Risk Control

Fidelity Growth Strategies keeps the risks of mid-cap growth investing in check.

/s3.amazonaws.com/arc-authors/morningstar/6bbc8215-6473-41db-85a9-2342b3761e74.jpg)

An investment management internship in the summer of 2000—as the dot-com bubble was bursting—might have dissuaded some students from pursuing a career in the field. Jean Park was undaunted. After graduating from Harvard with a bachelor’s degree in economics, she followed a clearly marked path to portfolio management, starting with a job as a high-yield analyst at Goldman Sachs, then an MBA from Wharton.

“I’m one of those lucky people who figure out at their first real job what they find interesting,” Park says. That conviction ultimately led her to a position at Fidelity as a financial-services analyst in 2006—just in time for the financial crisis.

Again, the timing may have seemed inauspicious, but it helped shape the investment philosophy Park follows today: “My early experiences instilled my focus on protecting the downside.”

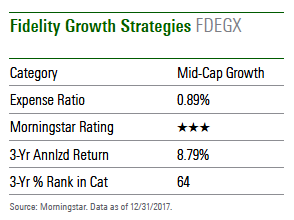

That philosophy is manifest in Fidelity Growth Strategies FDEGX, which Park has run since mid-2013. She aims to take less risk than the fund’s benchmark, the Russell Midcap Growth Index, while earning competitive returns over the long run. Under her direction, the fund has earned a place on the Morningstar Prospects list, a list of up-and-coming or under-the-radar investment strategies that Morningstar Manager Research analysts believe may prove worthy of full coverage in the future.

Where the Fish Are The strategy starts by screening a universe of about 1,000 mid-cap stocks for those with above-average free-cash-flow yields. Citing data that indicates that companies in the Russell benchmark with the highest free-cash-flow yields have outperformed from 1990 to 2016, Park says that it makes sense to "fish where the fish are." The screens also select for what she calls "alpha factors" that will improve the odds of outperformance: consistent and above-average returns on capital, favorable capital allocation, and valuations below or in line with historical averages. As that last factor underscores, this is not an aggressive growth play.

The screens are the starting point. From there, Park seeks out companies with unique competitive advantages, in industries with favorable structures, and where management incentives are aligned with shareholder interests. Here’s where she leverages the work of the analyst team she grew up in, first covering financial services and then consumer discretionary names, before being tapped to run a sector fund, Fidelity Select Leisure Portfolio FDLSX, in 2010.

“The research department at Fidelity is a big part of the process,” Park says. “We have comprehensive coverage, an army of analysts who are industry experts.”

Katie Rushkewicz Reichart, a director with Morningstar Research Services, agrees that Fidelity’s fundamental research provides an advantage. The group overall did see a fair amount of turnover in 2016–17 on the consumer, energy/utilities, and cyclical teams. Reichart notes, however, that “Fidelity’s equity analyst team is particularly strong in technology and healthcare, which this fund benefits from given its growth mandate.”

Improving the Odds That research team is largely aligned by industry group, and the analyst expertise is picking stocks, not sectors. Accordingly, this fund does not deviate dramatically from its benchmark's sector weights, though it can make active bets of plus or minus 500 basis points. To figure out where to tilt, Park monitors the benchmark by valuation.

The fund shifted from being underweight to overweight in technology in 2014 because the sector screened as the cheapest on a free-cash-flow basis. As of Oct. 31, the fund’s technology stake was about 3 percentage points higher than the Russell Midcap Growth’s 23.6% stake. Tech still screens well, Park says, as do financials and healthcare.

But again, the fund is tilted in these directions, not top-heavy. Likewise, Park does not make big bets on individual stocks. Roughly 200 stocks qualify for the portfolio based on the initial free-cash-flow-yield screen. From these, she aims to hold 100 to 150 names. At the end of October, the fund held 102 positions, all under 3% of assets.

“I’m playing to statistics, rather than to any one or two stocks,” Park says. “I’m trying to exploit natural tailwinds in the way I do portfolio construction. I like to have a lot of bets because I’m leaning on cheaper and high quality [to drive performance] over time.” Indeed, the fund has lower price multiples than its benchmark, combined with higher returns on equity and returns on invested capital.

In keeping with the approach to sector and stock stakes, the fund’s cash stake is generally around 1%. Rather than attempt to market-time, Park focuses on relative opportunities. Her early experience as a high-yield analyst informs her perspective: “Where liquidity was in the market, bond prices would move hugely, from 100 cents to 60 cents, then back to par two weeks later. When you see that early on in your career, you learn the market can be fickle.”

Weighing Options By both Fidelity's and Morningstar's performance attribution analysis, technology has been the biggest positive contributor to the fund's performance over the past three years, and video game publisher Electronic Arts EA has been a key pick over that time.

“It showed up on the radar in 2014, with one of the highest free-cash-flow yields. It screened beautifully,” Park says. New management focused on pruning the lineup of games, and the company’s formerly erratic return metrics improved. Since it was added to the portfolio, the stock has risen from the $40 range to more than $100 per share.

“The trouble with finding great stocks is that they grow their way out of the portfolio, and I am very focused on staying in mid-cap growth territory,” Park says. Electronic Arts outgrew the Russell Midcap Growth Index in June, and Park had trimmed the position below 1% as of October. Similarly, value-priced Avago was added in 2013 but has been cut after combining with Broadcom to become a semiconductor powerhouse; Broadcom AVGO has surged.

Park is not doctrinaire about market cap, however. She recently added a small position in largecap Applied Materials AMAT. She’d been watching the stock while monitoring her positions in KLA-Tencor KLAC and Lam Research LRCX and is enthusiastic about semiconductor capital equipment companies.

