The Rise and Fall of Bank-Loan Funds

A Morningstar Category grapples with its future.

/s3.amazonaws.com/arc-authors/morningstar/d70ff945-8520-4b27-9d10-eb509531f5aa.jpg)

Bank-loan funds have had a difficult time. The Morningstar Category has endured outflows since late 2018, and following the March 2020 sell-off, it has shrunk to its smallest size since 2012. And the category’s narrow return spread--a function of loans’ ties to rock-bottom short-term interest rates and limited upside because of call risk--means that fees eat up a larger percentage of returns than in many other categories and make it difficult for individual funds to separate themselves from the pack.

Meanwhile, the bank-loan market itself has evolved in a direction that has undercut its traditional role as a credit-sensitive asset with more resilience than high-yield bonds. In fact, the bank-loan sector's traditional downside protection versus high-yield has been eroding for some time. More than ever before, bank-loan investors must ask themselves what they want out of their allocation and whether bank-loan funds are still able to deliver it.

Going With the Flow Leveraged bank loans packaged for investors in closed-end funds and then interval-structured funds have been around for decades, but bank-loan mutual funds with daily liquidity are still a relatively new phenomenon. Because bank loans are not securities in the legal sense, and the process of trading them is more cumbersome, they tend to be significantly less liquid than most other fixed-income sectors, which makes placing them into daily liquidity vehicles a tricky proposition. Over time, market growth and a widening audience, combined with syndication and third-party arm's-length pricing, enabled their entrance into the open-end world, though their relatively less-liquid profile remains.

