Why College Savers Should Stay the Course Through the Coronavirus

An uncertain future should not deter college savers from capturing 529 tax benefits today.

/s3.amazonaws.com/arc-authors/morningstar/eda620e2-f7a7-4aef-bb6c-3fb7f1ac7a38.jpg)

Editor’s note: Read the latest on how the coronavirus is rattling the markets and what investors can do to navigate it.

Since the start of the year, the coronavirus pandemic has stressed communities and reoriented market views. College students were among the first to feel the effects: Students scrambled to return home, whether that was in the United States or abroad, and what many had hoped would be a brief break has instead extended indefinitely. School has moved online, and universities are exploring how to adapt to a socially distanced reality, but with so many unknowns, many people question whether universities can offer value under these new circumstances and if setting aside money in a 529 college savings plan is worthwhile.

With so much still up in the air, many families will have to take stock of their current savings and make hard choices about how to proceed. Even those who have sufficient financial resources may still think "What's the point?" when traditional college matriculation is no longer a given. In our latest 529 Landscape, Morningstar covers the trade-offs of choices like these. Below are our responses to four frequently asked questions.

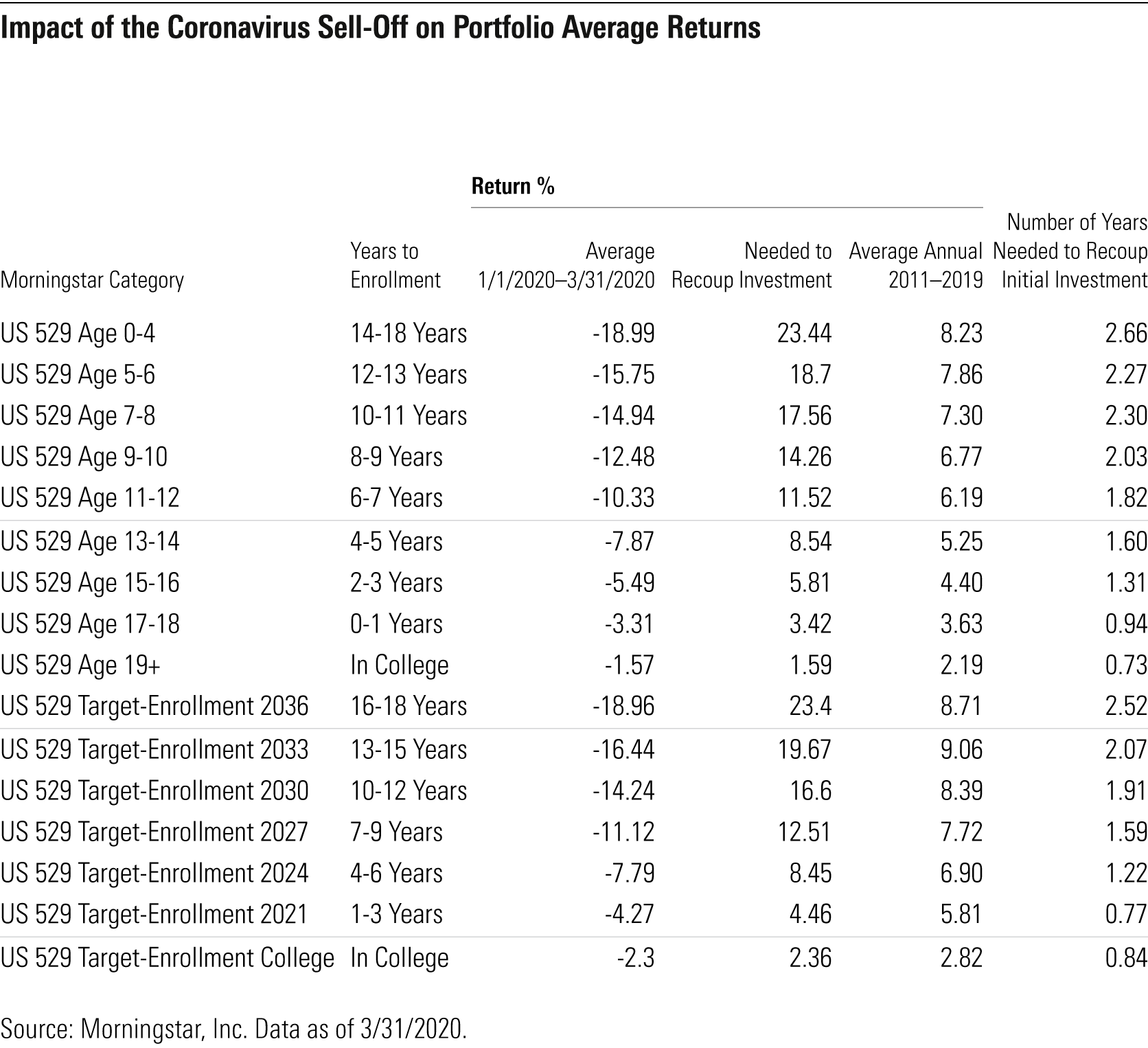

How far did the market crash set 529 portfolios back? The answer to this question often hinges on the age of the 529 beneficiary. Most investors pick an age-based option that implements periodic asset-allocation shifts into bonds from stocks, adjusting risk exposures as the 529 beneficiary nears college matriculation.

