Have U.S. Stocks Become Too Expensive?

Addressing the question from a global perspective.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Market-Timing? I had intended to rebut Ben Johnson's "Home Bias Blues" article, in which he argues that U.S. investors should hold more foreign securities. There are valid reasons for dining in, which I planned to raise. However, Ben acknowledges those arguments and counters them effectively. So … I agree with his column. This article will be no Point/Counterpoint.

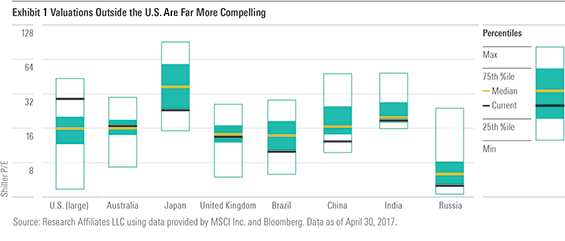

However, I do wish to examine one of Ben's side points, which is that now is a particularly good time to look elsewhere, because U.S. stocks have become unusually costly relative to their peers. Ben brandishes a chart, courtesy of Research Affiliates, showing that that U.S. stocks are now relatively expensive, while other countries' stocks look to be cheap. The obvious conclusion is to favor the latter over the former.

Yes and no. The "Yes" argument is straightforward: Research Affiliates is a reputable firm, and that chart's data makes a compelling claim.

Another Angle

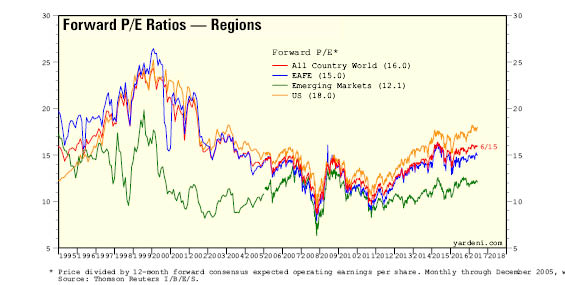

For the "No" argument, let's observe a different view of global price/earnings ratios

provided by Yardeni Research. This graph takes a regional rather than country perspective, sorting the world into three categories: non-U.S. developed markets (MSCI EAFE Index, in blue), emerging markets (green), and the United States (yellow). The red line then combines the other three lines to illustrate the MSCI All Country World Index.

- Source: Yardeni Research

That red line looks odd. In theory, it blends the yellow, blue, and green lines, yet only the first two seem to matter. No matter where the green line is drawn, the red line lands midway between the yellow and blue. This occurs because, despite their huge populations and land masses, the emerging countries remain a small slice of the global stock market. The money--and corporate profitability--is not yet where the people are.

The green line of emerging markets currently falls well below U.S. levels, but that's nothing new. The emerging markets were even further behind in 2001. Which provides a useful test. If Ben's thesis is correct--that countries with lower-cost stocks offer higher future returns--then the emerging markets should have outstripped the U.S. since 2001.

Score one for Mr. Johnson. The emerging markets have gained 9% annually since 2001, as opposed to just under 6% for the S&P 500. On that occasion, at least, the cost signal worked.

Whether it will do so for emerging markets in the future is unclear. At the start of 2009, U.S. stocks carried a forward P/E ratio (based on expected operating earnings) of 24, with the emerging markets at 9. Quite the gap. These days the divergence is much smaller, at 18 versus 12. That difference is roughly the average between the two regions during the past 20-plus years, so it may not narrow. On this measure, at least, I would hesitate to call U.S. stocks relatively expensive.

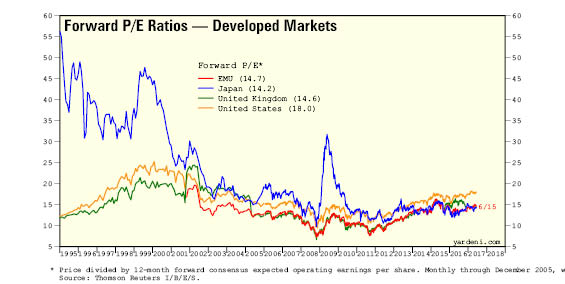

The evidence from EAFE is stronger. After hugging American valuations for 15 years, EAFE's P/E ratio has gradually lost relative ground during the past several years. At 15 compared with the U.S.' 18, the P/E ratio for non-U.S. developed markets trails by the largest margin since at least the mid-1990s--and its absolute level isn't terribly high, either. This chart supports Ben's claim.

But Then Again … The next chart does not. There is EAFE, and then there is EAFE. By which I mean the major non-U.S. markets consist of two distinct regions: Western Europe and Japan. Those entities have behaved very differently indeed. Japanese stocks had far higher P/E ratios than did U.S. equities throughout the 1990s, and even sometimes in the years following. They have since dropped below U.S. levels.

Stocks in continental Europe and the United Kingdom have steadily churned along, selling at P/E ratios about 25% below those of the U.S. This held true in the early 2000s, the late 2000s, and today.

- Source: Yardeni Research

Thus, upon further examination, that blue EAFE line misled. Rather than show one region that had been priced for years similarly to U.S. stocks but that has recently been left behind by American increases, the EAFE line subsumed two regions--one of which had been far more expensive than the U.S, but no longer is, and one that reliably and consistently has sold at a moderate discount to the U.S. If there is any cost argument to make, it is that Japan is now desirably cheap--not that the U.S. is relatively expensive.

Forward P/E ratios on operating earnings are but one way of gauging stock valuations (albeit a sound one). Other measures will yield other results. Nonetheless, Yardeni's figures suggest that, if U.S. stocks are indeed too expensive when compared with the global alternatives, this is something we will learn only in hindsight; based on current information, reasonable minds can differ.

I heartily endorse Ben's recommendation that U.S. investors increase their international-stock exposure--admittedly, it's advice that I have yet to follow--but I do not believe that now is a particularly good time to do so. All times are appropriate for diversifying overseas, this one being no more or less than others.

(True, the U.S. dollar has recently been strong, which would suggest that perhaps foreign stocks will benefit from rising currencies. However, as the U.S. dollar index is currently near its 40-year mean, there's no particular reason to regard the dollar as being too rich rather than too poor.)

Conflicting Indicators The elevator info-screen flashed, "The dumbest guy in high school just got a boat," thanks to his E*TRADE account. That reminded me of a similar advertisement that accompanied a stock-market peak: Discover Brokerage's tow-truck driver--who just happened to also own a desert island, courtesy of his day-trading skills.

Yes, that worried me. But I was comforted when I picked up The Wall Street Journal this morning. Thirty-two pages in total, from cover to cover. That's no sign of a market top.

So, as with global stock P/E ratios, consider the anecdotal evidence on U.S. stock prices to be a mixed bag.

John Rekenthaler has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ROHC7ZXJXZU7LIKGTTYJTD667I.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TP6GAISC4JE65KVOI3YEE34HGU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RFJBWBYYTARXBNOTU6VL4VSE4Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)