Vanguard Won the Loser's Game

How an outsider conquered the fund industry.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Reaching the Top That Vanguard might eventually become the largest fund company is not startling. Thirty years ago, when Vanguard wasn't among the 10 largest mutual fund sponsors, it had nonetheless established the industry's strongest brand. Competitors advertised their mascots--lions here, bulls there. Vanguard didn't bother with such fluff. Instead, it painstakingly differentiated its contents.

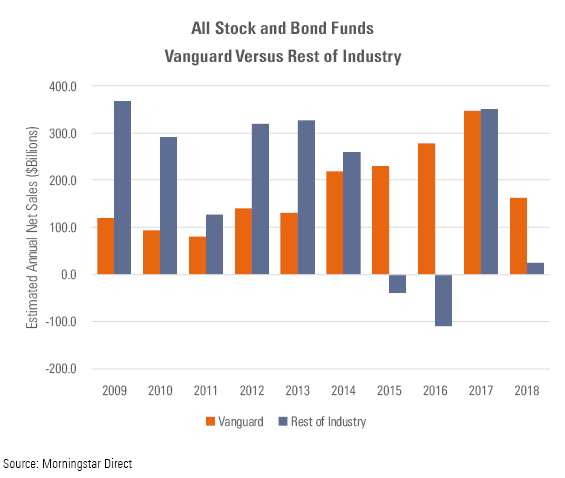

Eventually, investors noticed. The first of this article's three charts compares Vanguard's annual net sales (including exchange-traded funds, but excluding funds-of-funds so as not to double-count transactions) against those of all its rivals combined.

(Better than measuring net amounts would be separately assessing 1) gross sales and 2) redemptions, to determine how much of Vanguard's success has come from 1) attracting new assets as opposed to 2) retaining shareholders. But, as an outsider, Morningstar cannot obtain such information. The best it can do is to estimate monthly net sales, which are calculated from a fund's starting assets, ending assets, and monthly performance.)

The 2008 financial crisis was Vanguard's sweetest pain. By and large, its equity funds didn't outperform the mutual fund (and ETF) averages--but that counted as a victory, as the same applied to their actively run adversaries. Roughly speaking, all stock funds went down together. Active managers had long promised that when a bear market finally arrived, that they would outperform Vanguard's fully invested index funds. It did, and they did not.

Neither did they beat Vanguard's actively managed funds. With both equities and fixed income, Vanguard invests conservatively, eschewing complex strategies and, with bonds, favoring higher-credit securities. Such an approach steered it clear of 2008's headlines. To be sure, many Vanguard funds lost money, some heavily, but none significantly more than one might have expected. There were no unpleasant surprises.

Getting Better (All the Time) All that explains the chart's first five years, from 2009 through 2013. Entering the period, Vanguard was already among the sales leaders. Navigating the worst investment climate in decades further boosted its reputation. Before 2008, the company had received about 15% of the industry's net sales. After that year, its share doubled, to roughly 30%. Vanguard had entered uncharted territory.

This, it turned out, was only the beginning. In 2014, the company's business surged again, as Vanguard became the first fund company to claim more than $200 billion in net sales. In the process, it almost matched the total for all its rivals. Vanguard then broke its own sales record in each of the next three years. Over the ensuing half-decade, the firm took in $1.2 trillion, as opposed to $500 billion for all other fund companies combined. Seventy percent of all net sales!

Why the second outburst? Vanguard's initial advance owed to its 2008 performance, but subsequent markets have provided no such drama. The reason Vanguard's sales have become stronger can't be explained by the company's ability to navigate difficult investment markets.

Rather, the success owes to two factors. First, equity sales have increased, and Vanguard's market share is higher for stock funds than for bond funds. Second, Vanguard is gaining ground with bond funds. It's not there yet, but it has shown indications that its bond funds may yet become as popular as its stock funds.

