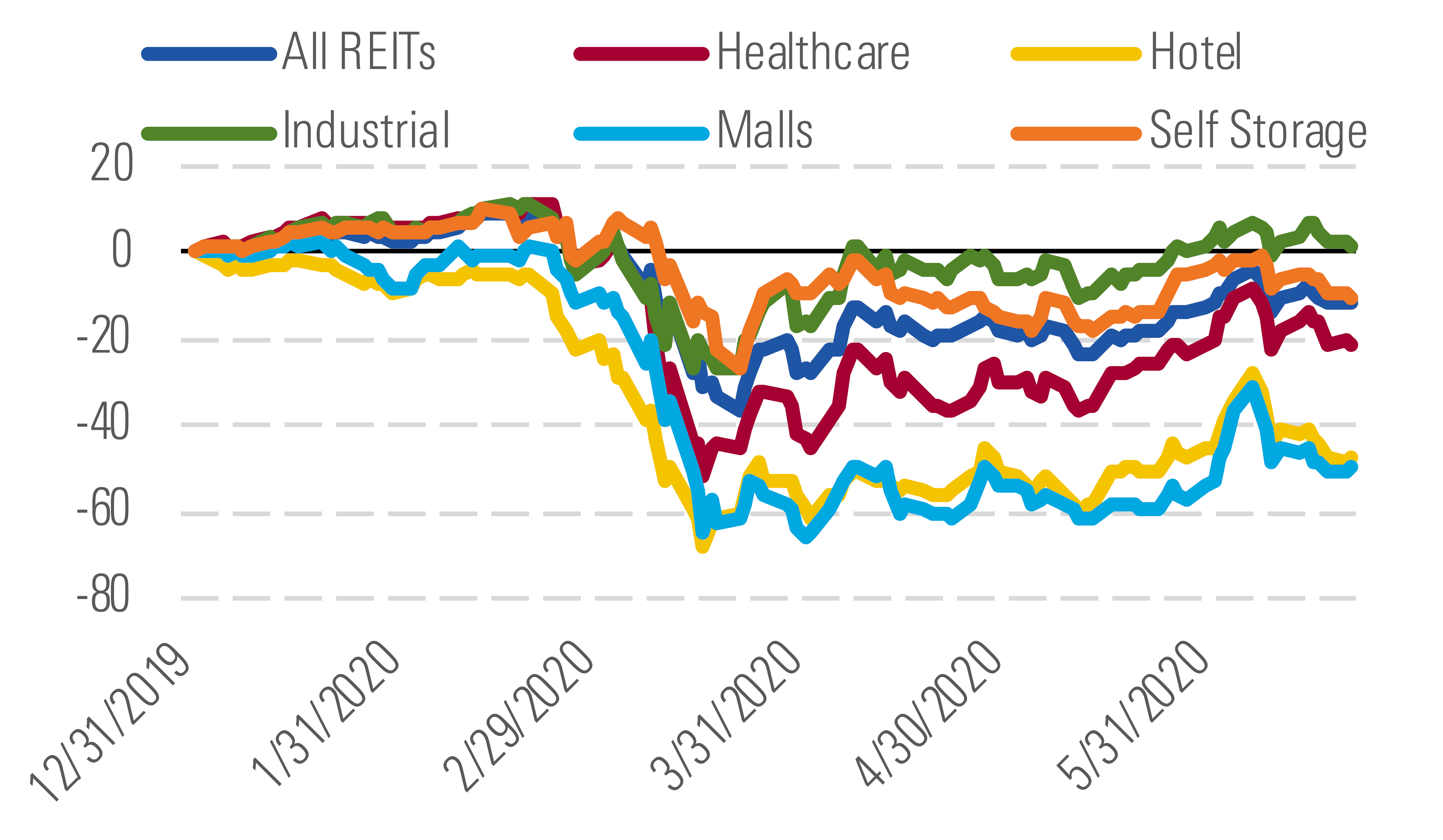

We have seen significant bifurcation in the performance of the different real estate subsectors. Sectors that are more sensitive to the impacts of the coronavirus have seen significantly worse total return performance year to date. Global travel restrictions and lingering fears of the virus spreading have caused massive occupancy declines for the hotel industry. Malls across the country were closed for several months, and consumers are only slowly returning to stores as the country reopens. The virus has a higher lethality rate among the senior population, affecting occupancy at healthcare companies exposed to senior housing. All three sectors have underperformed the broader real estate sector.

Meanwhile, while the industrial and self storage sectors declined initially, they have outperformed the broader real estate sector, and the industrial sector has produced a positive return year to date in 2020. These sectors are outperforming, as they should be relatively insulated from the worst effects of the virus on the global economy. That said, we currently see some of the best values among the hardest-hit subsectors. Given our long-term outlook, we believe that the hotel, mall, and healthcare sectors will rebound and see years of strong growth once the global crisis is over.

Real estate subsectors most affected by the virus have underperformed. - source: Morningstar

Top Picks

Simon Property Group SPG Economic Moat Rating: None Fair Value Estimate: $154 Fair Value Uncertainty: High

Class A malls continue to outperform other forms of brick-and-mortar retail. Over the 12 months ending in February, Simon's tenants produced 6.5% sales per square foot growth, and the company ended the first quarter of 2020 with a healthy 94% occupancy level. The stock has sold off significantly over the past few months as fears of the coronavirus impact on brick-and-mortar retail sales grew among investors. Simon has long-term leases with tenants, so it should continue to receive rent even during the current crisis. While many weaker retailers may go bankrupt because of the lack of sales, we think Simon's attractive portfolio will be able to quickly fill any vacancies.

Pebblebrook Hotel Trust PEB Economic Moat Rating: None Fair Value Estimate: $23.50 Fair Value Uncertainty: Very High

Global travel bans and fears of traveling have significantly affected the hotel industry. We think that Pebblebrook's upper upscale hotel portfolio could see almost a 50% decline in revenue in 2020 and a nearly 100% decline in operating profit. However, we think that the industry should rebound, with several years of strong growth, and the company should eventually return to 2019 peak levels. While we have lowered our outlook for the company, we think that the recent sell-off in the name is overdone, given our long-term outlook for the hotel industry.

Ventas VTR Economic Moat Rating: None Fair Value Estimate: $50 Fair Value Uncertainty: High

Ventas owns high-quality assets in the senior housing, medical office, and life science fields. While the company's medical office and life science portfolios should be relatively unaffected by the coronavirus outbreak, the senior housing portfolio is likely to experience a very significant impact to occupancies, as the virus has the highest lethality rate among senior citizens. However, while the coronavirus will stunt net operating income for the industry in 2020 and potentially 2021, the industry should see strong long-term growth from the coming demographic wave of baby boomers aging into senior housing facilities.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZZNBDLNQHFDQ7GTK5NKTVHJYWA.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HE2XT5SV5ZBU5MOM6PPYWRIGP4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/AET2BGC3RFCFRD4YOXDBBVVYS4.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/b9459b20-3908-4448-a36c-b728946ddbe5.jpg)