Financial Services: Despite Recession Fears, We Find Value in Banks

The sector overall is slightly undervalued.

/s3.amazonaws.com/arc-authors/morningstar/75bbf764-3b6f-4f5a-8675-8f9488c74c04.jpg)

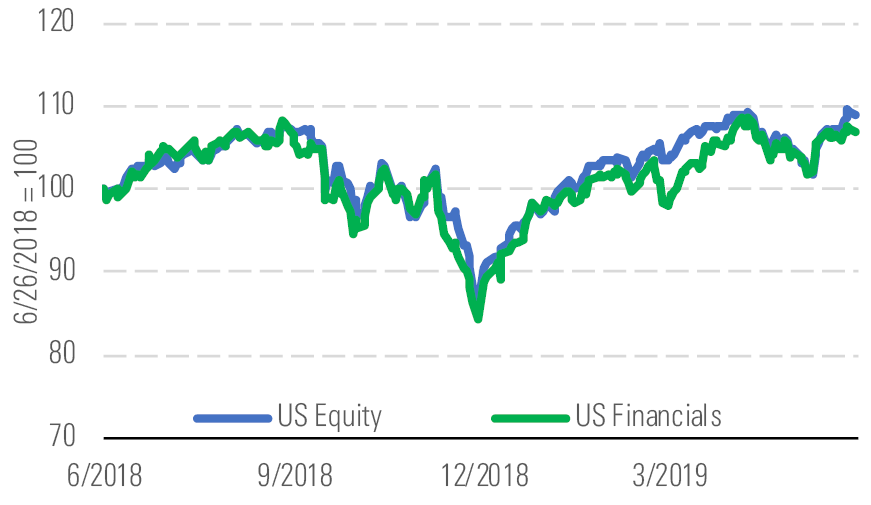

The Morningstar U.S. Financial Services Index outperformed the Morningstar U.S. Markets Index quarter to date through June 25, up 6% compared with 3% (Exhibit 1). Overall, the median U.S.-based financial-services stock trades at about a 6% discount to its fair value estimate, so we assess the sector as modestly undervalued.

Financials have recently clawed their way back up - source: Morningstar Analysts

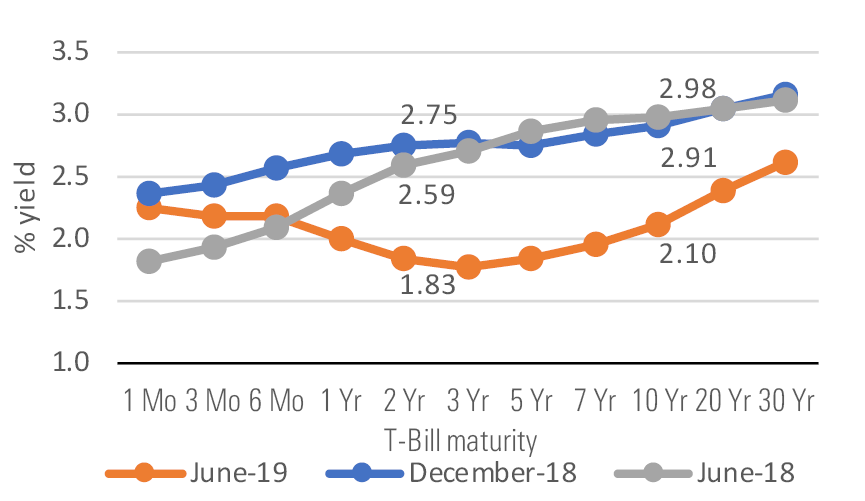

There's been a drastic change in the absolute level and shape of the U.S. yield curve over the previous year (Exhibit 3). Recently, U.S. Treasury securities until the 20-year Treasury bond all have yields below the target federal-funds rate. The 30-year Treasury bond is also yielding around 250 basis points. This compares to six months or a year ago when the yield curve sloped upward and the 30-year Treasury bond yielded over 300 basis points. Many are interpreting the inversion of parts of the yield curve as a sign that the Federal Reserve will cut interest rates soon and that a recession is on the horizon.

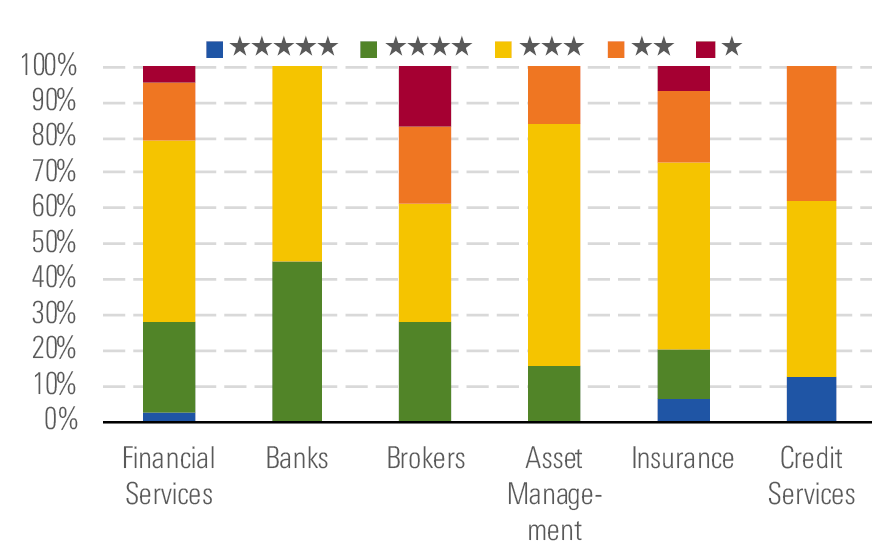

Banks and asset managers look modestly attractive - source: Morningstar Analysts

The shape of the yield curve has worsened for financials - source: Morningstar Analysts

