ESG Proxy Resolutions Find More Support in 2019

But large fund companies often block their path.

Mutual fund companies backed proposals addressing sustainability concerns by the widest margin yet in 2019, but a lack of support from the largest U.S. fund managers kept many just short of winning a majority of votes.

Now, with BlackRock BLK signaling its intention to integrate sustainable investing across the firm's strategies and actively support climate-change-related shareholder proposals in corporate elections, 2020 could be a year when many more environmental, social, and governance resolutions pass with majority support.

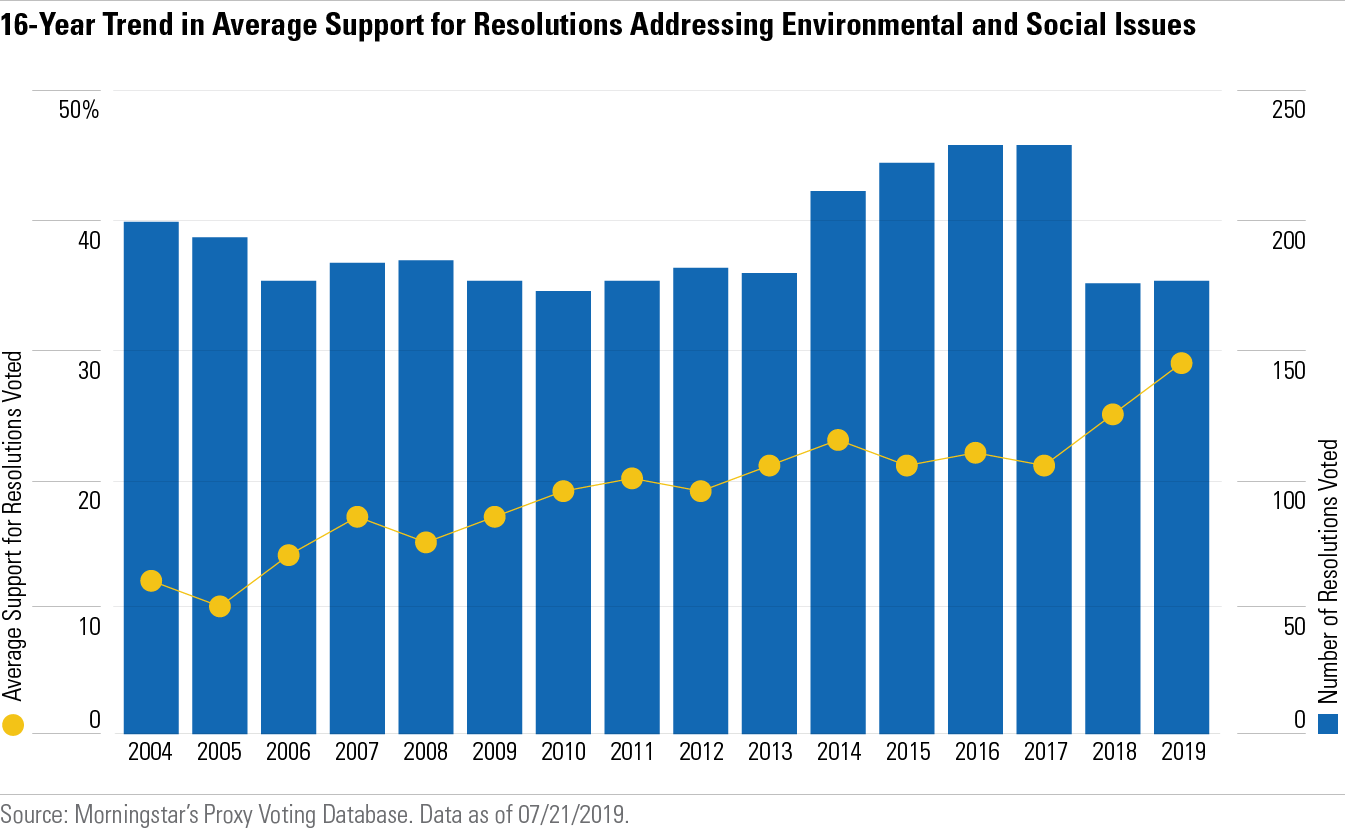

Morningstar's proxy voting coverage shows that investor support for ESG proposals reached an overall record high in 2019. ESG-related shareholder resolutions were supported, on average, by 29% of investor shares voted. The previous record high was 25% in 2018.

