6 Traits of the Best Indexes

Finding an index that scores well across these six dimensions can help investors choose among seemingly similar funds.

/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)

This article is part of Morningstar's Guide to Passive Investing special report.

A version of this article was published in the November 2016 issue of Morningstar ETFInvestor. Download a complimentary copy of ETFInvestor here.

It may be tempting to skimp on due diligence for index funds and exchange-traded funds. After all, they typically employ transparent, rules-based strategies that are not susceptible to key-manager risk. But seemingly similar index funds can look and perform differently, so portfolio construction still matters. To evaluate these funds' processes, we set out to answer two questions: 1) How is the index constructed? and 2) How is the portfolio managed to deliver high-fidelity tracking performance of its index? The former determines the composition of the portfolio and how the fund will behave. The latter focuses on both the fund's replication strategy and structure. While it is important, it doesn't move the needle as much as index construction, which is the focus of this article.

Index Construction Framework The best index funds have portfolios that are representative of their actively managed peers--or in the case of strategic-beta funds, the style they are trying to capture. They are well-diversified, investable, transparent, sensible, and take steps to mitigate unnecessary turnover. Funds don't have to score well on all these dimensions to receive a Positive Process Pillar rating, but this framework can help us differentiate between seemingly similar strategies and better evaluate their merit.

The more representative an index fund is of its actively managed peers, the more reliably its cost advantage should translate into better performance. If there are material differences--with respect to the sector, style, security, or country weightings--between the index fund and its active peers, its gross performance can differ meaningfully from the category average. And its cost advantage may not be sufficient to overcome underperformance when it does occur.

For example,

Diversification is perhaps an even more important consideration than representativeness because it can help mitigate exposure to risk that the market does not reward. Investors can gauge concentration risk with simple metrics like the percentage of a fund's assets in its top 10 holdings. As a rule of thumb, if this figure is above 30%, firm-specific risk may be creeping into the portfolio. Diversification across sectors and countries (in the case of international strategies) is also important.

Even a well-diversified index may not be worth touching if it is difficult to track or has limited capacity, meaning that it is not investable. Fortunately, investability isn't a problem for most equity index funds. However, it can be an issue for funds that invest in less liquid securities, like micro-cap stocks and thinly traded bonds. These securities are often difficult to access and expensive to trade. Consequently, index funds that cover them tend to have higher tracking error and transaction costs than those that invest in more-liquid securities.

Transparency makes it easier to anticipate changes to the portfolio, which is important because index strategies run on autopilot. It can also make it easier to understand how the index will likely perform. Indexes managed by committee, like the S&P 500 and Dow Jones Industrial Average, do not meet the transparency standard. Neither do index funds that employ complex optimization models to construct their portfolios, like iShares Edge MSCI Multifactor USA LRGF. These strategies could still be worth investing in, but it is prudent to wait until they have established a record to get a better handle on how the process works in practice.

It goes without saying that a strategy should be sensible, but it's not always obvious which strategies clear that hurdle. Price weighting, the approach that the Dow Jones Industrial Average employs, is a prime example of a process that falls short. There is no viable economic theory to support price weighting, which assigns larger weightings to higher priced stocks. Dow Jones simply adopted it because limited computing power rendered alternative approaches impractical when it first calculated the index in the late 1800s. While there are other such indexes that fail this basic sensibility test, there aren't many of them and most do not attract much money.

Finally, good indexes take steps to mitigate unnecessary turnover. This is important because there are costs associated with turnover, particularly among less liquid securities. For example, the Dow Jones U.S. Small-Cap Total Stock Market Index, which Silver-rated

In contrast, the Russell 2000 Index, which underlies Bronze-rated

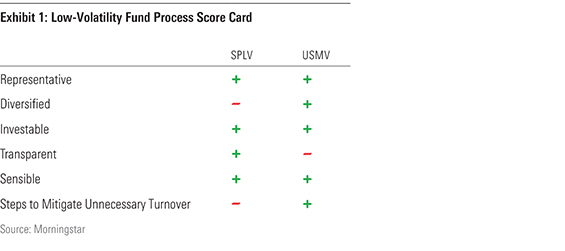

Case Study 1: SPLV vs. USMV

To illustrate how we apply this framework in practice, let's use it to compare Bronze-rated

USMV takes a more holistic approach to reduce volatility. It employs a complex optimizer to construct the least volatile portfolio possible with stocks from the MSCI USA Index under a set of constraints. These include limiting turnover and sector tilts relative to its parent benchmark to improve diversification. This strategy doesn't just target the least-volatile stocks. It also considers each stock's exposure to common risk factors and how they interact with each other to affect the portfolio's overall volatility.

