Active Managers' Short-Term Success Rates Have Spiked Higher

Despite short-term trends, picking good active managers is hard and keeping costs low is paramount.

/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)

In 2015 I, along with some of my colleagues, began working on a project to more systematically measure active managers' success rates in a given Morningstar Category. Specifically, we were looking to answer this question: If an investor were to select an actively managed fund at random from a particular category, what are the odds that fund will survive and outperform its passive peers in any given time period? The product of our efforts is the Morningstar Active/Passive Barometer.

The Active/Passive Barometer is a semiannual report that measures the performance of U.S. active managers against their passive peers within their respective categories. The Active/Passive Barometer report is unique in the way it measures active managers’ success relative to the actual, net-of-fee performance of passive funds rather than an index, which isn’t investable.

We measure active managers’ success relative to investable passive alternatives in the same category. For example, an active manager in the U.S. large-blend category is measured against a composite of the performance of its index mutual fund and exchange-traded fund peers

We believe this is a better benchmark because it reflects the performance of actual investable options and not an index. Indexes are not directly investable. Their performance does not account for the real costs associated with replicating their performance and packaging and distributing them in an investable format. Also, the success rate for active managers can vary depending on one’s choice of benchmark. For example, the rate of success among U.S. large-blend managers may vary depending on whether one uses the S&P 500 or the Russell 1000 Index as the basis for comparison. By using a composite of investable alternatives within funds’ relevant categories as our benchmark, we account for the frictions involved in index investing (such as fees) and mitigate the effects that might stem from cherry-picking a single index as a benchmark. The net result is a far more fair comparison of how investors in actively managed funds have fared relative to those who opted for a passive approach.

We measure each fund’s performance based on the asset-weighted average performance of all of its share classes in calculating success rates. This approach reflects the experience of the average dollar invested in each fund. We then rank these composite fund returns from highest to lowest and count the number of funds with returns exceeding the equal-weighted average of the passive funds in the category. The success rates are defined as the ratio of these figures to the number of funds that existed at the beginning of the period. Given this unique approach, our field of study is narrower than others, as the universe of categories that contained a sufficient set of investable index-tracking funds was fairly narrow going back 10, 15, and 20 years ago. We expect that the number of categories we include in this study will expand over time.

We also cut categories along the lines of cost. Cost matters. Fees are the one of the best predictors of future fund performance. We have sliced our universe into fee quartiles to highlight this relationship.

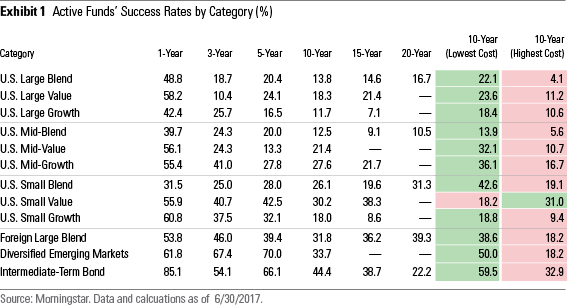

The Results Are In As is apparent in Exhibit 1, actively managed funds have generally underperformed their passive counterparts, especially over longer time horizons. In addition, we found that failure tended to be positively correlated with fees—that is, higher-cost funds were more likely to underperform or be shuttered or merged away, and lower-cost funds were likelier to survive and enjoyed greater odds of success. Again, fees matter. They are one of the only reliable predictors of success.

This latest installment of our report is the first to include success rates and performance figures for the 15- and 20-year review periods for those categories for which we have sufficient data. This includes 10 of the 12 categories we’ve examined for the 15-year period ended June 30, 2017, and five of the 12 for the trailing 20-year period. These longer-term numbers aren’t—in most cases—materially different from the 10-year numbers. The noteworthy exception is the intermediate-term bond category. The 15- and 20-year success rates in this segment are materially lower than what we’ve measured in more recent periods, which have been marked by active managers’ being richly rewarded for taking more credit risk and, of late, less interest-rate risk than their index-tracking peers.

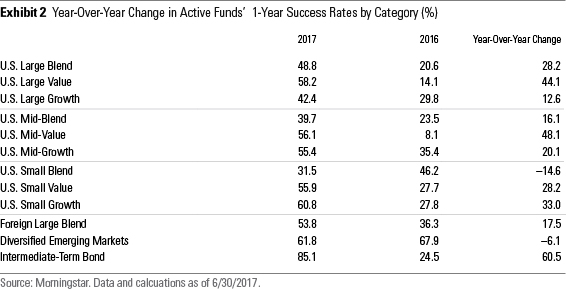

Don't Call it a Comeback As can be seen below in Exhibit 2, active managers' short-term success rates spiked higher over the 12 months through June 2017. The increases were especially pronounced among value-leaning stock-pickers. This recent uptick can be attributed to a variety of factors, most having to do with managers getting a lift from investments that aren't necessarily true to their style. Over the year ending June 2017, stocks in foreign developed markets outperformed U.S. stocks, growth beat value, and small caps edged out large caps. These are all generally favorable conditions for active managers that aren't shy about coloring outside the lines that define their position in the Morningstar Style Box. While many have heralded this as the beginning of a potential comeback for active managers, the reality of the matter is that it is business as usual. Active managers' short-term success rates have been and will continue to be noisy. The long-term signal remains clear: Picking good active managers is hard and keeping costs low is paramount.

A Beginning, Not a Middle, and Certainly Not an End I think the Active/Passive Barometer is a useful starting point for investors looking to assess their odds of finding a winner when it comes to picking successful active managers. It is little surprise that focusing on fees is the best way to boost your chances of partnering with a manager that will best their passive peers.

Those who are interested can find the mid-year 2017 edition of Morningstar's Active/Passive Barometer here.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/d10o6nnig0wrdw.cloudfront.net/04-18-2024/t_34ccafe52c7c46979f1073e515ef92d4_name_file_960x540_1600_v4_.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-09-2024/t_e87d9a06e6904d6f97765a0784117913_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)