Making Retirement Work on a Tight Budget

With seven to 10 years to go until retirement, a pre-retiree assesses what adjustments are in order.

/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

This article is part of Portfolio Makeover Week 2019.

Cheryl, a 60-year-old single woman who works in the healthcare industry, is starting to think hard about the “what” and “when” of her retirement.

She hasn’t saved as much as she would have liked, but she’d also like to retire while she’s young enough to enjoy herself. A recent shoulder surgery gave Cheryl an appreciation for how precious it is to be active and healthy; now that she’s fully recovered, she’d like to seize the day. She has taken some great trips outside the country in recent years, and looks forward to the day when she can travel at a relaxed pace and also visit relatives out of state.

The big question that nags at her is how much longer she should wait. “I’d like to retire at 70--or sooner, if I can afford it,” she wrote. But Cheryl recognizes the financial benefits of delaying, too. She’ll receive about $2,500 from Social Security if she retires at her full retirement age--66 and 8 months--whereas her monthly benefit will jump to nearly $3,200 if she delays until age 70.

Cheryl’s employer also contributes 5% of her salary to a cash-balance plan--a type of defined-benefit plan--as long as she is employed there. While her cash balance in that plan is still fairly low--about $23,000--because she hasn’t been there a long time, those additional contributions could stack up. Cheryl’s employer also provides a 4.25% match on her 401(k) contributions. “My boyfriend tells me I probably need 10 additional years of savings and earnings on my retirement accounts,” she wrote.

In addition to considering her retirement date, Cheryl would also like guidance on her retirement portfolio’s positioning. Like many people in her situation, Cheryl struggles with how to balance the growth potential she needs against the risks that can accompany a more aggressively positioned portfolio. “On the one hand, I feel I need riskier investments as I think I need a lot more to be able to retire. On the other hand, I feel I cannot afford to lose what I've got,” Cheryl wrote.

