3 Bond Funds You May Be Tempted to Buy but Shouldn't

Outstanding returns can be a warning sign late in the credit cycle.

It's easy to identify funds with strong records. But as my colleague Russ Kinnel noted recently, it takes more than a strong record to earn a Morningstar Analyst Rating of Gold, Silver, or Bronze. Those medals reflect our expectation that a fund will be a standout performer in the future, and that requires a deeper investigation into a fund's fundamentals to determine whether it has a sustainable competitive advantage. If our analysts aren't convinced that a fund can continue to deliver strong results, they'll assign it a Morningstar Analyst Rating of Neutral or possibly Negative.

When a fund with a great record earns a Neutral rating, we get questions. In the world of bond funds, the reason our analysts take a skeptical view of past performance often comes down to risk. We ask ourselves the following questions:

- How much and what kinds of risk did a fund manager take to achieve those results?

- Does that manager have the resources to manage those risks effectively?

- Has the manager exercised sound judgment in adjusting the fund's risk profile in different environments?

- Is the fund's risk appetite excessive versus peers?

- What could go wrong?

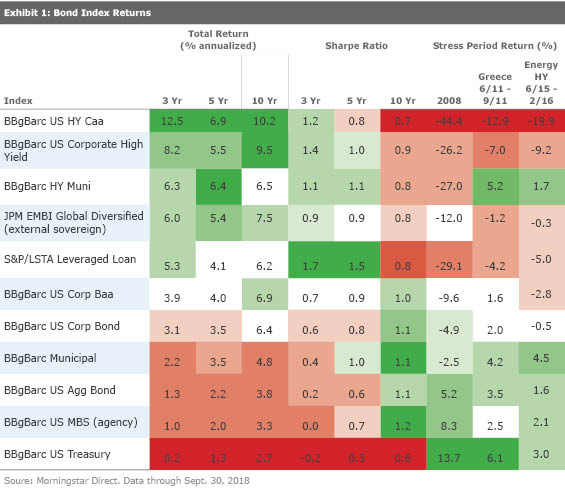

Risk is an especially critical factor to consider today, given that the last time the bond market experienced a broad sell-off across sectors was during the 2008 financial crisis. Now that we’ve passed the 10-year anniversary of Lehman Monday, financial crisis market stress is on the verge of rolling out of funds’ 10-year trailing records, an arbitrary but nonetheless standard period over which investors assess long-term performance. Meanwhile, several years of extraordinarily accommodative global monetary policy has suppressed yields on high-quality bond sectors and pushed investors into riskier sectors in exchange for incremental yield. As a result, the dominant trend over the past five years of gradual economic recovery and low default rates has been to reward risk-taking--the more the better.

The following table shows that the bond market’s riskiest sectors have also been its highest returning over the trailing three, five, and 10 years through Sept. 30, 2018. Adjusting those returns for volatility (Sharpe ratio) corrects for that somewhat, particularly over the past decade, which includes 2008’s painful final months. But as 2018 rolls out of the sample, the riskier sectors appear quite strong even on a volatility-adjusted basis.

Nevertheless, during periods of acute pain for credit markets, these same sectors have suffered significant downdrafts, as demonstrated in the table above. In addition to 2008’s financial crisis, I’ve shown bond sector returns during two subsequent credit sell-offs: contagion from the Greek government debt crisis in 2011 and the energy-sector-led high-yield sell-off from mid-2015 through early 2016. That’s worth remembering in this late stage of the current credit cycle.

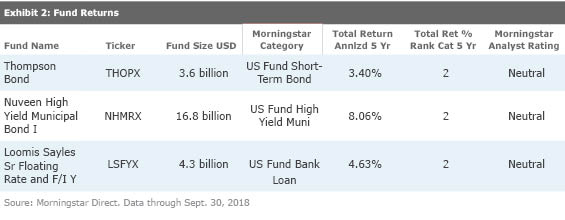

The funds discussed below are all examples of bond funds that have posted impressive returns over the past several years but earn a Neutral Analyst Rating. Here’s why.

Thompson Bond THOPX

Thompson Bond was a small fund until after the financial crisis, when it began to see large inflows. Investors were attracted by the fund’s plump yield, which came from its sizable stake in corporate bonds, especially its concentration in BBB rated corporates (typically above 70% of the portfolio). Amid a friendly climate for risk-taking, the fund grew from $45 million in assets at the end of 2008 to a peak of $3.7 billion in late 2014. Unfortunately, the fund’s appetite for risk stung when oil prices plummeted in late 2014 and 2015, causing the fund to shed 7.7% of its value during the sell-off from June 2015 through February 2016, the worst result of any in the short-term bond Morningstar Category. During that period, investors hit the road: The fund suffered 20 consecutive months of outflows totaling nearly $1.8 billion.

As the corporate bond market has bounced back since early 2016, so have this fund’s returns, and investors are once more piling in. The fund is sticking to its BBB corporate-heavy strategy, but with an investment team of five covering everything from corporate bonds to asset-backed securities to equities, we don’t think the fund has the resources to gain a research edge over the competition. Moreover, the fund remains vulnerable to suffering steep losses in another sell-off.

Nuveen High Yield Municipal Bond I NHMRX

Nuveen High Yield Municipal Bond has some compelling traits. It’s backed by one of the largest muni research teams in the industry, and we have enough confidence in the quality of the research and portfolio management at Nuveen to recommend some of this funds’ muni siblings, such as Bronze-rated

All of these techniques have turbocharged the fund’s returns and yield in favorable climates; its 5.4% 12-month yield as of September 2018 was the second-highest in its peer group, for instance. But they can also cause substantial pain during muni market sell-offs, as we’ve witnessed here in the past. The fund’s excruciating 40% loss in 2008 nearly doubled that of its typical peer, while its 10% decline following Meredith Whitney’s dire prognostications (October 2010 through January 2011) and 12% loss in the 2013 taper tantrum (May through August 2013), also ranked among the category’s worst. At $16.8 billion in assets, the fund is by far the category’s largest, and it took in nearly $8.0 billion of that total just since 2014. It remains to be seen how patient those investors are during future episodes of turbulence.

Loomis Sayles Senior Floating Rate and Fixed Income LSFYX

This bank-loan fund comes from good stock. Our confidence in Loomis Sayles’ corporate credit research acumen has supported Gold Analyst Ratings for a few of this fund’s siblings, including multisector bond fund

While the fund’s daring profile has been mostly successful so far, investors got a taste of the downside of this approach during the mid-2015 to early-2016 high-yield sell-off. The fund’s 6.9% loss during that stretch lagged more than 80% of its distinct peers. Absent a lengthier track record demonstrating otherwise, we’re concerned the fund’s struggles could compound during a more severe downturn.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OMVK3XQEVFDRHGPHSQPIBDENQE.jpg)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WJS7WXEWB5GVXMAD4CEAM5FE4A.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/NOBU6DPVYRBQPCDFK3WJ45RH3Q.png)