Ratings Changes to Highlight for November

We delve into six of the 177 strategies that were rated last month.

/s3.amazonaws.com/arc-authors/morningstar/d40a2fd9-48c7-4b1b-9f14-4a62f5f471bf.jpg)

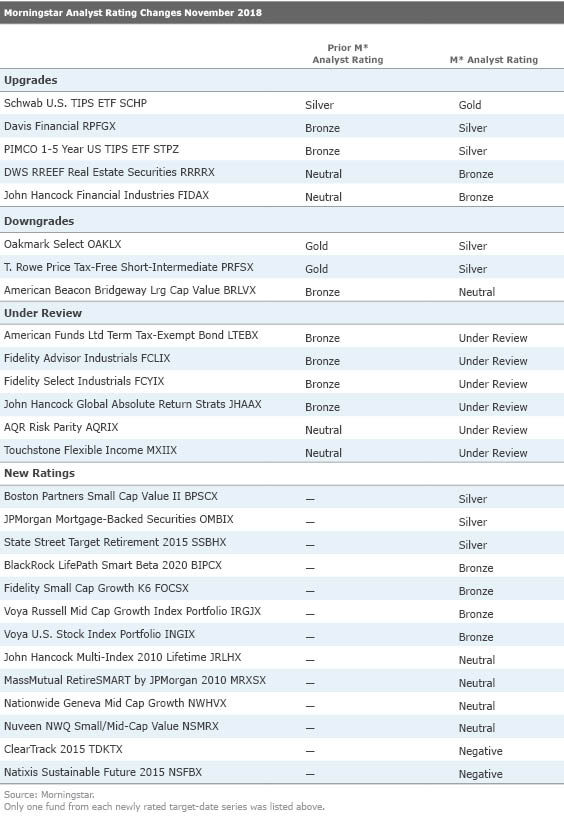

In November 2018, 177 strategies were rated, 13 of which were new to coverage. We affirmed the Morningstar Analyst Ratings of 150 strategies. Additionally, five ratings were upgraded, three were downgraded, and six funds were placed under review. A select group of ratings are showcased below, followed by the full list of ratings changes for the month.

Upgrades

The rating for

Downgrades

The rating for

New Ratings

For a list of the open-end funds we cover, click here. For a list of the exchange-traded funds we cover, click here. For information on the Morningstar Analyst Ratings, click here.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IGTBIPRO7NEEVJCDNBPNUYEKEY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/d40a2fd9-48c7-4b1b-9f14-4a62f5f471bf.jpg)