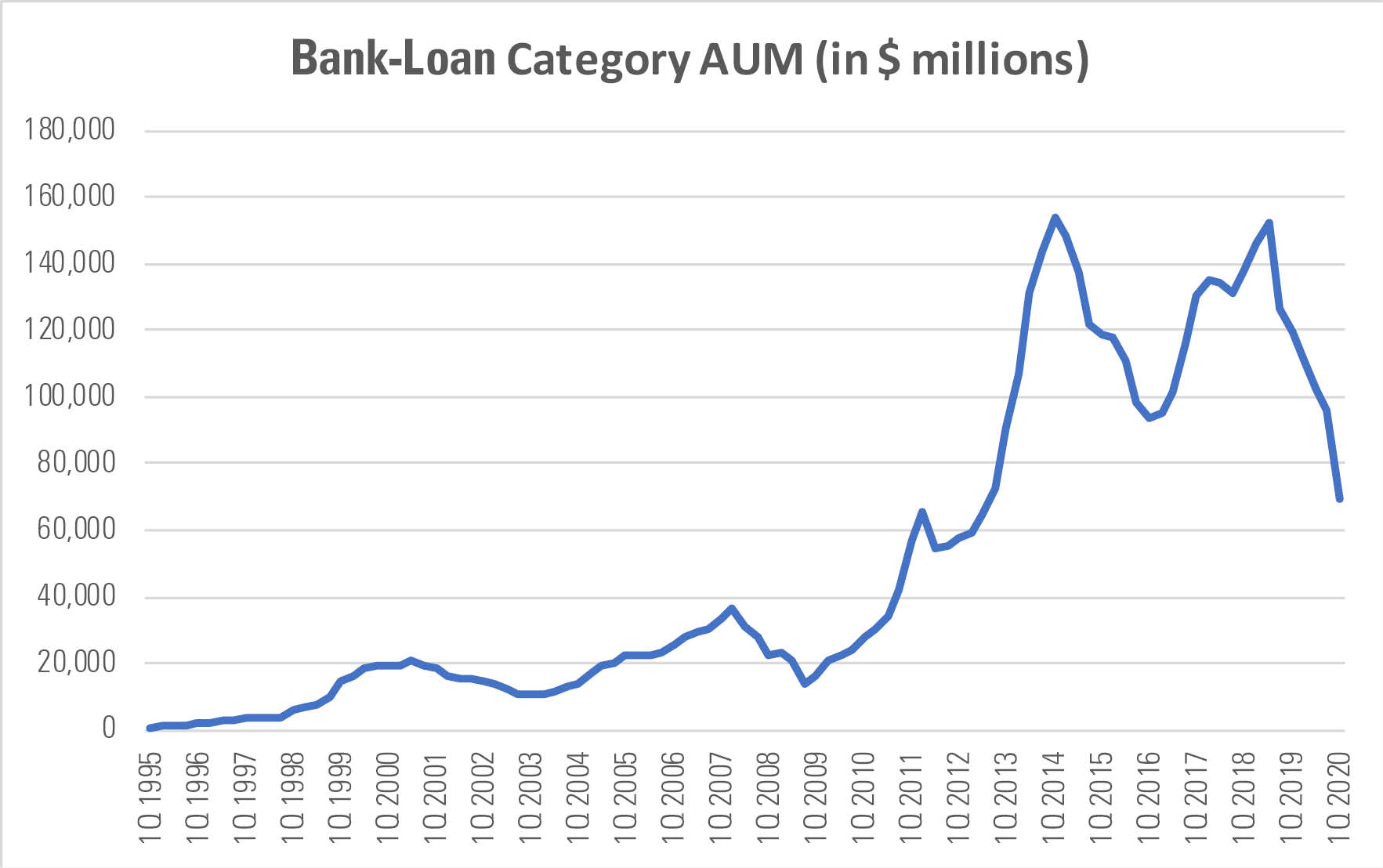

Including both exchange-traded funds and open-end mutual funds, the bank-loan category remained a comparatively small, niche market until 2013, when fear of rising interest rates led to a deluge of inflows. Bank loans pay a floating coupon that has historically been tied to Libor (a commonly used institutional short-term rate that's currently being phased out in favor of others), so the simple logic was that if rates rose, payouts would as well, and prices would remain stable.

This floating-coupon feature sets bank loans apart from most of the fixed-income market, and for a brief period bank-loan funds were the darling of the investment world. Investors plowed more than $67 billion into the category in 2013, and it effectively doubled in size to $143 billion by the end of that year from $72 billion at the end of 2012. Category assets briefly eclipsed $150 billion in early 2014, but the years since then have been a long slide back down to 2012 levels.

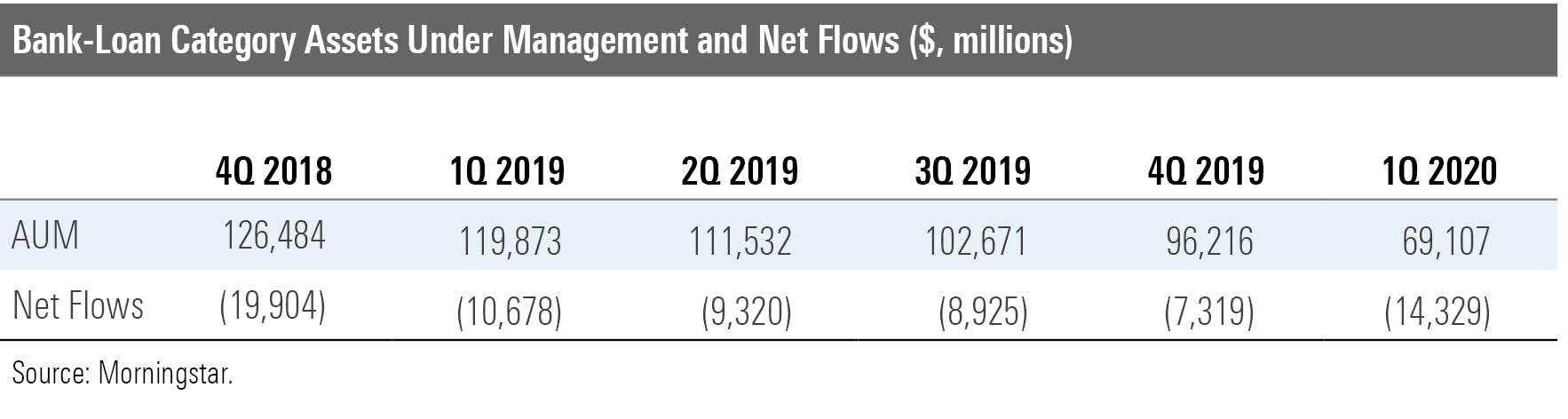

Source: Morningstar.

What's behind this decline? First, rising interest rates failed to materialize for much longer than many expected, while in 2014 and 2015, a commodity-driven bear market showed investors that the category was not impervious to credit volatility. Leveraged loans are senior in a company's capital structure but are typically extended to risky borrowers and invariably vulnerable in a credit crisis. After pumping in so much money in 2013, investors pulled $20 billion from the category in both 2014 and 2015.

