10 Cheap, High-Quality Stocks with Growing Yields

These 10 undervalued Morningstar US Dividend Growth Index constituents are cash-rich businesses with sustainable and growing payouts.

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

Companies' management teams tend to take their commitment to return cash to shareholders pretty seriously. Dividend cuts or eliminations are often severely punished by the market because they indicate financial distress (

To find companies with a history of dividend growth--and the ability to sustain it--the Morningstar US Dividend Growth Index uses several screens. First, we cull the U.S. equity market for securities that pay qualified dividends. (This excludes real estate investment trusts.) Index constituents must exhibit a five-year history of increasing their dividend payments. To gauge the sustainability of dividend growth, eligible constituents must display positive consensus earnings forecasts from the analyst community. As a safeguard against dividend cuts and financial distress, stocks with indicated dividend yield in the top 10% of the universe are excluded. Finally, existing constituents are allowed to remain if they have recently bought back shares and have not decreased their dividend payment.

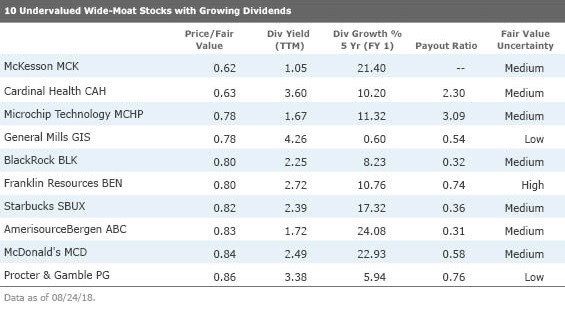

To find some investment opportunities among wide-moat companies that are well-positioned to increase their payout, we sorted the 450-plus constituents in the US Dividend Growth Index to find the 10 cheapest stocks relative to our analysts' estimate of their intrinsic value. Below, we dive into our analysts' takes on three of the undervalued names.

Director of technology sector equity research Brian Colello believes Microchip has a wide economic moat stemming from intangible assets around proprietary chip designs and manufacturing expertise. In addition, switching costs make it difficult to swap out Microchip's chips for competing offerings once they are designed into a given electronic device. Given Microchip's track record of stellar profitability in recent years and ability to retain its leadership position in microcontroller chips while expanding its analog business, Colello thinks it is more likely than not that Microchip will earn on excess capital over the next 20 years.

Colello believes Microchip's management team understands the importance of its dividend as part of an investment thesis, and he thinks Microchip has done a stellar job of distributing cash to shareholders. He points out that the firm has a very attractive dividend policy, paying out over half of its earnings and increasing the dividend a little bit on a quarterly basis.

Nonexistent switching costs, intense industry competition, and low barriers to entry make it difficult for restaurants and specialty retailers to establish long-lasting competitive advantages. Consumer equity strategist R.J. Hottovy believes Starbucks is an exception, however, owing to brand intangible assets that command premium pricing combined with meaningful scale advantages. He expects the company to maintain its specialty coffee leadership while successfully finding new growth avenues.

Hottovy also lauds the company's capital allocation approach. In general, Hottovy prefers consumer companies that show the willingness to invest in or acquire high-growth potential projects while still returning cash to shareholders through dividends and buybacks. Starbucks fits this bill, Hottovy says, with several investments and acquisitions in recent years like Princi, Teavana, Evolution Fresh, La Boulange, and the purchase of the remaining stakes of Starbucks Japan and Starbucks China that it didn't own.

Analyst Sonia Vora thinks General Mills enjoys a wide moat formed by intangible assets and cost advantages. She expect the firm's returns on invested capital to remain above its cost of capital (even in a pessimistic scenario) over the next 20 years. The firm's portfolio includes several recognizable brands, including Cheerios, Haagen-Dazs, and Yoplait, which have bolstered its relationships with retailers that depend on leading brands to drive store traffic and inventory turnover.

In general, Vora thinks General Mills' stewardship of shareholder capital has been decent, as evidenced by its returns on invested capital averaging 25% over the past decade, well in excess of our 7% cost of capital estimate. Vora expects General Mills will return substantial amounts of cash to shareholders via dividends and share repurchases. She estimates a dividend payout ratio averaging 65% (in line with the firm’s five-year historical average) over her forecast period.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ROHC7ZXJXZU7LIKGTTYJTD667I.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TP6GAISC4JE65KVOI3YEE34HGU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RFJBWBYYTARXBNOTU6VL4VSE4Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)