Exhibit 1 illustrates the length of hypothetical recoveries to various 529 portfolios following 2020’s first-quarter pandemic panic. We estimated the number of years before an investor gets back to even by calculating the average annual return realized in each age-based category over the past nine years ended December 2019. Of course, past returns are not indicative of future results, especially for target-enrollment portfolios that automatically de-risk over time. The past nine years also don't constitute a full market cycle and represent a generally strong stretch for equities. However, we stopped our measurement at nine years because, prior to 2011, our 529 age-based categories on average held fewer than 30 constituents, limiting the representativeness of category average returns. Investors whose 529 beneficiaries are at or nearing age 18 are running out of time--they need a 3.5% return to make them whole.

But near-college investors have reason to take heart: On average, markets have delivered returns in excess of that 3.5% over the past nine years, so it is not an unrealistic goal to achieve in less than a year. In fact, thanks to the sharp rebound in April, the average 18-year-old has already recouped 2.8%.

Recent history suggests 529 beneficiaries who are 16 and younger also have a good shot at recouping losses they have sustained. However, the possibility of extended economic shutdowns and additional market losses remain an unknown and could limit those asset recoveries.

Why should investors continue contributing to 529 accounts during the crisis? The answer is potential tax benefits. Although federal 529 tax benefits are applied to gains from investments, which increase as long as markets grow, state income tax benefits are granted based on contributions rather than investment gains. Where an investor falls along the gamut of state income taxes could motivate him or her to contribute more or less to a 529 plan. Our 2020 research finds that more than half of states' 529 tax benefits cover a direct-sold plan's expenses for more than a decade, during which time families essentially receive free investment management. This type of coverage provides a powerful incentive for families to continue contributing who may not have used up the entirety of that benefit.