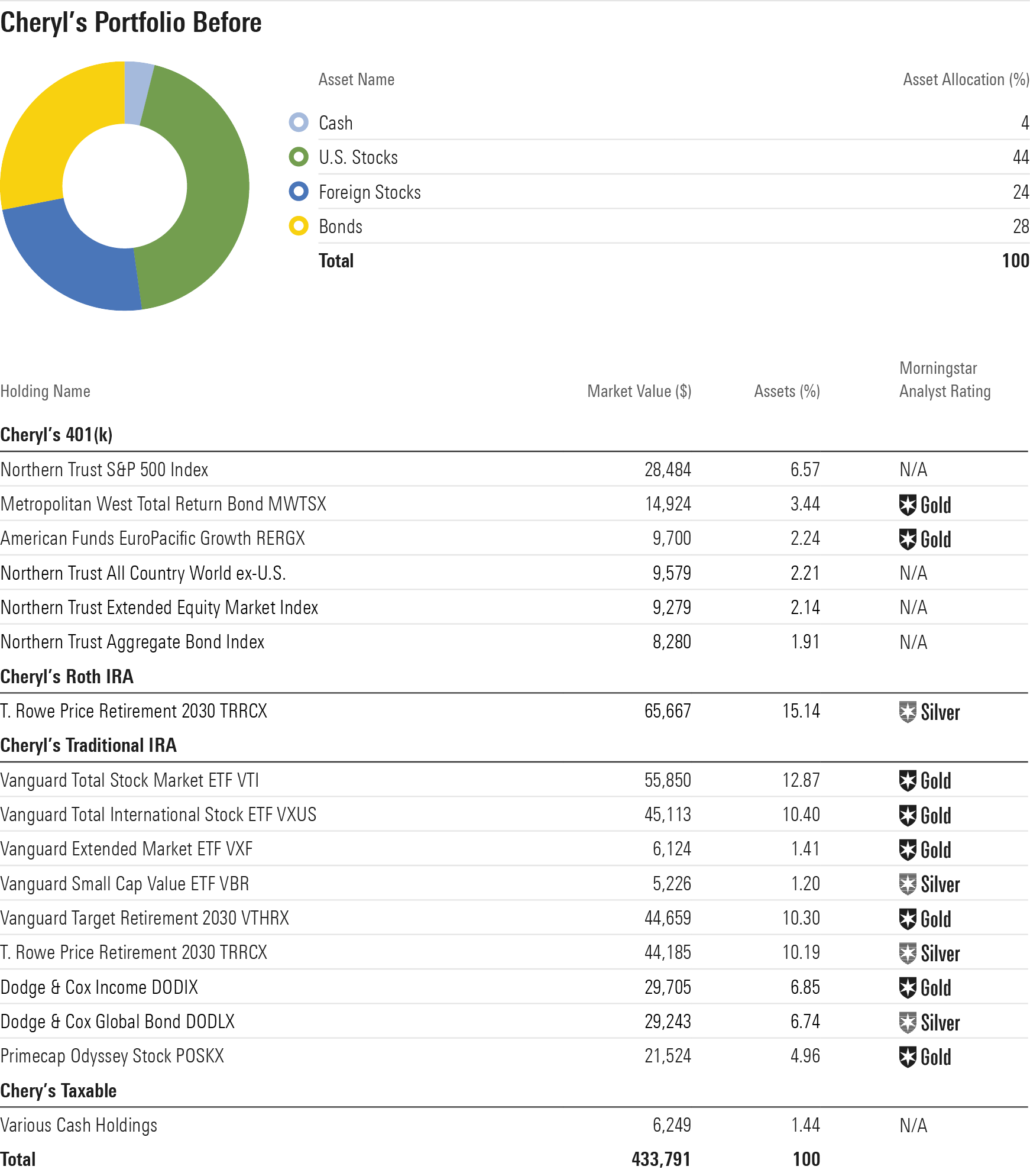

The Before Portfolio Cheryl's total portfolio is positioned fairly aggressively, with roughly two thirds of its assets in stocks, both U.S. and foreign, and the remainder in bonds and cash. (I didn't include Cheryl's cash-balance (pension) plan in that allocation because she doesn't control those funds; rather, I think it makes sense to indirectly factor a pension into asset-allocation decisions.) Because of her equity holdings' emphasis on index funds, her sector weightings and style-box allocations are quite close to what's represented in the market.

Cheryl holds her assets in a few silos. The largest is her Traditional IRA, which she rolled over from a former employer; it recently totaled about $280,000. Relying on guidance from her boyfriend, an avid Morningstar reader, she has assembled a portfolio that consists of low-cost exchange-traded funds and topnotch actively managed funds from Primecap and Dodge & Cox. In addition, her Traditional IRA includes 2030 target-date funds from both Vanguard and T. Rowe Price; those target-date funds earn Morningstar Analyst Ratings of Gold and Silver, respectively, from Morningstar’s analyst team. Cheryl also has a Roth IRA that consists of a single target-date 2030 fund from T. Rowe Price.

In addition, she’s contributing 13% of her salary to her workplace-provided 401(k) and getting matched another 4.25% on what she puts in. Cheryl’s 401(k) consists of fine, low-cost institutional share classes of mutual funds, as well as collective investment trusts that track various indexes and are managed by Northern Trust.

Finally, Cheryl has a small taxable account that holds cash. She recognizes that she needs a larger emergency cushion but raided her cash accounts and even racked up a little bit of credit card debt during her recent medical leave. (She currently has $3,800 on a credit card with a 0% interest rate, and plans to have it paid off before the teaser rate expires.)