While SPLV offers purer exposure to low-volatility stocks than USMV because it does not constrain the portfolio, both funds effectively reduce volatility and are representative of the defensive equity style. Both strategies are also sensible--backed by independent research--and investable, focusing on highly liquid large- and mid-cap stocks. But that's where the similarities end.

USMV earns high marks for diversification and steps to mitigate unnecessary turnover, where SPLV does not. That's because only the iShares fund limits its sector tilts and turnover. Consequently, SPLV has exhibited significantly higher turnover than USMV in three of the past four years. And, at times, it can make large sector bets. For instance, utilities stocks currently represent about 23% of the portfolio (though they only account for 3% of the S&P 500). But the PowerShares fund outshines its rival for transparency. There are a lot of moving parts in USMV's optimizer, so it is difficult to anticipate changes to the portfolio ahead of time. Exhibit 1 summarizes how these two funds' processes compare.

Despite their differences, both funds received Positive Process Pillar ratings because both construction approaches should lead to attractive risk-adjusted performance over a full market cycle. But USMV received a higher overall Morningstar Analyst Rating because of its superior diversification, turnover limits, and lower fee.

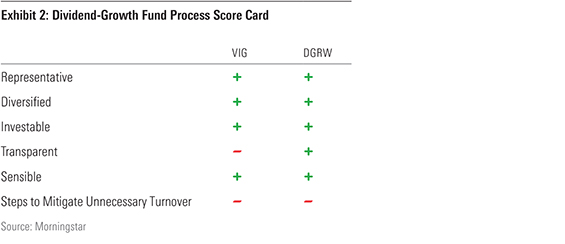

Case Study 2: VIG vs. DGRW

In contrast, the Bronze-rated WisdomTree fund ignores past dividend growth. Instead, it targets dividend-paying stocks with high profitability over the past three years and a strong forecast for earnings-growth rates over the next three to five years. It then weights its holdings based on the value of their dividend payments. This tilts the portfolio toward healthy firms that may have the capacity to increase their dividends in the future. But it ignores managers' actual behavior, which is an important indication of their willingness to raise their dividends.

Despite their differences, both funds are representative of the dividend-growth investment style. In fact, 65% of VIG's portfolio currently overlaps with DGRW's. Both funds favor highly profitable firms with durable competitive advantages that should have the capacity to sustain their dividend growth. They are also both well-diversified, their indexes are investable, and their strategies are sensible. Although VIG's principal strategy is straightforward, DGRW earns a higher mark for transparency, because of the former's secretive proprietary screens. Neither fund takes steps to mitigate unnecessary turnover, though VIG's market-cap-weighting approach should require less turnover than DGRW's dividend-weighted portfolio. And transaction costs in this highly liquid large- and mid-cap market segment are generally modest. Exhibit 2 summarizes how these two funds' processes compare.

Both funds earn Positive Process Pillar ratings. However, VIG received a higher Analyst Rating because its focus on long-term dividend-growth consistency gives it greater exposure to stocks with shareholder-friendly management teams and stable cash flows. Consequently, it will likely hold up a little better than DGRW during market downturns. Its lower expense ratio also contributed to its higher rating.

Index construction matters because it can have a significant impact on a fund's performance relative to its peers over the long term. Aside from cost, it is the most important factor to evaluate before selecting an index fund.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/d10o6nnig0wrdw.cloudfront.net/04-18-2024/t_34ccafe52c7c46979f1073e515ef92d4_name_file_960x540_1600_v4_.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-09-2024/t_e87d9a06e6904d6f97765a0784117913_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)