Long Bonds and Gold as Portfolio Diversifiers

Should equity investors consider holding less of the former and more of the latter?

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

In Dissent Friday's column stated that, at current prices, long Treasury bonds are bought to be sold. Their yields are too meager to justify a 30-year investment. Instead, people own long bonds because they must (as with foreign central banks), as a tactical tool (as with professional managers extending their portfolio's duration), or with the implicit idea of trading them later.

A reader disagreed. Gabriel Adams wrote, “Long-term Treasuries can serve as an excellent diversifier in an equity-heavy portfolio. Absolute and risk-adjusted returns are improved by adding a long-term Treasury allocation. The results are compelling.” Viewed in isolation, long bonds aren’t pretty. However, they look decidedly more attractive when complementing an existing stock position.

That certainly has been the case, as long Treasuries have diversified equity portfolios exceedingly well. Mr. Adams suggested that a 10% to 20% position would provide a useful hedge. For this column, I tested a bolder strategy: swapping long Treasuries for the entire fixed-income portion of a traditional 60% stock/40% bond balanced fund portfolio. The results were indeed outstanding.

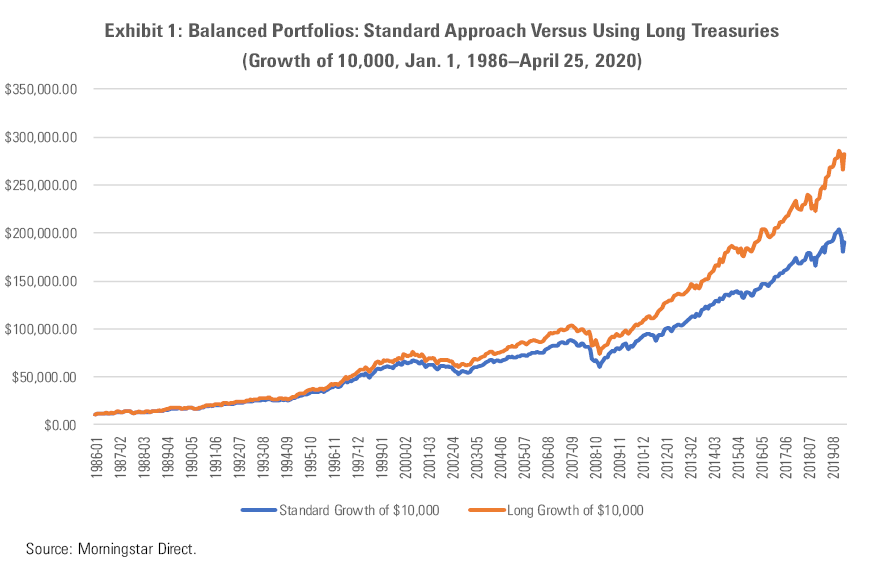

History's Lesson The chart below shows the growth of $10,000 for two portfolios, from 1986 through last Friday. The line labeled Standard carries a 60% stake in the S&P 500 (as represented by a proxy, Vanguard 500 Index VFINX) and 40% in an intermediate-term bond index, Bloomberg Barclays U.S. Aggregate Bond Index. The other line, called Long, holds the same equity position but substitutes Barclays Capital U.S. Treasury 20+ Year Index for the Aggregate Index.

The competition was a shellacking. Over the almost 35-year time period, the Long portfolio grew to almost $282,000, while the Standard portfolio lagged far behind, at just over $190,000. The annualized returns between the two portfolios were closer, but as Jack Bogle liked to remind audiences, small yearly improvements become large cumulative advantages when compounded over several decades.

Much attention, justifiably, has been paid to differences in equity strategies--active management versus indexing, domestic stocks or international, large-company stocks or those from smaller firms, value versus growth. Over time, such decisions strongly affected investor performances. However, so also did opting for long bonds rather than intermediate notes--but that choice is rarely discussed.

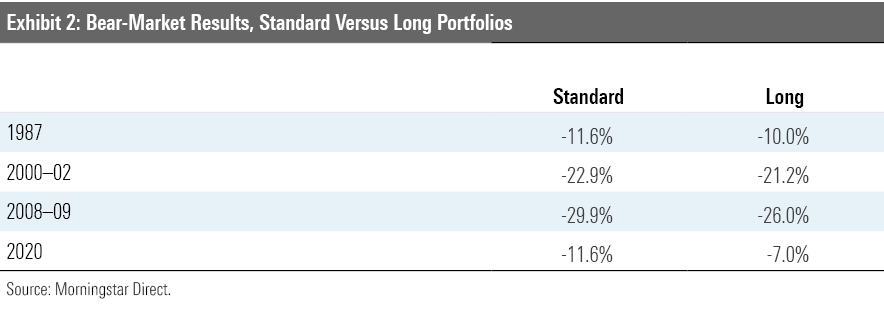

Twin Benefits Long Treasuries provided two benefits. First, they consistently answered the bell when stocks got clocked. The four worst periods for equities since 1986 have been: 1) October 1987, 2) September 2000 through September 2002, 3) June 2008 through February 2009, and 4) February 2020 through March 2020. On all four occasions, the Long portfolio withstood the downturn better than did the Standard portfolio:

Second, long bonds decisively outgained their intermediate-term rivals. In fact, a stand-alone investment in the Barclays Treasury 20+ Year Index would have almost kept pace with the Standard portfolio during the 1986-2020 time period. A $10,000 purchase of the long-bond index would have ballooned to $184,000, just short of Standard's $190,000 result. When your safe asset performs that well, you have lived La Vida Loca.

