Do Objectives-Based Funds Deliver?

The results haven't matched the hype for objectives-based funds.

/s3.amazonaws.com/arc-authors/morningstar/44f33af1-4d5c-42fb-934a-ba764f670bc6.jpg)

Objectives-based investing has moved to the asset-management industry's fore in recent years, but the results haven't matched the hype. In our recently released report, we reviewed over 1,000 distinct multiasset funds to identify strategies aiming to provide what investors most commonly seek from objectives-based portfolios: income, target returns, volatility protection, and inflation protection. A healthy number of funds accomplish their objective, though comparable blended indexes would do the same and usually with higher returns and lower volatility. Instead, the markers of worthy objectives-based investments are similar to those of other strong funds, and we indicate them through our Morningstar Analyst Ratings.

Background: Financial-Planning Origins We use the term "objectives-based" to describe funds that seek to address a specific investor preference or problem, which is in contrast to a more traditionally oriented strategy that seeks to provide exposure to a certain asset class; they're also sometimes referred to as "goals-based," "outcomes-based," or "solutions-based" investing.

But before delving more deeply into objectives-based investing, it is handy to understand the movement's antecedent in goals-based financial planning. Whereas the traditional planning process typically begins with investors and their advisors picking a conceptually acceptable level of risk and return, goals-based planning begins with more concrete and measurable goals. Goals might include having enough money to fund college education, retirement, or even material possessions like boats and vacation homes. The measure of investor success isn't necessarily centered on beating a benchmark. Instead, it more holistically takes into account the interactions between savings, spending, time horizons, and expected investment returns to maximize the probability of achieving the goal.

Asset-management firms have noticed this shift in benchmarking perspective and responded in kind. Some of the newly developed or rejiggered multiasset funds can be easily slotted into a goals-based financial plan. That financial-planning process often takes a goal and backs into the required rate of return needed to achieve it; target-return funds are tailor-made for that approach. Objectives-based funds can also be used to address certain investor preferences, such as a smoother return stream or protection from inflation. In those cases, the focus changes from what is in the portfolio--for instance, blue-chip stocks or Treasury Inflation-Protected Securities--to why it is in the portfolio.

Investing with a specific objective or goal in mind isn't new. One can argue that this motif also extends to target-date retirement funds and the age-based portfolios found in 529 college-savings plans. What is newer, though, is the way some objectives-based funds have been positioned to investors--as strategies whose value derives from their ability to satisfy the goal concerned. In effect, it shifts the yardstick from how well the fund performs versus a benchmark index to how well it satisfies the specified objective.

Meeting the Objective, Not Beating the Index

Not surprisingly, funds with an objectives-based angle generally meet their objectives, partly because those objectives can be so ambiguously defined. However, they're not nearly as successful when measured against a passively managed blended index. Take income-oriented funds, for instance, which generally have little trouble producing above-average income. However, investors in the average income-oriented fund could have achieved similar returns with lower volatility and with more control over the timing of income using a total-return approach that sold fund shares as needed. In fact, that change in view was signaled in the 1990s when many bond funds shifted from a pure yield focus to a total-return approach as championed by

The pattern of meeting the objective but failing to beat the blended index extends to the other objective-based funds as well. The average volatility-protection fund typically cushioned losses in months when the S&P 500 declined but lagged when it climbed; a blended equity and fixed-income index delivers a similar pattern of returns, though with markedly better downside protection, which results in better risk-adjusted results.

Target-return funds, also known as absolute return funds, by and large attempt to produce positive returns regardless of the market's direction. Most target-return funds produce positive returns over long-enough measurement periods. But so does a simple blended index, which has even better returns and lower volatility than most target-return funds.

Inflation-fighting funds have come out ahead of inflation, as measured by the Consumer Price Index for All Urban Consumers, during the past decade's mild inflationary environment. Their reliance on commodities and REITs has produced notably volatile results, especially compared with a blended index or the inflation-protected bond category average--the latter two have also produced better gains during that time.

It's Hard--but Not Impossible--to Beat the Index A healthy number of objectives-based funds seem to accomplish their goals, but it appears the same objectives could have been met far more simply, and at a sharply reduced cost, by using index-based balanced portfolios. Indeed, though the managers of these funds employed specialized asset classes, sophisticated tools, and techniques like tactical asset allocation to meet their objectives, they were still bound by the reality that applies to any type of active strategy--it is hard to beat passive indexes after accounting for fees.

To be sure, that doesn't mean objective-based funds completely lack merit. In fact, we recommend a number of objectives-based funds. But we don't believe that investors should apply a different set of criteria when evaluating the merits of an objectives-based strategy. Rather, we believe the markers of worthy objectives-based investments are similar to those of other strong funds: They're run by a talented, committed management team ("People"); they leverage a prudent, repeatable process ('Process"); they're backed by a parent firm that puts shareholders first ("Parent"); and they're reasonably priced ("Price") while boasting attractive past performance ("Performance").

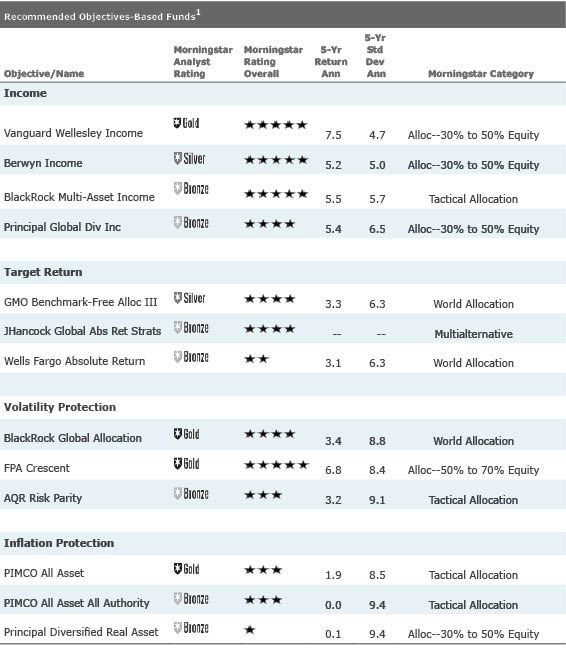

We rate and recommend funds based on the People, Process, Performance, Parent, and Price Pillars that underlie the Morningstar Analyst Rating. For investors looking for funds that address income, target-return, volatility-protection, or inflation-protection objectives, the table lists the funds that we recommend, as designated by an Analyst Rating of Gold, Silver, or Bronze. A Morningstar Medalist rating indicates our conviction in a fund's ability to outpace its index and peer group over a full market cycle. During the next few weeks, we'll dive into the details of each subset of objectives-based funds, including our assessment on the likelihood of the below funds achieving their intended objective.

[1] On June 6, 2016, we put the Analyst Ratings for GMO Benchmark-Free Allocation and its more expensive clone, Wells Fargo Absolute Return, under review because of personnel changes. Comanager Sam Wilderman, a 20-year veteran of GMO, will leave the firm at the end of 2016, and GMO also laid off roughly 10% of its 650-person staff in the past few weeks. While the continued presence of longtime lead manager Ben Inker at the helm and GMO's deep asset-allocation resources provide a solid foundation for the fund, the team changes are substantial, and we are currently assessing their impact on the fund's prospects.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IGTBIPRO7NEEVJCDNBPNUYEKEY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/44f33af1-4d5c-42fb-934a-ba764f670bc6.jpg)