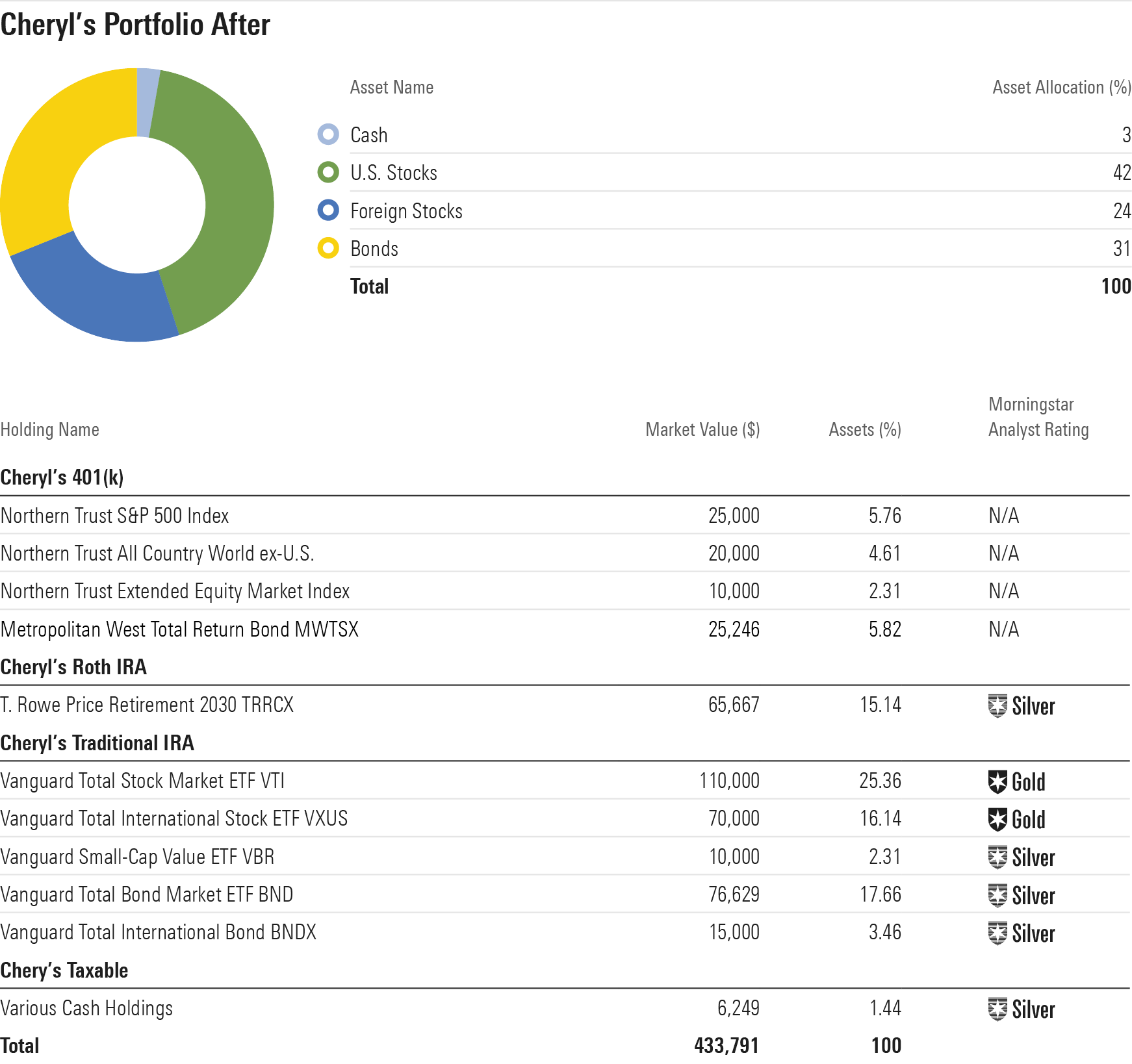

The After Portfolio By the numbers, Cheryl's goal of delaying retirement until full retirement age or beyond looks like a worthy one. If she can keep working another 10 years, continue to make retirement plan contributions, and receive employer matching funds, she could increase her total balance to about $900,000 assuming a 5% rate of return. Of course, a 5% return for balanced portfolio may be a bit optimistic for the next decade. If I haircut that to a more conservative 3%, her portfolio value would be worth about $750,000 10 years from now, assuming the same monthly contribution schedule. She'd have $75,000 in her cash-balance plan, assuming that her employer continues to make contributions and her money compounds at a 2.5% interest rate.

The really big-ticket benefit that comes along with delaying retirement is that Cheryl’s enlarged Social Security payments will reduce her eventual portfolio withdrawals, improving her plan’s sustainability. If she waits until age 70 to claim benefits, she’ll receive $38,400 in year 1. Assuming 2% annual salary adjustments over the next 10 years, Cheryl’s ending salary will be about $100,000. Income replacement rates are highly individual-specific, but I used 80% of her ending salary, or $80,000. That means that the remaining $42,000, above and beyond what Social Security provides, will need to come from her portfolio. And because most of Cheryl's assets reside in tax-deferred accounts she'd need to withdraw about $47,000 from her accounts to arrive at $42,000 on an aftertax basis, assuming a 12% tax rate. That’s a 6% withdrawal rate on an $825,000 portfolio (assuming a 3% rate of return on her 401(k) and an additional $75,000 in the cash balance plan) and a 5% withdrawal rate on a $975,000 portfolio (assuming a 5% rate of return on her 401(k) and an additional $75,000 in the cash balance plan).