Now for the very large caveat. (Of which Mr. Adams is fully aware; he wrestles with the same issue.) Future long-bond performance will surely be far lower than that of the past. Thirty-year Treasuries yielded 9.28% in January 1986. Today, they pay 1.17%. Thus, the expected return for long bonds is 8 percentage points per year less than what one would have estimated in 1986. (A good estimate it would have been, as the Barclays 20+ Year Index gained 8.9% annually.)

In other words, adding long Treasuries to an equity portfolio once delivered diversification while preserving high returns. Now, possessing long bonds is akin to holding an insurance policy. To be sure, insurance can be a fine thing. It is at worst comforting to possess protection when stocks crash, and at best essential, should stocks not rebound. However, insurance does not come for free. It has a cost.

Considering Gold Shares Which led me to wonder: For those who do seek portfolio insurance, would supplementing long bonds with gold be wise? That tactic has never previously appealed to me because gold is an erratic diversifier. Might as well just own bonds, which diversify more reliably while offering similar (if not better) gains. With fixed-income yields so low, though, gold looks to have higher expected returns. Adding gold would therefore reduce the cost of the insurance policy.

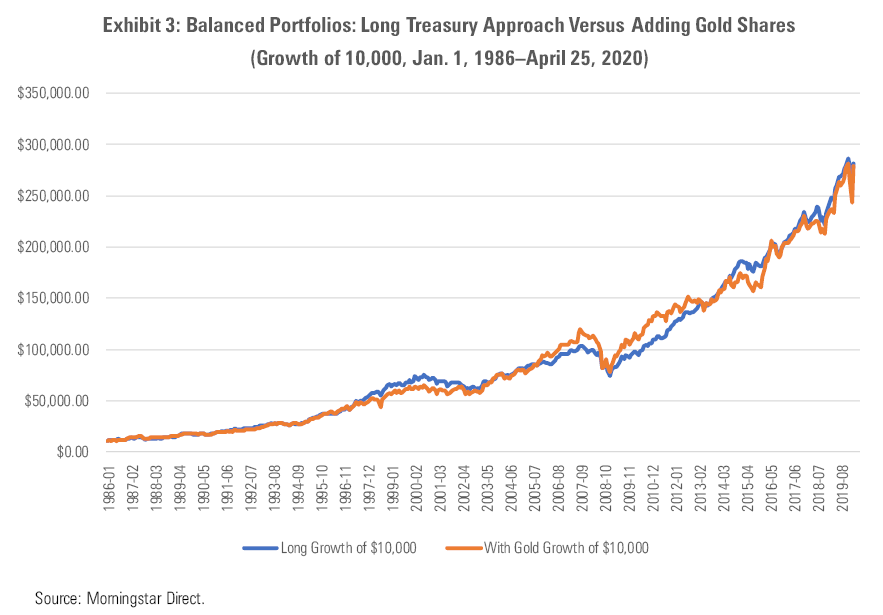

Such is the theory. Let's look at the history. I adjusted the Long portfolio by substituting Fidelity Select Gold FSAGX for half the bond stake. The new creation, dubbed the With Gold portfolio, consists of 60% Vanguard 500 Investor, 20% Barclays Capital U.S. Treasury 20+ Year Index, and 20% Fidelity Select Gold. The chart below compares its growth of $10,000 against that of the original Long portfolio.

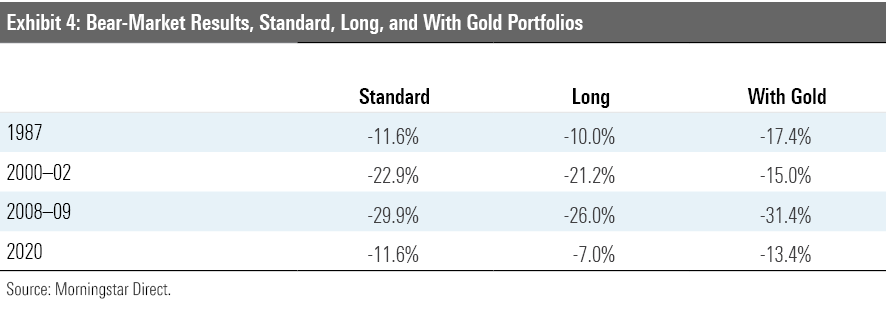

The final resting point is excellent. The cumulative gain for the With Gold portfolio was almost identical to that of the Long portfolio. However, With Gold’s run was considerably bumpier. In addition, the With Gold portfolio trailed both the Long and Standard portfolios during three of the four bear-market scenarios. The good news about gold is that its returns were uncorrelated with that of conventional equities. The bad news is that the correlation was not negative.

Over the surveyed time period, Long was clearly the superior portfolio. The two rivals ended in the same place, but Long did so with less drama, and it consistently protected against stock market declines. Equity investors would therefore have been served by skipping gold. The math is not so simple looking forward, though. There looks to be a trade-off. Holding long bonds alone will provide greater comfort but at what figures to be a steeper insurance cost. Adding gold shares could make sense for those who are willing to accept the higher volatility.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HTLB322SBJCLTLWYSDCTESUQZI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TAIQTNFTKRDL7JUP4N4CX7SDKI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)