Avoid Leveraged and Inverse ETFs

They're only meant to be a one-day holding, and during that period you're just guessing.

/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)

A version of this article was published in the July 2016 issue of Morningstar ETFInvestor. Download a complimentary copy of ETFInvestor here.

It is hard to overstate the risks of owning leveraged and inverse exchange-traded funds. These funds are designed for a one-day holding period, a horizon over which price movements are unpredictable. And (with the exception of single inverse ETFs) they amplify those movements. Over holding periods longer than one day, their performance can diverge sharply from what many investors might expect. For example, during the trailing 12 months through May 2016, the S&P 500 returned 1.72%, while ProShares UltraPro S&P 500 UPRO, which targets 3 times the daily return of the S&P 500, lost 5.3%.

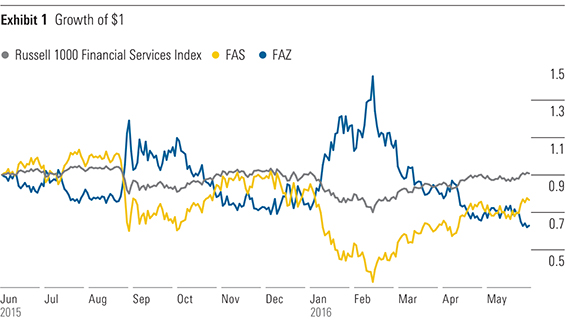

Direxion Daily Financial Bull 3X ETF FAS and Direxion Daily Financial Bear 3X ETF FAZ further illustrate how performance can deviate from targeted exposures over periods longer than a day. FAS and FAZ attempt to provide 3 times the daily return and inverse return, respectively, of the Russell 1000 Financial Services Index. From June 2015 through May 2016, the index returned a meager 0.64%. A little leverage should have boosted that return, right? Not quite. FAS lost 11.3%, while FAZ lost 22.9%. The chart below shows how the performance of these funds has diverged from the index's.

Source: Morningstar.

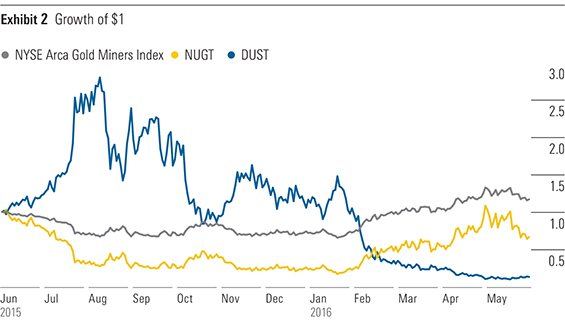

Those losses look tame compared with Direxion Daily Gold Miners Bull 3X ETF NUGT and Direxion Daily Gold Miners Bear 3X ETF DUST. NUGT and DUST target 3 times the daily return and inverse return, respectively, of the NYSE Arca Gold Miners Index. That index returned 16.9% from June 2015 through May 2016. Not surprisingly, DUST suffered a painful decline, losing 87.9% of its value. But NUGT also lost a hefty 33.8%, a far cry from what many might expect from a bullish fund when the underlying index had strong performance.

Source: Morningstar.

This type of divergence can occur because these funds reset their leverage ratios or short positions at the end of each day to maintain their targeted exposure to the daily price movements of their underlying indexes. For example, without any adjustments, UPRO's leverage ratio would decline on days when the S&P 500 is up because the index swaps that it uses to achieve leverage have a constant notional value. It has to increase its long positions after the market has gone up and trim them after it has declined to maintain a constant leverage ratio. This means that the absolute amount of leverage the fund takes relative to each investor's initial investment changes over time. And depending on the underlying index's path, the fund could return more than 3 times the index over periods longer than a day, or far less.

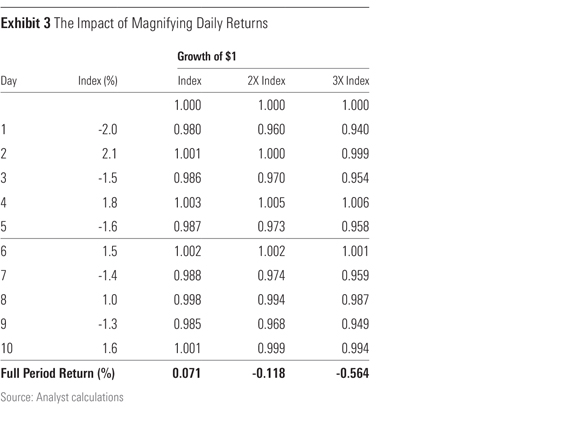

Leverage can hurt performance over the long term because it magnifies volatility, which in turn increases the asymmetry between gains and losses. For example, if a fund loses 2%, it must gain 2.04% to break even. But if it loses 10%, it takes an 11.1% return to get back to even. As volatility increases, so does the potential drag on returns. This is why the 3 times leveraged UPRO lost more than ProShares Ultra S&P 500 SSO (0.9%), which is 2 times leveraged, over the period cited above. A stylized example should make this point clearer. The table below shows the daily returns for an index and the growth of a dollar invested in that index, as well as funds that target 2 and 3 times the index's daily returns.

