Investment Signals Would Be Great, If They Worked

Their stories are compelling, but their results are not.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

False Prophets Two weeks ago, The Wall Street Journal posited that that money market assets might sustain the equity bull market. "Ready to Boost Stocks: Investors' Multitrillion Cash Hoard" notes that "nervous investors have socked away $3.4 trillion in cash. But stocks are rising and their nerves are calming, leading bulls to view the huge cash pile-up as a sign that markets have room to grow higher."

In other words, when investors put their money market holdings to work, stocks will advance. That sounds logical. But if money market outflows stimulate stock prices, then why haven't money market inflows caused the reverse? So far this year, money market funds have recorded their highest net sales since 2008, yet the S&P 500 is up 26%.

If this were my argument, and that was the response, I would immediately concede the point. However, those who champion investment signals are made of sterner stuff. Despite substantial evidence to the contrary, they continue to believe that the amount of money market assets, the rate of equity-fund inflows, and/or the direction of long-term demographic trends offer useful insights into future stock prices.

Unfortunately for the sake of investment simplicity, all three signals fail.

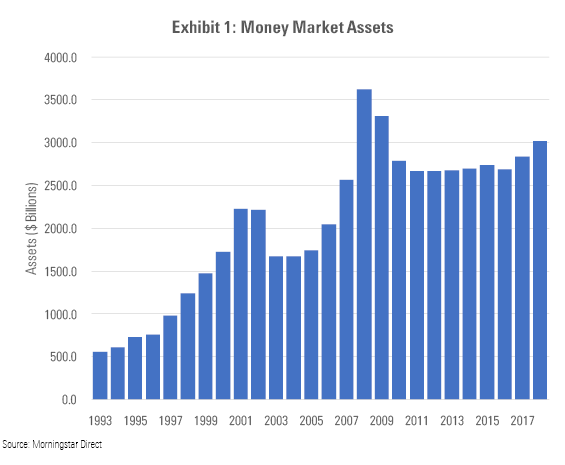

Cash Is Trash First, let's look at the money market indicator. It is alleged that high cash amounts presage stock-market success. Below are the year-end totals for money market assets since 1993.

The totals increased steadily from 1993 through 2001. Most of that period was a roaring bull market (save for 1994), followed by a severe downturn from spring 2000 through autumn 2002. Unfortunately, nothing in the money market figures distinguished the first era from the second. The pattern was the same throughout. Money market assets then bottomed in 2003 before gradually rising to an all-time high in 2007. Time to buy stocks? Quite the contrary.

By the end of 2008, money market assets had risen further yet, as investors fled to safety. One could argue, with the full benefit of hindsight, that all that cash helped to propel the ensuring bull market. I think that claim is actually correct. But how would one know that 2008's record wasn't another false alert? To answer my rhetorical question, one would not.

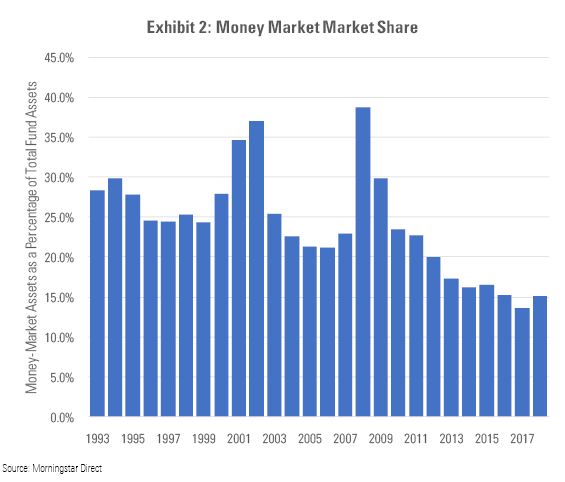

Perhaps raw assets is the wrong measure. Perhaps what matters is the relationship between cash and equity funds. The higher the percentage of cash when compared with equity-fund assets, the more fuel for the stock market. I reworked the first chart's calculation to be money market assets/equity-fund assets (counting both mutual funds and exchange-traded funds).

Nothing happening there, either. The 1999 percentage, before the big downturn, was the same as the 1996 percentage before the big upturn. Over the past few years, all percentages have suggested exiting the stock market. (The current "hoard" is only large by recent standards; for example, it is smaller than the money market percentage before the 2008 crash.) Not helpful!

