Energy: Oilfield Services Particularly Compelling

The sector overall is cheap, but oilfield-services stocks are at decade lows.

/s3.amazonaws.com/arc-authors/morningstar/6518ca15-698e-4020-8ab8-565600d029c7.jpg)

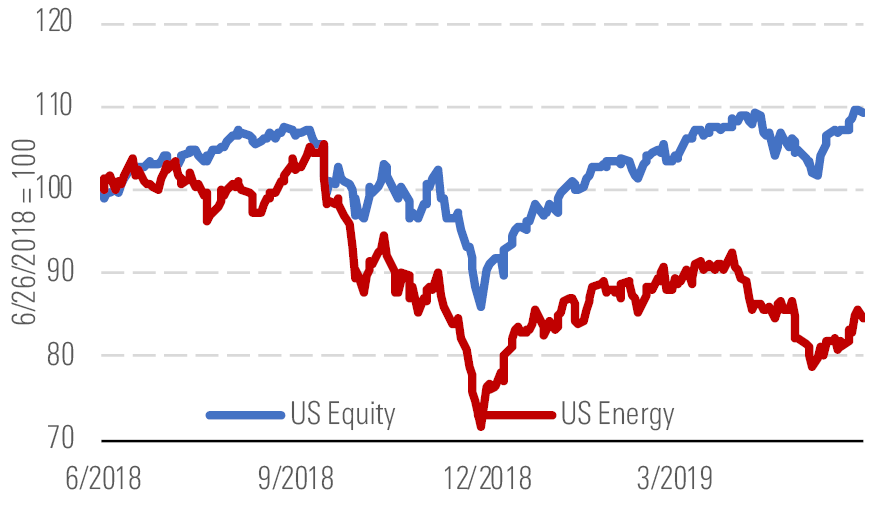

After rebounding in the first quarter, the Morningstar U.S. Energy Index sank in the second as oil prices ended the quarter roughly where they began. The Energy Index slipped 6% in the quarter to date through June 25 compared with a 3% gain for the Morningstar U.S. Equity Index (Exhibit 1).

Global energy index vs. global equity index - source: Morningstar Analysts

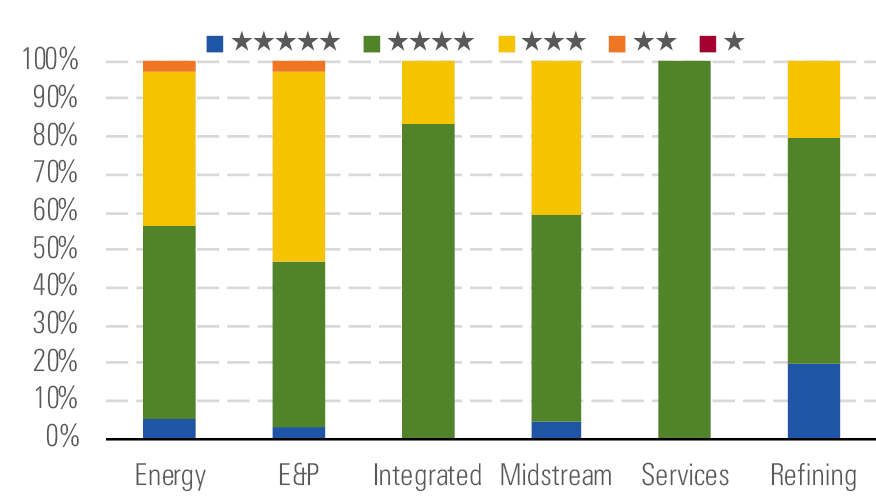

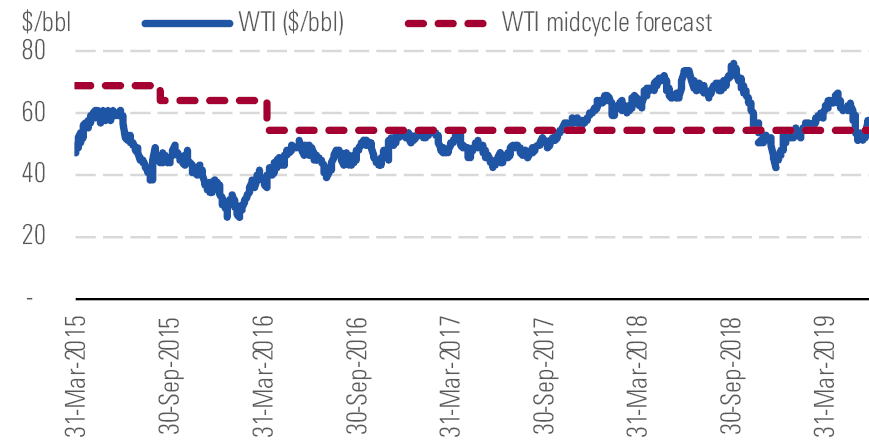

After briefly dipping below our unchanged midcycle price of $55 per barrel (Exhibit 3), oil prices recovered late in the second quarter to just below $60/bbl. But we still see value in oil-related stocks. As of June 25, the median price/fair value in our U.S. energy coverage was 0.83. The underperformance in energy has made it the cheapest sector in Morningstar's coverage, with a median price/fair value significantly below the 0.96 median for our entire coverage. We see particular opportunity in oilfield-services stocks, which haven’t looked this cheap in more than a decade.

