Utilities: Surging Sector Could Keep Its Rally Going

If interest rates keep heading toward zero, utilities could benefit.

/s3.amazonaws.com/arc-authors/morningstar/ea0fcfae-4dcd-4aff-b606-7b0799c93519.jpg)

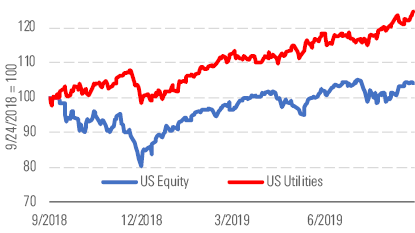

Utilities and their investors have little reason to complain. The sector is up 25% year to date, outstripping the broader U.S. equity market (up 20%) and all sectors except communication services, technology, and real estate. Falling rates mean ample cheap capital for a sector that has the second-largest debt appetite behind financials. Nearly all U.S. utilities have good three-year growth prospects, secure dividends, and sound balance sheets.

Utilities just keep going and going and going. - source: Morningstar

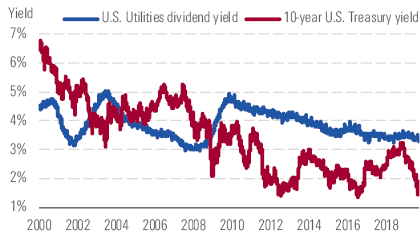

If interest rates keep heading toward 0% and investors continue favoring domestic businesses, utilities could keep rallying. A lot. The average U.S. utilities sector dividend yield at 3.3% is 160 basis points higher than the 10-year U.S. Treasury yield as of late September. The yield premium last reached this level in mid-2016. Utilities were up 13% one year later and 17% two years later even while interest rates doubled.

Hard to find anything cheap in the utilities sector. - source: Morningstar

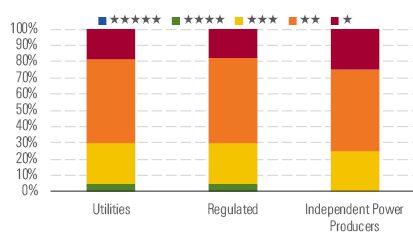

That said, relative to the long-term cash flows these businesses are likely to generate, prevailing prices look rich. The median utility under Morningstar coverage was 15% overvalued as of Sept. 24, up from fairly valued at the start of 2019. This is the most overvalued since late 2017 and mid-2016. We have no 5-star-rated U.S. utilities and only two utilities trade at a discount to fair value. All regulated utilities’ valuation multiples are historically rich: 25 P/E, 2.2 P/B, 2.8% dividend yield.

Drop in interest rates makes utilities’ dividends more attractive. - source: Morningstar

We think utilities investors should be cautious. High valuations erode some of the sector’s defensive benefits if the economy turns. Energy efficiency and customer rate cuts are fundamental headwinds. But for income investors trying to decide between bonds and stocks, high-quality U.S. utilities offer an attractive mix of premium yields and consistent growth.

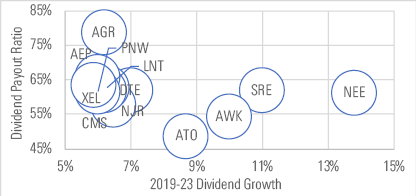

High-quality utilities have good growth, safe payout ratios. - source: Morningstar

Top Picks

Dominion Energy D Economic Moat: Wide Fair Value Estimate: $84 Fair Value Uncertainty: Low Dominion historically received premium valuations reflecting its high-return assets and constructive regulatory relationships. But the market remains fixated on the prospect of slowing dividend growth. Dominion's dividend increases have averaged 9% the past five years, but management has targeted 2.5% increases beginning in 2020 due to Dominion's elevated payout ratio. We believe the dividend is secure, due in part to the strong cash flow from Cove Point and earnings growth from its diverse regulated businesses. Investors willing to accept modest dividend growth in the short run should be rewarded with both a valuation uplift, attractive yield, and a return to long-term dividend growth that will outpace Dominion's peers.

Edison International EIX Economic Moat: Narrow Fair Value Estimate: $68 Fair Value Uncertainty: Medium The California utility has been wrapped up in market concerns about wildfires and bankrupt neighbor PG&E. But we think Edison's growth prospects and 4% yield outweigh any fire risk it faces. Edison is on track to invest $5 billion annually through 2023, most of which regulators have already approved. Its investments will go into infrastructure that supports energy security, safety, renewable energy, electric vehicles, and other next-generation energy services. This should drive at least 6% annual earnings and dividend growth. Resolution of political and legal issues involving PG&E during the next six to 12 months should remove the valuation overhang.

Duke Energy DUK Economic Moat: Narrow Fair Value Estimate: $88 Fair Value Uncertainty: Low Duke operates in mostly constructive regulatory regions, particularly in Florida, which allows it to recover costs in a timely fashion through supportive regulatory outcomes. We anticipate annual capital expenditures to average $8 billion over the next five years, supporting our 5% earnings growth forecast. The company's capital program focuses on grid modernization, renewable energy, natural gas infrastructure investments and environmental remediation. Key to our long-term growth expectations is successful completion of the Atlantic Coast Pipeline, which we continue to believe will be completed given the regional economic benefits.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WC6XJYN7KNGWJIOWVJWDVLDZPY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HHSXAQ5U2RBI5FNOQTRU44ENHM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/737HCNGRFLOAN3I7RKGB7VPEKQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ea0fcfae-4dcd-4aff-b606-7b0799c93519.jpg)