By truncating the time horizon--assuming retirement at age 66 and 8 months--Cheryl’s plan looks riskier because her withdrawal rate goes even higher. Moreover, her Social Security benefit would be lower, assuming she files for Social Security at the same time.

Of course, Cheryl also has other options. If she decides to retire before age 70 or needs to do so, for example, she can still delay Social Security. That will mean that she withdraws more aggressively in the early years for retirement but could be advantageous in the long run because she'll have enlarged her benefit over her lifetime. Additionally, Cheryl can also take steps to drive her budget down so that she needs less than 80% of her ending income. And regardless of when she retires, one of the best things she can do for her plan is to be conservative about her initial withdrawal rate, especially if it coincides with a weak market environment. The fact that her apartment is rent-controlled helps ensure that the largest line item in her budget won’t skyrocket, but Cheryl will need to keep a tight watch on total spending to ensure that enough of her portfolio is in place to recover when the market eventually does.

Even though delaying retirement is a worthy goal for Cheryl, it still makes sense to create a backup plan in case she can't. After all, research from Morningstar Investment Management's head of retirement research David Blanchett suggests people often retire earlier than they expect to. Thus, it's not too early to do some preliminary "bucketing" of her portfolio, to help ensure that she wouldn't have to tap her equity assets amid a downswing for stocks. Cheryl's starting asset allocation--roughly two thirds equity, with the remainder in cash and bonds--is quite reasonable given a 10-year horizon. She has at least a few years' worth of withdrawals in safe assets to draw upon if her retirement happens to coincide with a weak equity market.

Nonetheless, some of her bond holdings are embedded in the target-date funds in her IRA portfolio. That means that if she needed to raise funds from her portfolio for living expenses, selling the target-date funds would entail selling pro rata allocations to stocks and bonds rather than spending exclusively from the bond holdings.

To help address this issue, my “After” portfolio jettisons those otherwise-solid target-date funds in Cheryl’s IRA in order to ramp up positions in dedicated bond funds that can provide her spending assets if she retires earlier than she expects. In Cheryl’s IRA, I cut the target-date funds, as well as Dodge & Cox Income DODIX and Dodge & Cox Global Bond DODLX. (It’s also worth noting that it usually doesn’t make sense to hold other assets alongside target-date funds in the same account, in that those extra positions can undermine the asset allocation embedded in the target-date vehicle. In other words, hold target-date fund or discrete stock/bond funds, not both.) I swapped in Vanguard Total Bond Market ETF BND and Vanguard Total International Bond ETF BNDX. While all the holdings in her “Before” portfolio are superb, my goal was to make the bond stake more “vanilla” in an effort to diversify the equity risk of the portfolio. I retained Gold-rated Metropolitan West Total Return Bond MWTSX in her 401(k); it’s especially attractive at an expense ratio of 0.37%.

Reducing costs and idiosyncratic risk colored my approach to the portfolio’s equity exposure, too. For example, I stuck with a non-U.S. index fund for foreign stock exposure in Cheryl’s 401(k), and I also employed index funds for equity exposure in her IRA. While it pained me to cut the otherwise excellent Primecap Odyssey Stock POSKX, it’s a very aggressive fund. Moreover, Cheryl’s “Before” portfolio had a slight emphasis on the large-growth square of the Morningstar Style Box, adding to its risk. I retained a small position in Vanguard Small Cap Value ETF VBR.

I also retained Cheryl’s Roth IRA position in T. Rowe Price Retirement 2030 TRRCX; for a smaller account like that one, it makes sense to employ a single fund with a lot of diversification.

Cheryl’s plan to pay off her credit card during the “teaser” period of 0% interest rates make sense; she should plan to retire that debt on schedule. In addition, I’d like to see Cheryl set a goal of raising her cash reserves to a minimum of three months’ worth of living expenses, to help ensure that she won’t need to rely on credit cards to tide her through unanticipated expenses.

Amy Arnott, Jess Liu, Chris Margelis, and Michael Schramm contributed to this report.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CGEMAKSOGVCKBCSH32YM7X5FWI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LUIUEVKYO2PKAIBSSAUSBVZXHI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)