Even though the return on the index was slightly positive over the full 10 days, the 2 times leveraged fund lost 0.12%, and the 3 times leveraged fund lost even more. This volatility drag can weigh on the performance of leveraged and inverse funds during long holding periods.

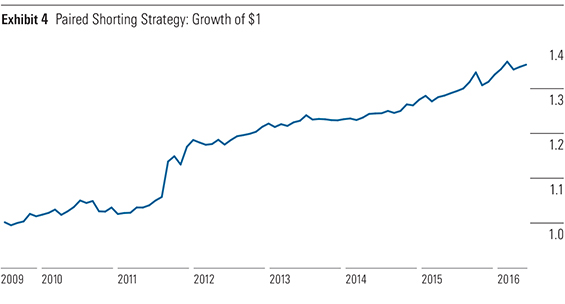

Betting Against Leveraged and Inverse ETFs The volatility drag and high expense ratios that plague leveraged and inverse funds got me thinking: If these funds are as bad as they seem, could it be profitable to bet against them? To test this idea, I constructed a portfolio evenly split (50%) between short positions in UPRO and ProShares UltraPro Short S&P 500 SPXU, which targets 3 times the inverse daily return of the S&P 500. Importantly, I only reset the short positions once a month to mitigate the volatility drag. Daily rebalancing would leave a similar payoff to long positions in the underlying funds.

Shorting SPXU translates into leveraged long exposure to the market, while the short position in UPRO hedges out that exposure. Because these positions are only rebalanced once a month, it is possible to have net long or net short market exposure during the month. But this net market exposure should be small.

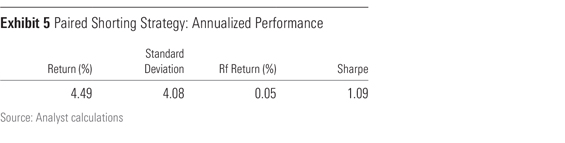

Ignoring transaction costs, this paired shorting strategy would have returned 4.49% annualized from July 2009 through May 2016, with low volatility. Fees accounted for nearly 1 percentage point of this return (when you're short these funds you're collecting their fees, not paying them). The remainder of the return came from reducing the volatility drag by rebalancing the short positions monthly, instead of daily, as the ETFs do.

I ran a regression analysis on this strategy to determine whether its apparent success could be attributed to common factors, including market risk exposure, size, value, and momentum. The strategy had slightly negative exposure to the market-risk premium, suggesting that it was net short the market, which detracted from performance over the sample period. It did not have any have significant exposure to the other factors, and yet it still paid off.

In reality, it is probably not feasible to implement this strategy. Transaction costs, including the costs associated with borrowing shares to sell short, can quickly erode its returns. Also, investors may have to contend with margin calls that can make it difficult, if not impossible, to maintain the requisite short positions. But this exercise demonstrates that the game is stacked against investors who take long positions in leveraged and inverse funds.

Alternatives For all their flaws, leveraged and inverse ETFs do have a couple of minor advantages. They don't require a margin account. And the most investors can lose in inverse funds is 100%, while the potential losses on a naked short are unlimited.

It is best to avoid these funds altogether. They are only designed for a one-day holding period, and making a bet over that horizon is no different than going to a casino. Those determined to use leverage with a time horizon longer than a day would likely be better off using a margin account because it would allow them to maintain a constant amount of leverage relative to their initial investment. Bearish investors interested in limiting potential losses would probably be better off using put options. That said, these alternatives are still very risky and are not appropriate for most long-term investors.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/d10o6nnig0wrdw.cloudfront.net/04-18-2024/t_34ccafe52c7c46979f1073e515ef92d4_name_file_960x540_1600_v4_.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-09-2024/t_e87d9a06e6904d6f97765a0784117913_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/56fe790f-bc99-4dfe-ac84-e187d7f817af.jpg)