This would negatively affect banks and companies that earn interest on securities portfolios. We think the market is overstating the long-term value implications and see the comparably more value in the banking industry than the rest of financial services, with over 40% rated 4 stars (Exhibit 2).

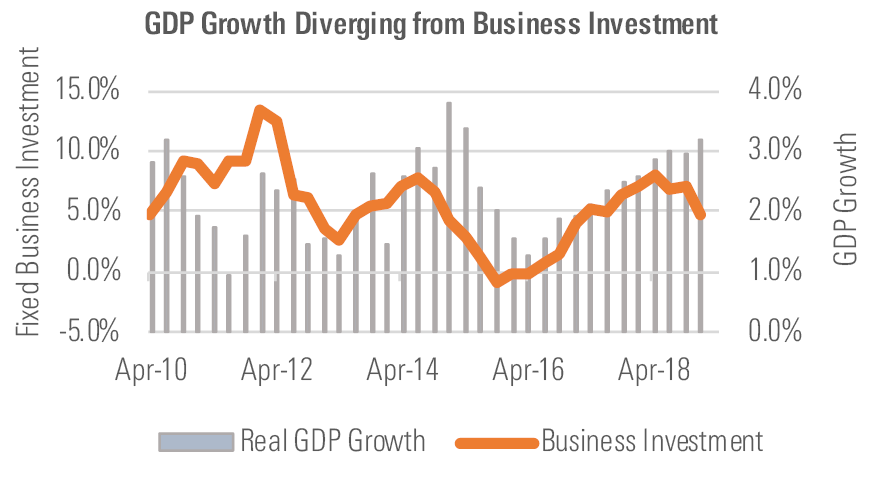

Many economic indicators are holding up fine (Exhibit 4), lending some credence to the ideas that a recession would have to be caused by some shock, such as a trade war, or a self-fulfilling prophecy of businesses pulling back on investing and consumers reining in spending in anticipation of a recession. Regardless of whether a recession occurs in the near future, interest rates and securities pricing in a recession could have real effects on the earnings of financial sector companies.

Most economic indicators are holding up fine - source: Morningstar Analysts, U.S. Treasury

Top Picks American International Group AIG

Star Rating: 5 Stars

Economic Moat: None

Fair Value Estimate: $76

Fair Value Uncertainty: Medium

We believe AIG CEO Brian Duperreault is a good fit for solving AIG's main operational issue: commercial property-casualty insurance underwriting. He was a primary architect behind peer Chubb's strong franchise that has generated industry-leading underwriting margins. He has pledged that AIG will generate an underwriting profit in 2019, and the company is on track to reach that goal. Given that we see no structural issues in its core operations, we believe AIG is gradually trending toward peer results. The current market price equates to about 0.8 times book value, a level that implies a long period of poor returns.

Berkshire Hathaway BRK.B

Star Rating: 4 Stars

Economic Moat: Wide

Fair Value Estimate: $243

Fair Value Uncertainty: Medium

We continue to be impressed by Berkshire Hathaway's ability to generate high-single- to double-digit growth in book value per share, and we like that the two front-runners for Warren Buffett’s CEO job—Ajit Jain and Greg Abel—have plenty of capital-allocation experience. Berkshire has plenty of cash on hand and a disciplined share-repurchase program. The shares are trading at a deep enough discount to our $364,500 ($243) per Class A (B) share fair value estimate, equivalent to 1.35 times our estimated end of 2020 book value per share, to warrant the attention of long-term investors.

Capital One Financial COF

Star Rating: 5 Stars

Economic Moat: Narrow

Fair Value Estimate: $133

Fair Value Uncertainty: Medium

Investors seem to be concentrating on the recent decline in interest rates and fears surrounding economic growth and applying it across all banks regardless of interest-rate sensitivity and growth prospects. Though economic growth would weigh on Capital One, investors should take comfort that its open-source software strategy should help the company win market share. Capital One’s victory in winning Walmart is important. To us, it signals that businesses are looking at a bank’s technological competency when deciding financial institutions with which to partner. We believe Capital One is years ahead of its competitors.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/2UWGQD7LCJCYNF3WQ5HHLP7UBE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WC6XJYN7KNGWJIOWVJWDVLDZPY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HHSXAQ5U2RBI5FNOQTRU44ENHM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/75bbf764-3b6f-4f5a-8675-8f9488c74c04.jpg)