Rising rates did materialize in late 2016, and they continued through 2017 and most of 2018. This led to a run of strong performance from bank-loan funds as previously tiny payouts began climbing while the market responded to borrowers' improving credit fundamentals.

Another defining feature of bank loans, though, is a lack of call protection. With almost no preconditions, bank loans can be refinanced at or near par to cut their interest costs. The ease of doing that is traditionally a function of a borrower's improving credit profile, but when there is significant demand and banks are eager to earn fees, borrowers can negotiate deals that are better for them than for investors.

This is significant because it limits the upside available to bank loans. Corporate bonds, both investment-grade and high-yield, typically come with call protections or make-whole features that allow them to trade above par value more easily, increasing their potential total return. But callability means that bank-loan upside is typically capped, while bond upside is not, so improving economic fundamentals--which tend to parallel rising short-term rates--can only go so far in terms of driving up a loan's price. For example, roughly 70% of bank-loan issuance activity in 2017 was used to refinance or reprice existing loans.

Rising interest rates--the primary reason bank loans are touted as an investment--became a moot point in late 2018. The Federal Reserve had aggressively hiked rates throughout 2018 until the perceived stress put on the economy led to a short but violent sell-off in the fourth quarter. In early 2019, just days after the New Year, the Fed reversed course and began a rate-cutting cycle. This blew up the primary thesis for owning bank-loan funds, and since then, the category has been in heavy and consistent outflows.

The category saw $36 billion of outflows in 2019, its worst year on record; that represented roughly 28% of assets from the start of the year.

A Changing Market Leads to Lower Recoveries There is also reason to believe that bank loans' traditional downside protection will not hold as strongly going forward. Huge demand for loans has fostered incredible growth over the years: In 2003, the total loan market was $148 billion, in 2008 it reached $600 billion, and in 2017 it crossed the $1 trillion mark. Private equity was booming while loans became an increasingly popular way to structure buyout deals driving up supply, while rapid growth in collateralized loan obligations fueled the demand side. Indeed, the CLO market--which packages pools of loans into securitized products that are then tranched much like a mortgage-backed security--grew from $19 billion of issuance in 2003 to $277 billion of issuance in 2018. In 2019, the total CLO market was roughly $600 billion, about half the size of the loan market.

Of course, massive growth in both supply and demand paved the way for a loosening of credit standards. As a result, a larger and larger percentage of the market is now made up of covenant lite and loan-only capital structures. The former are loans with limited protection for lenders, while the latter are businesses that lack a "traditional" capital structure that includes bond and equity investors with capital at risk ahead of loanholders. Because loans are senior to bonds in the capital structure, they should come out of bankruptcy restructurings with much higher recovery rates.

According to J.P. Morgan, covenant-lite loans accounted for nearly 84% of the outstanding loan universe, as measured by the JPMorgan Leveraged Loan Index. Prior to 2013, covenant-lite exposure was consistently below 20% of the market, but since that year, it has accounted for a majority of new issue volume, reaching a high point in 2018 at 87% of issuance. At the same time, a whopping three fourths of loan issuers are now loan-only, up from one fourth going into 2008. These developments carry significant implications.