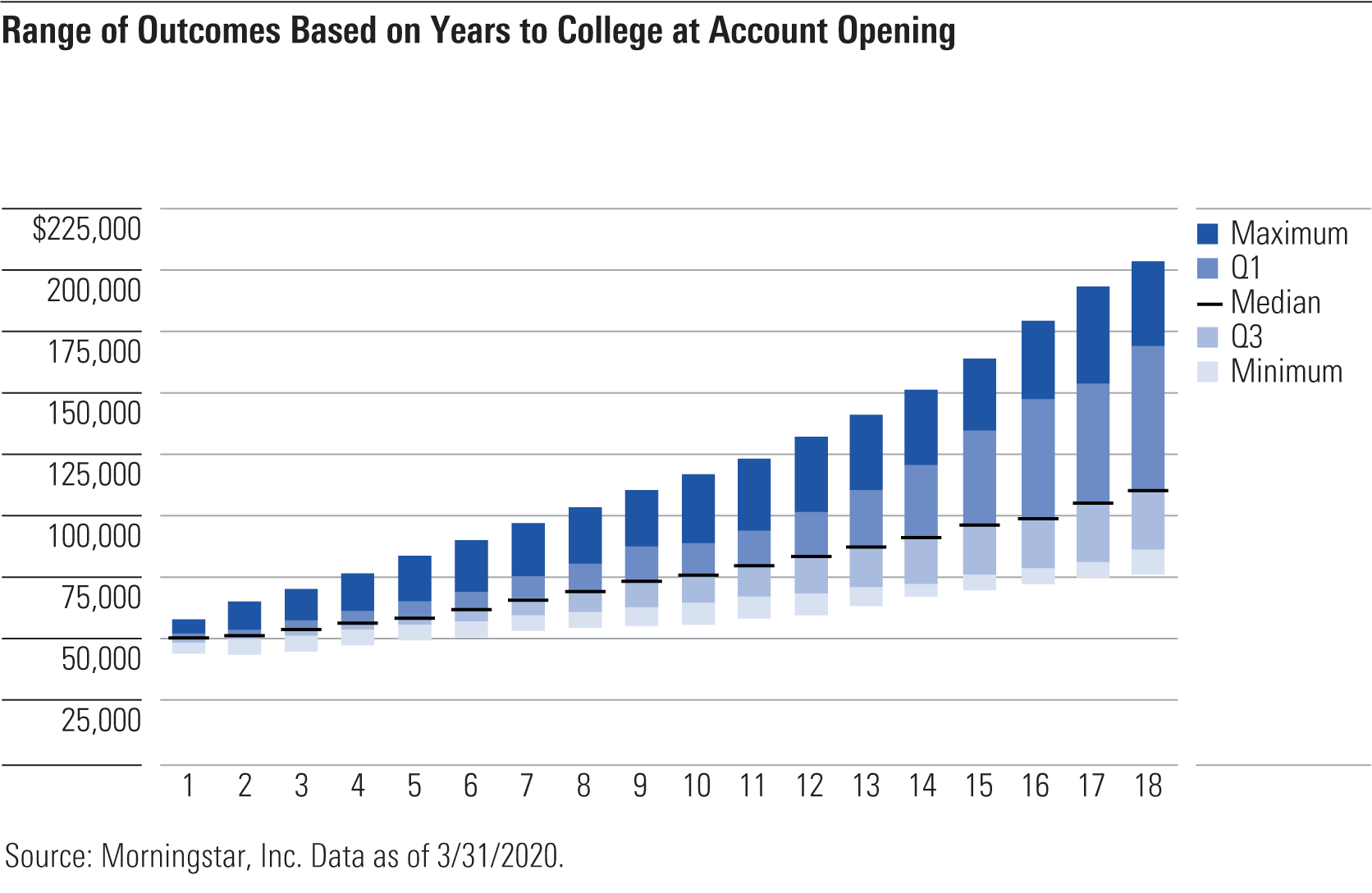

Should investors continue contributing if their 529 beneficiary has elected to delay college? Generally, yes. Our research finds that any year that investors do not contribute, they reduce the capacity for their savings to grow. The typical 529 saver opens an account when the beneficiary is 7 years old, with roughly 11 years for the contributions and returns to compound in the educational coffer. But if the 529 beneficiary delays use and the account continues to accrue value, the element of additional time can have a substantial positive impact. As an illustration, we assumed the college saver invested $50,000 in equal monthly contributions across different time horizons, and we used historical rolling returns dating back to 1976 to model the ending account balances depending on when the account was opened. The hypothetical portfolio split the stock allocation into 70% S&P 500 and 30% MSCI EAFE and fully invested the bond portion in the Bloomberg Barclays U.S. Aggregate Bond Index. We also assumed college savers did not reinvest their tax savings into the 529 plan. Within this situation, one additional year can increase the median ending account balance by up to $5,900.

What can an investor do with college savings if a 529 beneficiary chooses not to attend college at all? If a child makes the difficult choice to pass up postsecondary education or abstain from attending college altogether, there are several ways to repurpose the savings set aside in a 529 plan. Plans allow accountholders to change the beneficiary from one person to another, so if the former student has younger siblings then it can just be a matter of filling out a form.

But investors with no other potential future 529 beneficiaries to transfer to have reason to take heart. Congress has increased the potential uses for 529 plans in recent years. Now, 529 savings can be used to pay for apprenticeships in skilled trades. Balances can also be repurposed to pay off $10,000 of existing student loans, either for the intended 529 beneficiary or a sibling. Even if a child takes a nontraditional path toward education, college savings can evolve to meet those needs.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IGTBIPRO7NEEVJCDNBPNUYEKEY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/eda620e2-f7a7-4aef-bb6c-3fb7f1ac7a38.jpg)