Indexing in Less-Efficient Markets

The case for index investing rests on the index fund's cost advantage and how representative it is of its actively managed peers, not market efficiency.

/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)

A version of this article was published in the August 2016 issue of Morningstar ETFInvestor. Download a complimentary copy of ETFInvestor here.

Intuitively, the case for index investing seems the strongest for more-efficient areas of the market, like U.S. large-cap stocks. Here, information is easy to obtain and widely disseminated. So prices should reflect all available information, making it difficult to consistently outperform without taking on greater risk. In less-competitive markets, it may be easier to obtain an informational edge, or identify mispriced securities, giving savvy investors a better chance to outperform.

In theory, that story makes sense, but it often breaks down in practice. According to data published in the June 2016 installment of Morningstar's Active/Passive Barometer, 14.8% of all actively managed U.S. large-blend funds survived and outpaced their passive counterparts during the 10-year period ended June 30, 2016. The success rates for the U.S. small-blend (26.1%), foreign large-blend (33.1%), intermediate-term bond (39.0%), and diversified emerging-markets stock (32.4%) Morningstar Categories, which many view as less efficient, were higher but still shy of 50%.

It is tempting to view active managers as informed investors with a chance to collectively outperform, profiting at the expense of less-sophisticated individual investors. But the reality is that many of the supposedly less-efficient areas of the market are still fairly competitive. And even when that is not the case, active investors' asset-weighted average performance should be similar to a representative benchmark gross of fees. Outperformance is a zero-sum game, and a negative-sum game after accounting for fees. If there are greater opportunities for skilled managers to outperform in less-efficient markets, it is also true that unskilled managers here can hurt investors more.

So the case for index investing isn't necessarily weaker in less-efficient markets. Rather, it depends on how well the index represents the waters where active managers are fishing, the size of the cost hurdle active managers must clear, and investors' confidence in their ability to identify skilled managers and/or winning investment strategies. The remainder of this article will focus on the first two factors to examine the case for index investing in the U.S. small-blend, foreign large-blend, intermediate-term bond, diversified emerging-markets stock, foreign small/mid-blend, and high-yield bond categories.

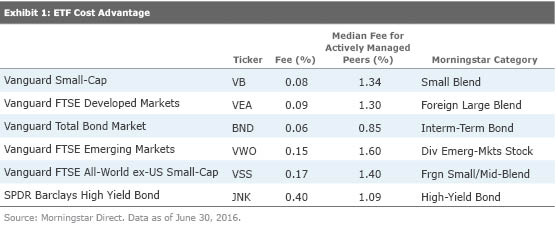

Low-Cost Options Fees are one of the best predictors of future relative performance (the lower the better). As index funds' cost advantage over their actively managed counterparts increases, so does the strength of the case for investing in them. Exhibit 1 highlights one of the lowest-cost index funds in each category that I will examine here.

In all four equity categories, the index funds' cost advantage relative to the median active fee exceeded 1.2 percentage points at the end of June 2016. In other words, more than half of all actively managed funds in these categories have to generate annualized gross returns that are at least 1.2 percentage points higher than these exchange-traded funds to offer the same returns net of fees. That's no small task. However, there are lower-cost actively managed options available that should have a better chance to outperform. The cost advantage relative to the median active fund was the smallest in the high-yield bond category.

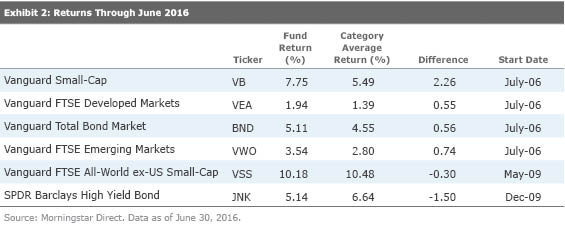

Low fees should translate into attractive category-relative performance over the long term. That was the case in four of the six categories, as Exhibit 2 shows. In contrast to those groups, data for the two index funds that lagged their survivorship-bias-adjusted category averages started after the 2007–09 market downturn.

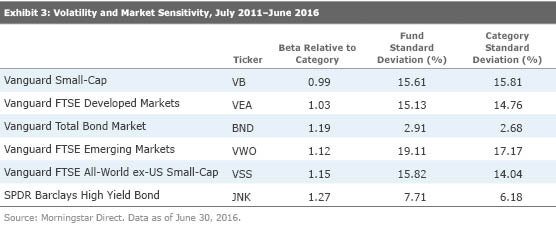

Active managers tend to carry larger cash balances than their passively managed counterparts to manage redemptions, which can create a small drag on their returns over the long term. This may also help explain why five of the six index funds were more sensitive to market fluctuations (had higher market betas) during the trailing five-year period through June 2016 than their respective category averages. But most of these performance differences are attributable to differences in their holdings.

Fishing in the Same Pond? If an index fund's portfolio is representative of how active managers are investing, its long-term performance should be comparable to that of its typical actively managed peer, gross of fees. And if it charges a lower fee, as most index funds do, it should come out ahead net of fees. But this cost advantage could prove less reliable in cases where active managers invest differently than the index. This could occur because they may either invest in assets the index excludes or invest differently from other market participants. For example, the investment-grade-focused Barclays U.S. Aggregate Bond Index would not be representative of intermediate-term bond managers who dip into high-yield bonds to boost their returns.

Vanguard Small-Cap ETF VB and

Vanguard FTSE All-World ex-US Small-Cap ETF VSS and

The biggest differences between VWO and its U.S.-based active peers are that it has greater exposure to stocks listed in China and excludes South Korean stocks. Chinese stocks accounted for about 28% of VWO's portfolio at the end of June, while the corresponding figure for the average active fund in the category was 17%. Most U.S. active managers don't feel comfortable with such a large weighting in a single emerging market. The large China weighting in the index VWO tracks reflects Chinese investors' holdings. Many of the largest stocks in this market are state-owned enterprises, which may prioritize political objectives over long-term profit maximization. This risk should be reflected in market prices. But the case for traditional index investing is still weaker in emerging markets because active oversight here can improve diversification and reduce risk. Active managers also have the flexibility to invest in developed-markets stocks with high exposure to emerging markets, which are not eligible for inclusion in most emerging-markets indexes.

The two fixed-income index funds were the least representative of their respective active peer groups. Market-cap weighting skews these portfolios toward the most heavily indebted issuers. This gave

Summary

- The case for index investing is not dependent on market efficiency. Rather, it rests on the cost hurdle active managers must clear, how representative an index is of active managers' opportunity set, and investors' confidence in their ability to select winning funds.

- Low fees should translate into attractive category-relative performance for index funds that are representative of the waters their active peers are trolling.

- The case for market-cap-weighted index investing is stronger for U.S. and foreign developed-markets stocks than it is among fixed-income and emerging-markets stocks.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)