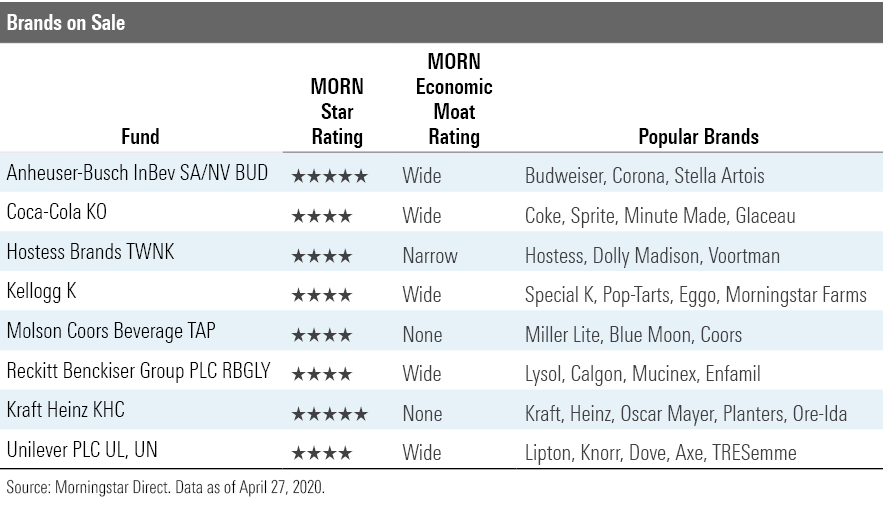

8 Cheap Stocks with Solid Brands

These consumer names are undervalued according to our metrics.

/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)

Editor's note: Read the latest on how the coronavirus is rattling the markets and what investors can do to navigate it.

During the coronavirus lockdown, we're cooking and cleaning more, according to a recent report in The Wall Street Journal. We're also grooming less and indulging in comfort foods from well-known brands. Bring on the mac & cheese!

With this shift in shopping habits in mind, today we're looking for consumer stocks with solid brands that are undervalued by our measures. Of course, which consumer trends will persist post-pandemic is up for debate. But these companies have the brand strength to endure no matter where consumer tastes go next.

We've recently talked about two of the names from the list: Coke KO and Kraft Heinz KHC.

Long-Term Value for Coke Despite Uncertainty

Kraft Heinz Sees Sales Gains, but Will It Last?

Here's a little bit about a few other companies on the list.

Anheuser-Busch InBev SA/NV BUD We recently trimmed our fair value on AB InBev, taking into account the effect we expect the COVID-19 crisis to have on short-term results. That said, we think the pandemic will have little long-term impact on the business and cash flows, reports director Philip Gorham. In fact, Gorham calls the stock "egregiously undervalued," given its wide Morningstar Economic Moat Rating and significant cost advantages.

Here's Gorham's take on the business overall:

"Anheuser-Busch InBev has one of the strongest cost advantages in our consumer defensive coverage and is among the most efficient operators. Vast global scale and near-monopoly dominance in several Latin American and African markets give AB InBev significant fixed cost leverage and pricing power in procurement, especially following the acquisition of SABMiller in late 2016. This plays out in the firm's excess returns on invested capital and best-in-class operating and cash cycles, asset turnover ratios, and working capital management. AB InBev delays payments to trade creditors more than 20% longer than its closest rival Heineken, and its free cash flow conversion has been consistently higher than peers in recent years. Driving AB InBev's profitability is its majority stake in Ambev, the Latin American brewer that generates a whopping near-40% EBIT margin in beer in Brazil.

"AB InBev has been acquisitive, having made transformative deals for Interbrew and Anheuser-Busch, and more recently acquiring Grupo Modelo, Oriental Brewery, and SABMiller. Management's playbook is to buy brands with a promising growth platform, expand distribution, and ruthlessly squeeze costs from the business. We think the acquisition of Modelo perfectly demonstrates the strategy. Corona is a premium brand, so it plays well in an environment of premiumisation in beer consumption. AB InBev can enhance profitability by removing duplicate costs, expanding volume (it has tripled Budweiser's volume in China in less than three years and has doubled its share in the United Kingdom), and bringing distribution in-house, thereby capturing the downstream margin opportunity. The risk to the strategy is that cost-cutting can go too far, and it is vital that the brands are supported with sufficient marketing spend to meet the increasing customer acquisition cost. Companies such as RB and Kraft Heinz (another 3G business) have suffered market share loss by failing to invest in the business. A lean cost structure provides the financial flexibility to compete on price, but the consumer in most consumer goods categories must be perpetually reacquired, and this requires an appropriate level of spending."