Among the 50 largest fund families, support for ESG-related shareholder resolutions hit 46%, up from 27% five years ago.

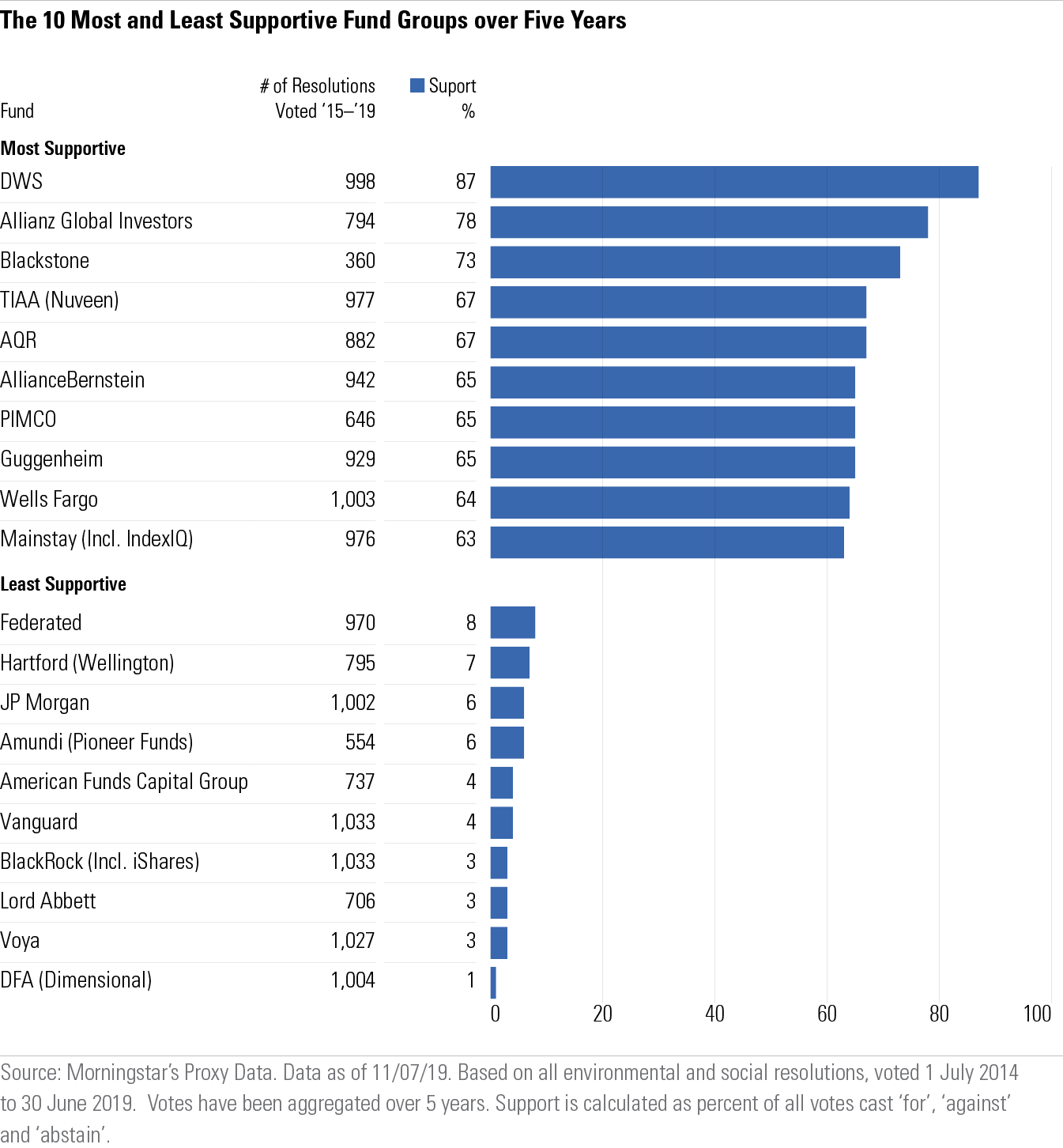

Funds offered by Allianz Global Investors, Blackstone, Eaton Vance EV, and Pimco were the most likely to support shareholder-proposed ESG resolutions in 2019, voting for these resolutions more than 87% of the time.

But five of the 10 largest fund families--Vanguard, BlackRock, American Funds, T. Rowe Price TROW, and Dimensional Fund Advisors--voted against more than 88% of ESG-related shareholder resolutions.

To some degree, large fund groups voting against ESG-related shareholder resolutions kept many of these initiatives from achieving majority support.

The 25 largest fund companies accounted for 82% of investors' assets in U.S. funds midway through 2019, which was up from 79% one year earlier. The largest five--Vanguard, BlackRock, Fidelity, American Funds, and State Street STT--controlled 56% of fund assets, or $10.7 trillion.

(Fidelity's index funds are run by its Geode unit and cast votes independently of the firm's actively managed funds.)

In a significant number of cases, a vote by just one large asset manager would have tipped the outcome on a resolution to a majority vote for the motion.

That's because for many public companies, a large fund group may own (on behalf of fundholders) 10% or more of shares outstanding. In 13 out of the 23 cases where an ESG resolution failed by 10% or less in 2019, Vanguard held a stake in the company of more than 10%. For BlackRock, this was true in four instances.

Of the 23 ESG resolutions that achieved between 40% and 50% support, 19 would have passed if supported by Vanguard, and 15 would have passed if supported by BlackRock. Four would have passed if supported by T. Rowe Price, and one would have passed if supported by J.P. Morgan. In at least three cases where Fidelity controlled more than a 5% stake, Geode voted Fidelity's index funds for the resolution, whereas Fidelity's actively managed funds voted against.