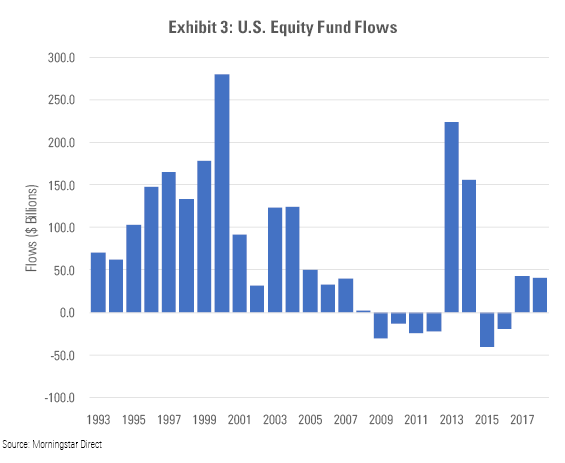

Stocks Are Also Trash The numbers also torpedo the common belief that equity-fund flows offer useful information about stock-market performance. The chart below depicts annual net flows into equity funds (again, both traditional mutual funds and ETFs).

Stock-fund inflows were positive during the 2000-02 bear market and negative for six of the past 10 years, which of course have been fabulous to equities. From the broadest perspective, the equity-flow indicator was incontrovertibly wrong. In recent years, it has behaved even worse: randomly. (Ultimately, all patterns are helpful. If a sell signal identifies securities that mostly perform well, then reverse the indicator. No such luck attempting to profit from randomness.)

For example, stock funds did receive large inflows during 2013, which has been the S&P 500's best year during the current bear market. Hurrah! However, stock funds suffered outflows in 2009, which was the next-best year. Another way of stating the confusion: Stocks posted similar returns in 2012 and 2014, although they experienced outflows during the former and high inflows during the latter.

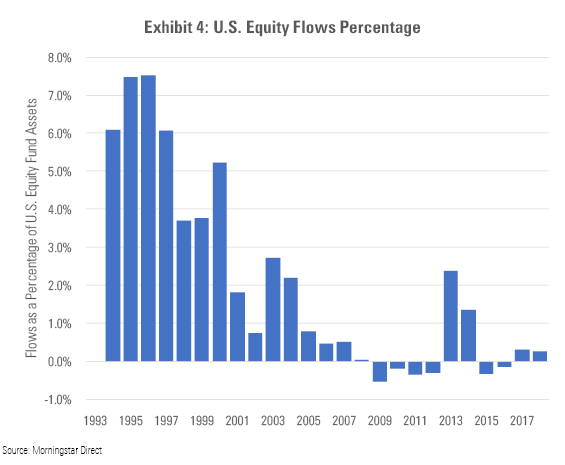

The mess doesn't improve when the calculation is reworked into a percentage. Indeed, the big picture becomes worse. Because today's stock market is so much larger than that of previous decades, equity-fund flows fade into insignificance. They are mice attempting to bump an elephant.

The Gray Wave The most specious of all signals is the one with the grandest aspirations: demographics. That developed countries' populations are already older than those of any previous civilization, and will become older yet, is indisputable. Also undeniable is the overwhelming effect that first-world aging will have on many industries. The U.S. healthcare business, for example, will continue to expand.

But translating this general knowledge into anything that might help investors-- anything at all--appears to be beyond anyone's ability. In the 1990s, the demographic arguments tended to emphasize American baby boomers, offering the simple explanation that boomers would push up stock prices until about 2010, then stocks would sink as they moved into bonds. More recently, the contention has been expanded to include international factors.

Either way, their predictions haven't panned out. By necessity, demographic forecasters were always vague about the timing, because demographic changes occur so gradually. Thus, even if they were correct, it's difficult to see how investors could profit from such knowledge. But they haven't been right even by the most generous assessments.

Someday, of course, stock prices will indeed plunge, and those who favor demographic explanations will assert that their predictions were finally vindicated. When that happens, their claims cannot be denied. Stocks don't talk; they can't explain why their prices change. Perhaps the demographic hypothesis will prove true. If so, that's for The Lord to determine. We mere mortals are best served by ignoring the discussion.

A Final Caveat I do not wish to overstate my case. The first two indicators could be useful. (Demographic data, not so much.) Evaluating money market assets and equity-fund flows won't help ordinary investors--whether defined as retail shareholders or the typical investment professional--achieve better outcomes, but they could benefit short-term trading strategies. Hedge fund managers often keep an eye on such numbers. It may be that some know how to use that information profitably.

If so, however, the signals' value is limited and specific. Such indicators cannot answer general investment questions.

John Rekenthaler has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T5MECJUE65CADONYJ7GARN2A3E.jpeg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/VUWQI723Q5E43P5QRTRHGLJ7TI.png)

/d10o6nnig0wrdw.cloudfront.net/04-22-2024/t_ffc6e675543a4913a5312be02f5c571a_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)