6 New Stocks in the Wide Moat Focus Index

The Morningstar Wide Moat Focus Index adds some healthcare and tech, eschews some financial services stocks.

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

In December, the Morningstar Wide Moat Focus Index swapped out six stock positions.

To be included in the Wide Moat Focus strategy, a company must have an economic moat rating of wide (which means we think they have advantages that will fend off competitors for at least 20 years), and its shares must be among those trading at the steepest discount to their fair value estimates. (Our fair value estimates are determined through independent research by the Morningstar Equity Research team.) Only U.S. stocks are included in the index.

The index consists of two subportfolios with 40 stocks each. The subportfolios are reconstituted semiannually in alternating quarters, and stocks are equally weighted within each subportfolio. After the December reconstitution, half of the portfolio swapped out six positions. The net result is that the index now holds 46 positions.

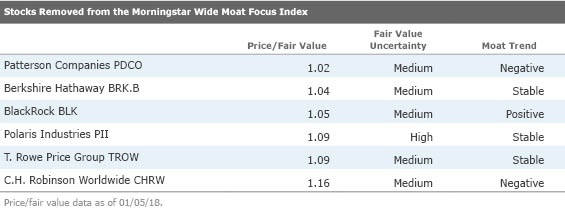

On the flip side, five stocks were removed because their price/fair values rose beyond our buy range. Notably, two asset managers,

In addition,

We removed

"We believe Patterson faces significant pressure from alternative sourcing options for dental consumable products (fillings, gauze, latex gloves, disinfectants, swabs)," said senior equity analyst Vishnu Lekraj. "From what we can gather, there has been increased competition from online-based wholesale players that can source consumables from the cheapest suppliers nationwide."

The table below lists the 10 cheapest stocks in the index, ranked by price/fair value. The median stock in the Wide Moat Focus Index is trading at a weighted average price fair/value of 0.90. By comparison, the broad Morningstar US Market Index is overvalued, trading at a weighted average price/fair value of 1.11 (with 85.7% of the index under analyst coverage).

Digging Into 2017 Performance

During 2017, the Wide Moat Focus Index returned 23.8%, beating its benchmark, the Morningstar US Market Index, by 232 basis points. It also outpaced the S&P 500 by nearly 200 basis points. Consumer cyclical stocks were the main performance driver during the quarter, comprising more than a fifth of the portfolio and rising 38%.

Financial services and healthcare were big contributors to performance, with

The Wide Moat Focus' zero weighting in energy continued to pay off, helping it outperform broader market indexes. Energy was the only stock sector in the red in 2017, ending the year with a 1.6% loss. Despite the slide, we have not identified any competitively advantaged companies selling at a discount in the energy space for quite a while. The median energy stock under our coverage is overvalued, trading a price/fair value of 1.1%.

Basic materials hurt performance worse than any other sector so far this year. Among individual stocks, rock-salt producer

And although the healthcare weighting has been a positive contributor in aggregate this year, not all bets in the sector paid off.

Click

to see the top 25 positions in the index. (Premium members can see

.)

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PLMEDIM3Z5AF7FI5MVLOQXYPMM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/I53I52PGOBAHLOFRMZXFRK5HDA.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CEWZOFDBCVCIPJZDCUJLTQLFXA.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)