Applied Materials is not so far out of mid-cap range that Park was willing to forgo the additional opportunity. “We use quantitative risk metrics to monitor the portfolio, and by avoiding the riskiest assets, those with low to negative free cash flow, we have a beta below 1. Our semiconductor-equipment exposure bucked the beta.”

Overall, the fund had about 35% of assets in stocks that fall within Morningstar’s large-cap range, compared with 26% for its benchmark. However, its $15 billion average weighted market-cap is comfortably in mid-cap territory. (Small caps are only 3% of the portfolio, in line with the benchmark.)

Puzzling It Out While the fund has consistently fallen in the mid-cap growth section of the Morningstar Style Box over Park's tenure, the portfolio overall leans closer to the blend or core section of the box than its benchmark and typical category peer. That's a reflection of Park's attention to value, which sometimes demands a creative approach to tapping into growth trends.

“I think of it like a puzzle,” Park says. If an industry trend is promising but that fact is already reflected in stock prices, then she looks elsewhere in the market for related trends. Her 2017 entry into Carter’s CRI is an example. “I’d been spending a lot of time thinking about demographic shifts. Millennials are buying homes, but the valuations of homebuilders were anticipating a lot. Who else would benefit?” That line of thought led her to the children’s apparel maker.

Park sells when a stock’s valuation fully reflects its growth prospects, or when there are better relative opportunities. Other sales are driven by changing corporate strategies, and sometimes a realization that the original investment thesis was incorrect.

“O’Reilly Automotive ORLY is a pain point for me,” Park says. “It had high free cash flow, high ROEs, growing comps. I was suspicious of what was happening in the consumer discretionary sector, but O’Reilly seemed safe from Amazon.com AMZN. After Amazon bought Whole Foods, however, it was like a switch flipped.”

O’Reilly was a significant detractor from performance, but Park took the opportunity to harvest a tax loss. “To keep me honest, I periodically look at stocks where I’ve lost money,” laughs Park. “O’Reilly was on that list, and it prompted me to revisit the thesis.”

An Even Keel That misstep aside, the fund's performance overall under Park is promising, says Morningstar's Reichart. Its record was so-so under previous managers, while its 12.4% annualized return during her tenure (from mid-August 2013 through December 2017) is well ahead of the 10.9% mid-cap growth average. The fund did not best the tough-to-beat Russell Midcap Growth over that time; it trailed by an annualized 43 basis points.

Park’s emphasis on risk is evident in the results. The fund’s three-and five-year Morningstar Risk scores, which encompass her nearly four-year tenure on the fund, rate Low within the mid-cap growth category. That’s a significant drop from the fund’s 10-year score of Average, which incorporates outsized losses in 2008 and 2011. In contrast, under Park, the fund was in the black in 2015, and in the top quintile of the category, when its average peer was in the red.

Risk control is where the fund stands out relative to its benchmark, as well. From September 2013 through December 2017, it earned 93% of the Russell Midcap Growth Index’s upside, but only 87% of its downside. (The fund’s downside protection was even greater relative to peers; it suffered only 75% of the mid-cap growth average downside.) While that left the fund a bit behind its benchmark on an absolute basis, it came out ahead on risk-adjusted measures such as the Sharpe and Sortino ratios.

The fund is likely to lag in rallies, and indeed, it ranked in the bottom half of its category for 2017, although its 21.5% return was decent. (Funds in the top quartile of the category last year were up more than 30%.) But, as Park says, “the fund shines most in a downturn. My job is to make sure the fund is aligned with its strategy, and to leverage our strengths.”

Easy to Use Given Park's attention to valuation and risk, the fund might serve as a core mid-cap holding for investors with a growth orientation. It also slots neatly into the mid-cap growth space of a broader portfolio, given its close alignment with the Russell Midcap Growth Index. (The fund's tracking error is around 3%.) Its limited cash stake makes it easy to factor into asset-allocation decisions.

Because Park is also mindful of tax implications when timing trades, the fund is suitable for taxable accounts. Its 15.1% annualized five-year return through December drops only a bit, to 15.0%, after taxes on distributions. While some of the fund’s shareholders invest via tax-advantaged accounts, Park notes that a tax-aware approach aligns with Fidelity’s long-term approach to equity analysis, which involves forecasting 12 to 24 months out. “Research shows that high turnover is not where the alpha is,” Park says.

The fund has other advantages that improve its chances of maintaining a competitive edge. For one, with “a good chunk” of her own assets in the fund—in the $500,000 to $1 million range, per the most recent SEC filing— Park’s interests are aligned with shareholders. That bodes well because Morningstar has found that manager investment correlates with fund success rates. Funds with high manager investment are more likely to both survive and outperform peers.

Second, although Park recently took over the large-cap Fidelity Fund FFIDX (employing a similar approach, benchmarked to the S&P 500), her assets under management in this strategy are not approaching capacity. At under $3 billion, this fund remains nimble for a mid-cap fund. Factor in a below-average expense ratio relative to other mid-cap no-load funds, and the fund is set up well for success.

In every issue of Morningstar magazine, Undiscovered Manager profiles a noteworthy strategy that hasn’t yet been rated by Morningstar Research Services’ manager research group.

This article originally appeared in the February/March 2018 issue of Morningstar magazine. To learn more about Morningstar magazine, please visit our corporate website.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LUIUEVKYO2PKAIBSSAUSBVZXHI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HCVXKY35QNVZ4AHAWI2N4JWONA.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/6bbc8215-6473-41db-85a9-2342b3761e74.jpg)