Like Snowflakes, No Two Bear Markets Are Alike

There are no absolutes when it comes to value versus growth.

/s3.amazonaws.com/arc-authors/morningstar/e6b4cff4-0d77-4881-abc5-5b0b34d64bf6.jpg)

A longer version of this article was published in the November 2016 issue of Morningstar FundInvestor. Download a complimentary copy of FundInvestor by visiting the website.

When I was starting my career as a Morningstar analyst in the late 1990s, one of my closely held beliefs was that value stocks were lower-risk than growth stocks. I believed that value-oriented funds would always hold up better in a bear market than those that owned growth stocks.

After reading books by Martin Zweig and David Dreman, I believed that the low price multiples of value stocks meant that they inherently had less risk than growth stocks. Expectations were, by definition, lower for value stocks. Meanwhile, I interpreted growth stocks’ higher price multiples to mean that any slip in company fundamentals would ravage their share prices. I had a lot to learn.

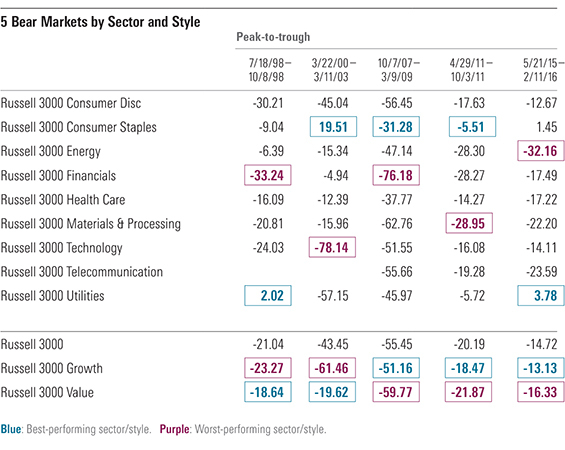

But, in the short run, value stocks did weather the storm better during the next two bear markets. (See the table.) The first came in 1998's third quarter when Russia devalued the ruble and defaulted on its debt. This occurred while the dot-com bubble in the United States was still inflating. From mid-July through early October 1998, the Russell 3000 Index, a proxy for the U.S. stock market, fell 21%. Growth stocks did a bit worse, with the Russell 3000 Growth Index dropping 23.3%, while the Russell Value Index fell a milder 18.6%.

- source: Morningstar Analysts

Value stocks outperformed by a wider margin during the next bear market. When the dot-com bubble finally burst in March 2000, growth-oriented technology stocks--and Internet stocks in particular--were truly priced for perfection. Of course, Internet stocks weren’t the only shares trading at ridiculous price multiples. Huge swaths of the equity market were overpriced. Even mature companies like

Even so, growth stocks, and technology shares in particular, took the brunt of the bear market that began in March 2000. The pain lasted for nearly three full years, and the Russell 3000 Growth Index fell a brutal 61.5%. The Russell 3000 Technology Index collapsed by nearly 80%. Value stocks, many of which were ignored by investors during the late 1990s rally, dropped just under 20%, as measured by the Russell 3000 Value Index.

But anyone who bet on a value index would have been worse off during the next three downturns. That’s because not every bear market targets stocks selling at high price multiples. Growth fared better in 2007–09, 2011, and during the recent 2015–16 correction because the sell-offs were focused on financials and later on energy, two historically value-oriented sectors.

So, it’s very difficult to know whether value or growth stocks will endure the next bear market better than their counterparts. No two bear markets are the same, and the catalysts behind them tend to change. There is usually one sector that gets hit particularly hard, but it is difficult to anticipate which one it will be. The 1998 bear market was, as mentioned above, sparked by the Russian default. Given that it was a debt crisis, financials were hit the hardest with the Russell 3000 Financials Index dropping 33.2%. Alternatively, utilities provided a safe haven (as they did during the recent 2015–16 correction). But the roles of those two sectors reversed during the 2000–03 bear market. Financials dropped by just under 5%, while utilities fell an incredible 57%, second-worst behind technology stocks.

Reversion to the Mean Whichever style or sector has been in favor tends to get hit the hardest during the next bear market. This is the idea behind reversion to the mean. While reversion to the mean almost always happens eventually, it is very difficult to know when it will happen. Often, it can take far longer than one expects. Alternatively, beaten-down sectors can come in for another round or two of pain. Financials were not the best-performing sector heading into the mid-2011 downturn, but they were still one of the hardest-hit sectors. Similarly, growth stocks had already been doing better than value stocks heading into the 2015 correction, but they still held up better during the downturn.

So, unfortunately, there are no absolute guidelines for protecting one’s portfolio during a bear market. The best one can do is prepare in advance by suitably diversifying. It is also critical to understand the risks inherent in each fund one owns. In addition, don’t try to fight the last war. Don’t assume that what worked recently or in the previous bear market will work next time.

But, perhaps most important, when the next bear market does strike, remain calm. A bear market is the worst time to be reactionary. Plan in advance and stick to it.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IGTBIPRO7NEEVJCDNBPNUYEKEY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/e6b4cff4-0d77-4881-abc5-5b0b34d64bf6.jpg)