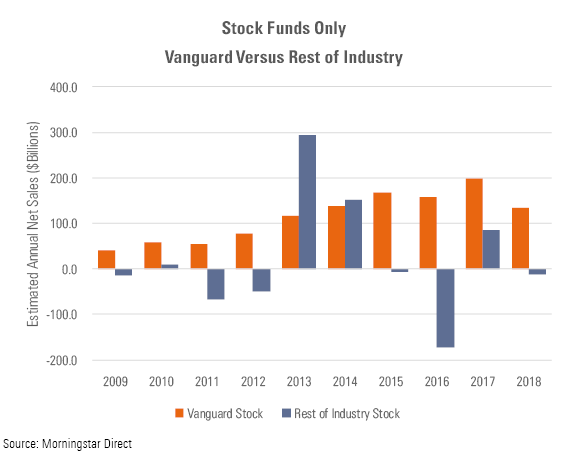

Stock-Fund Domination Here are results for the past 10 years' stock-fund sales, again including ETFs but excluding funds-of-funds.

The first word that comes to my mind is "despotic." Vanguard controls stock-fund sales thoroughly and utterly. Others enjoyed a short respite in 2013-14, when they collectively outsold Vanguard's equity funds, but otherwise they have been battered. During the remaining eight years of the period, their stock funds suffered net redemptions, while Vanguard's stock funds enjoyed high and growing inflows.

With stock funds, Vanguard did not consume more of the pie as the decade progressed, but the pie expanded. The category was barely positive from 2009 through 2012 but has since attracted at least $100 billion per year, with the sole exception of 2016. The better equity-fund sales, the better for Vanguard.

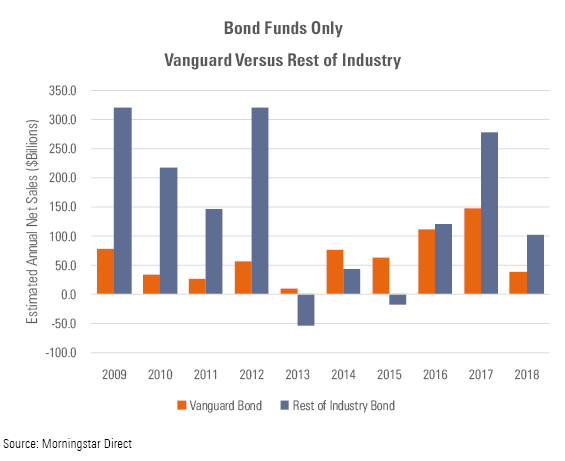

Bond-Fund Improvement In contrast, bond-fund inflows have somewhat declined from their post-2008 days, although they remain sturdy. What has changed is Vanguard's market share. The company's portion of fixed-income sales was modest in the early years but gained momentum as the decade progressed. Vanguard sold more bond funds even as its competitors sold fewer.

Once again, Vanguard benefited from misfortune, although in this case the affliction was more perceived than actual. Its increased bond-fund success coincided with the fuss at PIMCO Total Return PTTRX, then the world's largest bond fund, which had spooked investors by divorcing its lead manager and firm co-founder Bill Gross even as its performance dipped. The incident cast doubt on ambitious bond funds. Perhaps those that followed the straight and narrow were preferable.

(Advice to fund companies: Stagger your problems. Don't post bad results during the bad news. Shareholders will dismiss the headlines if the numbers are strong and will hold tight during the tough periods if the story stays intact, but suffering the two fates at once is incurable. PIMCO Total Return has lost 75% of its assets since 2014, despite outgaining the category average.)

The Loser's Game The causes were different--the entire world's financial crash for stock funds, and the travails of a single (albeit highly prominent) rival for bond funds--but the outcome was identical. The struggles of actively run funds that had made grand promises highlighted the virtues of Vanguard's comparatively modest approach. Bland became fashionable.

In 1975, the year of Vanguard's inception, the consultant Charley Ellis shocked professional investors by informing them that their best chance of winning was in not losing. The more chances they took, the greater the possibility that they would harm themselves by making critical mistakes. Counseled Ellis, "Don't do anything because when you try to do something, it is on average a mistake." Investment management was a loser's game, where highly skilled participants battered each other senseless. The winners were those who avoided the fracas.

Nobody has done that better than Vanguard.

John Rekenthaler has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IGTBIPRO7NEEVJCDNBPNUYEKEY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)