Dig deeper: Consumer Defensive: Uncertainty Creates Attractive Valuations

Hostess Brands TWNK We think Hostess' revenue will remain relatively stable though the COVID-19 disruption, says analyst Rebecca Scheuneman. We expect that purchases via grocery stores, mass retailers, and drug stores should offset potential weakness in convenience stores. We expect Hostess will continue to capture consistent market share gains.

Here's what Scheuneman had to say about Hostess in her latest report:

"Although the previous owners of the Hostess brand filed for bankruptcy in 2004 and 2012, we contend it was due not to a lack of brand equity but rather highly inefficient manufacturing and distribution systems, a powerful unionized workforce, and a high debt load. We believe the Hostess brand's demonstrated pricing power, selling at a consistent premium to its branded competitors, provides evidence of an intangible asset. In addition, we believe Hostess is a valued partner in the convenience store channel (supporting another facet of the firm's intangible edge), where the sweet baked goods category drives a material portion of channel revenue and Hostess is the market share leader. These competitive advantages lead to our narrow moat rating.

"Consumers' heightened focus on healthy eating has led to 1% average category growth for the sweet baked goods category. However, the Hostess brand has continued to grow, albeit at a decelerating pace, as it regains shelf space that was lost during its 2012-13 hiatus. We believe the firm has additional distribution gains to realize as its current market share is just 19%, lower than the old company's 23%. Further, Hostess' share is likely to expand beyond its prior peak, given its greater access to convenience, drug, and dollar stores (following enhancements to its distribution network) and club stores after a recent acquisition. Expansion into adjacent categories such as breakfast pastries and cookies should increase its reach.

"Hostess has created significant shareholder value via its disciplined acquisition strategy. Although the 2018 Cloverhill acquisition initially depressed margins, the business is now generating healthy profits, and the deal provided a breakfast platform and access to the club channel, where the firm is successfully expanding the Hostess brand. We think the January 2020 Voortman Cookies acquisition also adds material value, as the business' 5% sales growth boosts the firm's sales trajectory, margins are comparable with those of the highly profitable Hostess brand, and as the top-selling brand of sugar-free cookies, provides a brand to leverage in the growing better-for-you snacking segment."

Watch: 2 Consumer Defensive Brands Maintain Value Amid Uncertainty Unilever PLC UL, UN The pandemic knocked down volumes of the maker of Knorr soups, Lipton teas, and Dove skin products (among dozens of other brands) last quarter, leading us to slightly reduce our fair value estimate of Unilever earlier this month. We haven't changed our long-term assumptions, though, says Gorham, and we think the high-quality firm can defend its shelf space.

Here's Gorham's snapshot of the business:

"Amid fragmentation in consumer profiles and retail and marketing channels, along with lower barriers to entry for startups, most consumer staples multinationals are fighting strong organic growth headwinds, and many are cutting costs in order to spend to drive growth. With value growth in most categories currently running at little more than 2%, not all of the large caps will be successful in regenerating growth to the 4%-5% range they used to enjoy. In the case of Unilever, however, we think the management team is taking the right steps to reignite growth in some highly competitive categories.

"The law of large numbers is unfavorable for the large-cap consumer companies, and moving the needle on Unilever's EUR 50 billion top line in a low-growth environment is challenging, especially as growth is largely being driven by niche, local, and artisanal brands. Unilever has struggled to adapt its business model, with management recently admitting that in its strategy to give more product development autonomy to regional management, the company had lost focus on scalable innovation. We do not think this is a problem that will easily be solved and will require higher levels of customer acquisition spending, financed through cost savings from elsewhere.

"Strategies to streamline the cost structure include 5S, which is focused on supply chain and gross margin efficiencies; zero-based budgeting, which has replaced budgets and spending targets with operational KPIs and primarily focuses on marketing spending and overheads; and Connected 4 Growth, which has delivered a 15% reduction in middle and senior management.

"The financial targets accompanying these strategies include EUR 6 billion in cumulative cost savings by 2020, two thirds of which will be reinvested; a 20% operating margin and 100% free cash flow conversion; and increased acquisition activity and direct returns to shareholders. With a wide economic moat, built around its supply chain advantages, Unilever has a better chance than most of its peer group of reigniting growth in the medium term, in our opinion, but it remains in categories with relatively weak pricing growth drivers."

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IORW4DN3VVC3BC4JO7AQLSJTF4.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ODMSEUCKZ5AU7M6BKB5BUC6G5M.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TGMJAWO4WRCEBNXQC6RFO5TOAY.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)