Energy star rating distribution for sector and by key industry - source: Morningstar Analysts

Our long-term oil price forecast is above current prices - source: Morningstar Analysts

The decline in crude prices from the 2019 peak in mid-April has erased most of the energy stock gains from earlier in the year, when fundamentals were supported by strong compliance with steep OPEC cuts. Indeed, OECD oil inventories plunged in February and March. But debottlenecking in the United States has since enabled shale producers to resume their rapid growth, while trade fears increasingly threaten to stymie demand. Meanwhile, U.S. inventories have surged in the last three months. OPEC is likely to extend the cuts when they expire in June, with or without Russian support. However, this won’t be enough to sustainably drive up prices beyond our midcycle forecast, as shale producers can compensate by increasing activity during periodic upswings.

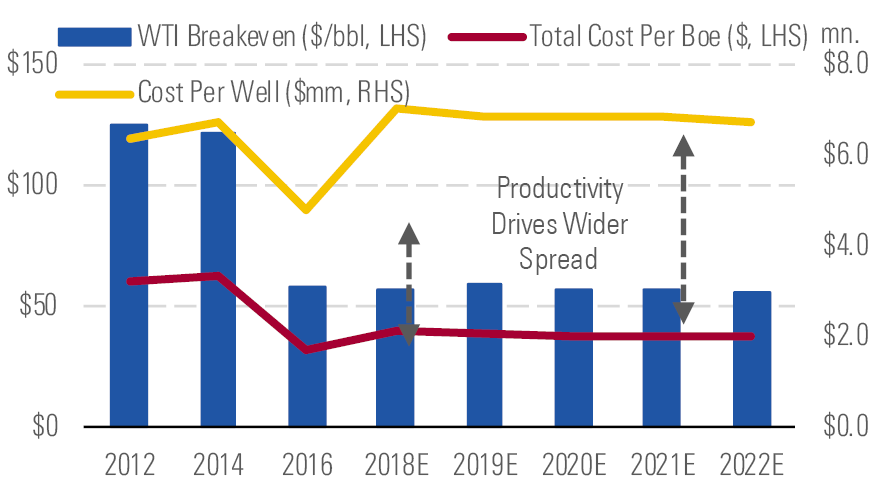

We see $55 as the fully loaded cost for the marginal barrel of oil that will balance global supply and demand in the long run, and we expect this barrel to come from a U.S. shale well. Shale wells today are much cheaper per barrel than the large, complex megaprojects that would have set prices in a world without U.S. shale. Over the long run, we think U.S. shale well cost inflation will remain subdued, owing greatly to the no-moat nature of many shale services, and that wider adoption of current technologies coupled with decades of attractive drilling opportunities will contain unit break-evens (Exhibit 4).

Oil break-evens to remain relatively flat - source: Morningstar Analysts

Top Picks Enbridge ENB

Star Rating: 4 Stars

Economic Moat: Wide

Fair Value Estimate: $46

Fair Value Uncertainty: Medium

Wide-moat Enbridge represents our Best Idea for investors in the Canadian midstream sector, and we see 30% upside in the stock. We believe the market doesn't realize the full potential of the company's growth portfolio, which is highlighted by the Line 3 replacement project (Canadian Mainline pipeline expansion). Even though Line 3 continues to face opposition and delays, we expect the pipeline to be built. Additionally, safeguards remain in place in the unlikely scenario that the project is canceled. Enbridge is able to recoup the capital spent on the project plus a healthy return on capital through toll surcharges. Accordingly, we expect Enbridge to generate significant free cash flow, allowing it to increase its dividend at approximately 10% in 2020 and 3% thereafter.

Enterprise Products Partners EPD

Star Rating: 4 Stars

Economic Moat: Wide

Fair Value Estimate: $35.50

Fair Value Uncertainty: Low

We don't think investors appreciate Enterprise’s leading position as the exporter of incremental hydrocarbon, whether liquefied petroleum gas, oil, or ethane. We expect NGL production and exports to sharply exceed consensus U.S. NGL production estimates, which imply that the U.S. cannot supply enough ethane to meet the $150 billion-plus steam cracker expansion underway, and U.S. NGL exports will actually decline.

Schlumberger SLB

Star Rating: 5 Stars

Economic Moat: Narrow

Fair Value Estimate: $62

Fair Value Uncertainty: High

Schlumberger remains our top oilfield-services pick. Schlumberger has the highest international share of revenue among peers, making it best positioned to take advantage of the coming capital expenditures rebound in international markets, which the market is neglecting. Also, we think the company is poised to gain market share and improve margins via its efficiency-boosting integrated project initiatives.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TP6GAISC4JE65KVOI3YEE34HGU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RFJBWBYYTARXBNOTU6VL4VSE4Q.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/YQGRDUDPP5HGHPGKP7VCZ7EQ4E.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/6518ca15-698e-4020-8ab8-565600d029c7.jpg)