In the many other cases where a resolution failed to win a majority by more than 10 percentage points, most of the shares cast by managers other than BlackRock and Vanguard were for the proposal.

For example, had BlackRock and Vanguard voted their stakes in support of lobbying transparency at Exxon Mobil's XOM annual meeting in May 2019, that proposal, which earned 37% support, would have passed. Thirty one of 46 other fund families that held Exxon Mobil in one or more funds in 2019 supported this resolution.

Similarly, had the two largest fund providers supported a resolution calling for a workforce diversity report at Charles Schwab SCHW, it would have passed with 3 percentage points to spare. As it is, the motion received just short of 40% of the votes and was decisively supported by 30 out of 40 of the fund groups voting on it.

In recent weeks, both BlackRock and State Street signaled their readiness to use proxy voting to move the dial on sustainable business.

If the firms follow through, their votes could sway outcomes on some of the important issues that shareholders place on corporate ballots.

At the same time, other asset managers may be challenged to provide greater transparency into their voting strategies, key vote rationales, and overall stewardship approach as they compete for clients and investors.

But perhaps more significantly, this could result in corporate managements becoming more motivated to engage with investors, particularly broad-based investor coalitions on ESG issues, amplifying the impact of other investors' efforts.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/NNGJ3G4COBBN5NSKSKMWOVYSMA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6BCTH5O2DVGYHBA4UDPCFNXA7M.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EBTIDAIWWBBUZKXEEGCDYHQFDU.png)