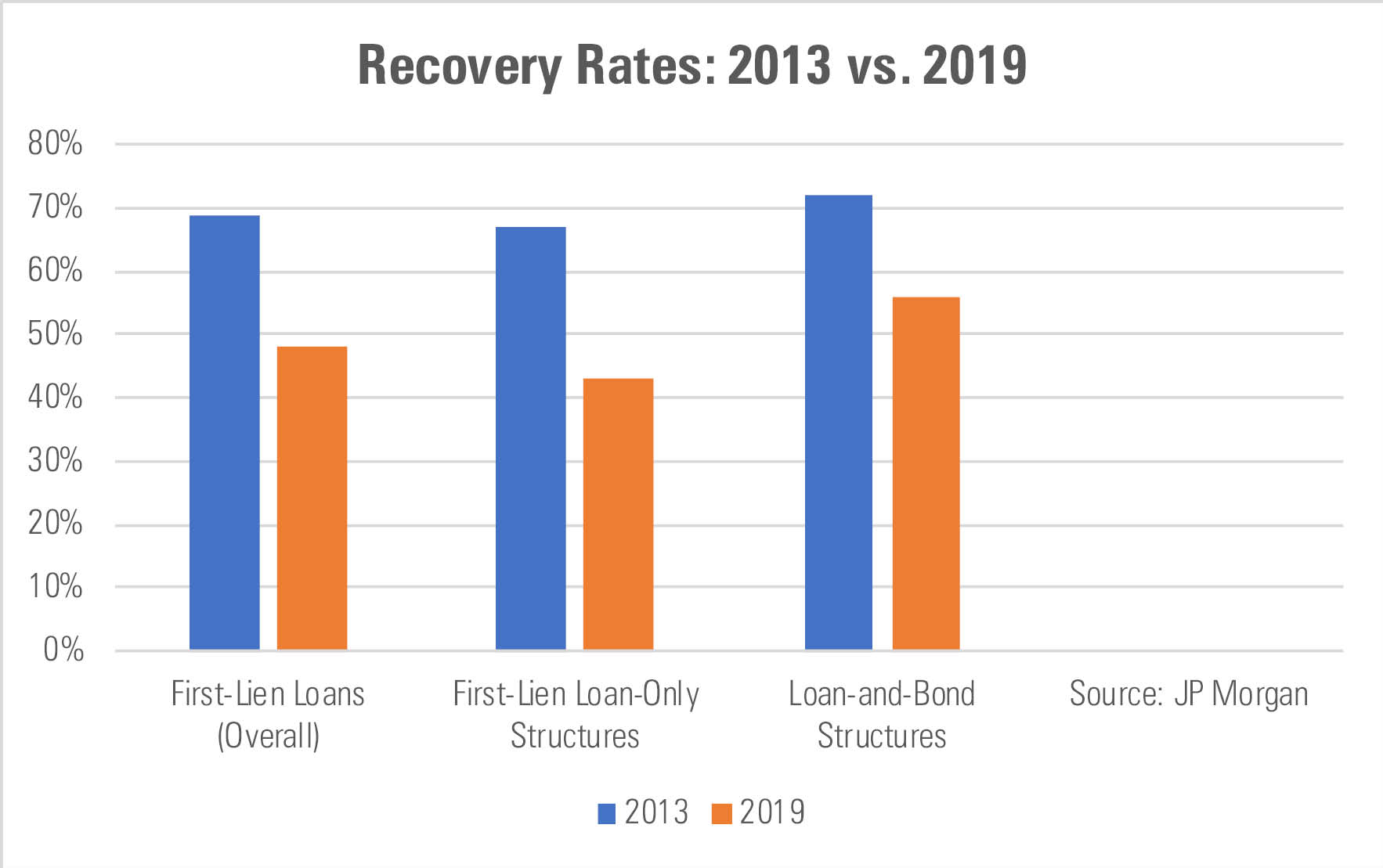

The biggest problem is much lower recovery rates. According to J.P. Morgan, the recovery rate on first-lien bank loans fell to 48% in 2019, its lowest point on record. Looking at the data comparing loans that sit atop capital structures that at least have bonds beneath versus those in loan-only deals tells a similar story. In 2019, the recovery rate for the former was 56%, while the first-lien loan-only recovery rate was 43%. Indeed, since 2008, loan-and-bond structures have consistently recovered more than loan-only capital structures.

As you can see from the exhibit above, recovery rates have fallen sharply across the board since the market's expansion began in 2013. That's a sea change in the entire structure of a loan market that provided 88% recovery rates in 2004. Falling recoveries carry significant implications for the loan market--worsening downside combined with a capped upside is not an attractive investment proposal.

Conclusion All of this means that bank-loan funds are in a tough place. If outflows continue, the category is likely to experience liquidations or mergers as asset managers shut down uneconomic products. Growth in both supply and demand has engendered changes that have weakened the sector's traditional downside protection. And the lack of call protection will remain an impediment to upside performance whenever credit markets rally, especially in a world of near-zero interest rates that neutralizes one of the sector's defining features and return generators. Given the disadvantages that the category faces, only the very highest level of team and approach--and low fees--can be expected to outperform.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OMVK3XQEVFDRHGPHSQPIBDENQE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/d70ff945-8520-4b27-9d10-eb509531f5aa.jpg)