When to Start Saving for College

What do college savers miss when they put off investing in a 529 plan?

/s3.amazonaws.com/arc-authors/morningstar/eda620e2-f7a7-4aef-bb6c-3fb7f1ac7a38.jpg)

/s3.amazonaws.com/arc-authors/morningstar/96c6c90b-a081-4567-8cc7-ba1a8af090d1.jpg)

Earlier this week, Morningstar released its annual list of the best 529 college savings plans of 2019, but choosing the right plan by itself doesn’t ensure success. Time is also crucial because college savers who start early have more time for their investments to compound and typically gain exposure to portfolios with higher growth potential. However, in the process of updating our 529 plan ratings, Morningstar analysts found that the average college saver doesn’t open a 529 account until their beneficiary is over 7 years old. So, what does a late start mean for beneficiaries?

A Day Late and a Dollar Short The most popular option within 529 plans is the age-based portfolio, an investment that automatically shifts from stocks to bonds as the beneficiary ages. Most 529 plan program managers designed the tracks of their age-based portfolios under the assumption that college savers invest for 18 years, from the beneficiaries' birth until college age. These portfolios take on risk early, allocating heavily to stocks to increase the assets' growth potential. The industry-average age-based track starts with an 83% allocation to stocks when the child is born, gradually reducing to around 67% at age 7.

College savers who start investing in 529 plans later miss out on the equity-heavy portfolios with the most growth potential. While stocks are certainly more volatile than bonds, they have greater return potential over the long run. Each year that investors wait lowers the growth potential of their savings as age-based portfolios gradually de-risk.

To make matters worse, college savers who invest late into a 529 plan also miss out on the benefits of compounding returns as their investment horizon shortens. College savers may be tempted to make up for lost time by making large contributions or taking on additional risk in their portfolios, but it is hard to make up for years of missed compounding, underscoring the virtue of saving for college as soon as possible.

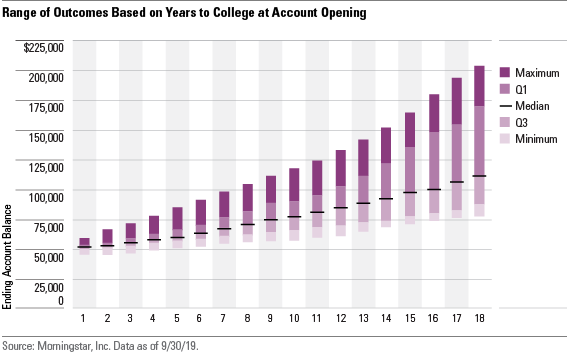

What’s the opportunity cost of starting late? Assuming a $50,000 investment spread out into equal contributions across different time horizons, we used historical rolling return data to model the ending account balances of savers depending on when they started. To replicate an age-based portfolio, we constructed a costless portfolio of market indexes that matched the industry’s average equity and fixed-income allocations over 18 years. The equity exposure in our hypothetical portfolio was split 70% S&P 500 and 30% MSCI EAFE, and the bond portion was 100% invested in the Bloomberg Barclays U.S. Aggregate Bond Index. We also assumed college savers did not reinvest tax savings into the 529 plan. Exhibit 1 shows the range of ending account balances.

- source: Morningstar Analysts

Even starting one year earlier can significantly increase a college saver’s ending account balance when it’s time to pay for college. This holds true for investors whether they start early or late. And while it is easy to assume that investing for 18 years would yield a higher account balance than investing for only a single year, we also see meaningful differences for every additional year an investor waits. For college savers who start at age 7 (or 11 years until college), a median account balance of $80,968 may seem like a fine return on their investment of $50,000. However, they missed out on another $3,980 that they would have earned if they had opened their 529 college savings account a year earlier--and nearly $30,000 if they had opened the account when the child was born.

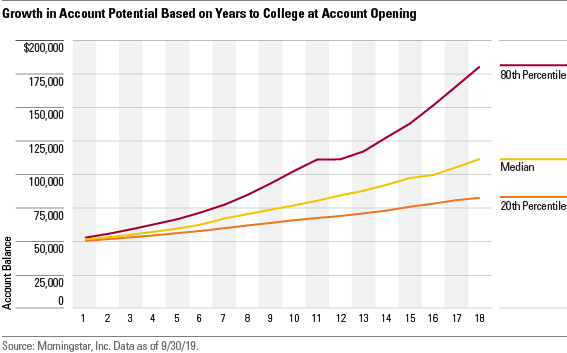

The Early Bird Gets the Return College savers that begin early also benefit more from the likelihood that markets rise. Using the same approach from the previous exhibit, Exhibit 2 highlights that early savers have a lopsided advantage since historical market returns skew positively, meaning that there are more dramatic outliers on the upside. Compounding returns magnify the effect that skew has on ending balances, and as a result, the spread between the 80th-percentile outcome and the median widens more than the spread between 20th-percentile outcome and the median. Investing heavily in equities and the compounding returns drive the higher balances for proactive college savers that started early.

- source: Morningstar Analysts

The sharpest increase in the 80th-percentile outcome starts 12 years prior to enrollment. That is, if families invest in 529 plans when their children are 6 years old or younger, the potential upside for the ending balance increases dramatically. If they began investing 18 years before college enrollment, the 80th-percentile outcome produced an ending account balance of $181,110, nearly $70,000 above the median outcome. At the opposite end, if families’ initial investments were made only one year before the beneficiaries hits college age, the 80th-percentile outcome of $53,398 nearly matched the median outcome of $52,217.

Starting to save for a child's education early will pay off with higher balances at college age. If you're having trouble sifting through the plethora of plans offered by 49 states and Washington, D.C., check out Morningstar's 529 plan center to get started.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IGTBIPRO7NEEVJCDNBPNUYEKEY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/eda620e2-f7a7-4aef-bb6c-3fb7f1ac7a38.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/96c6c90b-a081-4567-8cc7-ba1a8af090d1.jpg)