Markets Churn Violently in Early 2016

Strong equity returns in March brought the market back to where it started the year.

Equity markets have gone almost nowhere year to date. Emerging markets have done the best, gaining about 5%, and Japan the worst, down about 7%. Europe was also down but by a smaller amount, and the U.S. S&P 500 has returned about 2% year to date. However, that relative calm belies some powerful volatility.

Rough Start to 2016

From the beginning of 2016 to Feb. 11, almost all major equity markets and commodity markets received a beating ranging from 7% to 11% declines. Equity markets were driven down by worries about collapsing energy prices and the potential impact on oil companies, their lenders, and financial market participants more generally. More worries and better recognition of China's slowing growth prospects didn't help. U.S. economic data released in early 2016 was mixed, though an artificially weak initial print of fourth-quarter GDP growth (later revised higher to 1.4%) fueled the bear case. The weak GDP report seemed to suggest that falling energy prices and a slowing China were beginning to hinder growth, even in the United States.

Energy- and Central Bank-Related Rumor Mills Halt Market Decline

Some of those worries came to an end in mid-February, when some economic reports for January showed better data in the U.S. and Europe. Rumors of an energy producers' meeting to curb output stopped the decline in energy prices. The day energy prices bottomed was just a day or two ahead of the equity market trough, which was Feb. 11. This stabilization in energy prices, better economics news, and increasing rumors of central bank easing sparked a major rally in equity and commodity markets between mid-February and mid-March ranging from 7% to 16%, erasing most of the earlier equity losses.

Investors Buy Stocks on Central Bank Action, Pause on the Actual Monetary Changes

As typical, markets correctly anticipated that early 2016 economic and stock market weakness would trigger a lot of central bank actions. It didn't hurt that a lot of central bankers began whispering about more easing in February. In fact, by the time the European Central Bank instituted another wave of monetary easing on March 10 and the U.S. Federal Reserve decided to not hike interest rates on March 16 (with Fed governors indicating that two rate rises were likely in 2016, instead of the previous expectation of three or four increases), markets had already had their rally. Since leveling off around March 18, most equity markets have done little. Terrorist activities in Europe and worries about the potential exit of the United Kingdom from the European Union have caused modest losses in Europe over the past month, while emerging markets have gained about 3% as purchasing manager data out of China finally managed to show improvement in March (as it did the U.S. and Europe). The U.S. hasn't done quite as well, as recent worries about consumption growth, slowing auto sales, and the potential for a sub-1% growth rate for the first quarter held back U.S. equities over the past month.

Central Bank Easing and Goldilocks Growth Rates Make Bonds a Star Performer

Bond yields around the world have generally eased throughout 2016, driving high total returns for bonds so far this year. The 10-year U.S. Treasury yield has fallen from 2.2% at the end of 2015 to just 1.8% recently even in the aftermath of the Fed's first rate increase in December and promises to raise rates further in 2016. German bond rates have also continued to decline in 2016. Both the 2-year and 5-year German bonds carry negative yields, and even the 10-year German bond yields a miserly 0.1%. Most bond funds have returned 3%-4% year to date, with even high-yield and emerging-market bonds doing well. Much of that return was earned just in the past month. Emerging-market bonds have been the best performers, returning more than 5% year to date. A combination of central bank easing, fewer worries about catastrophic financial damage from falling energy prices, and better news out of China have helped even risky bonds do well. Those strong-performing bonds (year to date and monthly) include U.S. high-yield bonds that did so poorly early in 2016.

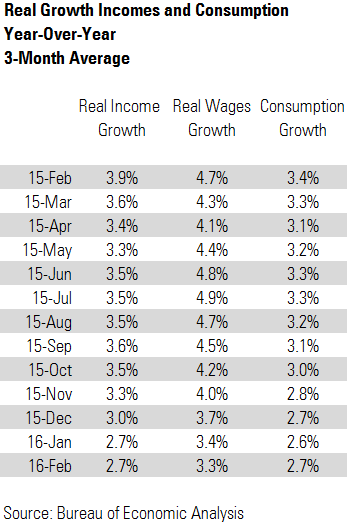

Slowing Total Wage Growth and Higher Inflation Give the Consumer Pause

The U.S. economy has become a very lopsided stool lately, with consumer spending and to a lesser degree housing driving U.S. economic activity over the past five quarters. In fact, as other sectors including net exports, inventories, and business investment spending have shown occasional outright declines, the consumer contribution has accounted for all (or even more) of the growth in GDP in four of the five most recent quarters. However, with total slowing wage growth (a function of employment, hours worked, and hourly wage growth), consumption growth appears to have slipped a bit in the first quarter. We believe faulty seasonal factors and odd weather patterns are as much a problem as any modest worsening in consumer fundamentals. Slower consumption growth is the primary reason we believe that overall GDP growth could fall below 1% in the first quarter.

Wage and Income Data Continue to Support a Stabilization of Consumption Growth

We aren't terribly concerned about the apparent short-term slowing in consumption data. Weak consumption data has weighed on first-quarter results in most recent years despite seasonal adjustment factors. First-quarter consumption performance, on a sequential quarterly basis, has shown the worst growth rates of the year compared with the other three quarters in three of the past four years. We note that wage, income, and consumption data have all slowed. Still, wage growth remains in excess of consumption growth, and real income growth remains at the same levels of consumption spending.

We do acknowledge that recent consumer data is softer than we like; this is perhaps fueled by a sharp rise in gasoline prices from $1.72 in mid-February to $2.07 in mid-April, which could be causing some consumers to reconsider purchases of gasoline-gobbling pickup trucks and SUVs.

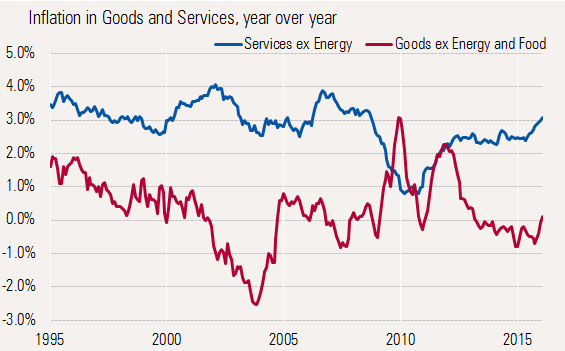

Higher Prices Remain a Concern

While consumer prices are likely to remain relatively calm on a year-over-year basis for a few more months, we are deeply worried about relatively high services inflation. In the U.S. consumer price report for February, shelter prices, mainly rent, jumped 3.3% year over year, the highest level since 2007. Medical prices were up 3.5% year over year, the highest level since 2012. Health insurance is up 6% year over year, and motor vehicle insurance rates moved higher as well, increasing 5.1%. So far, low energy prices and deflation in the price of many goods (often imported goods that have seen prices fall as the dollar has increased) have managed to offset higher services inflation. However, as energy prices and the dollar begin to stabilize, services inflation is likely to shine through and raise headline inflation above 2%, perhaps as early as this fall.

- source: BLS and Morningstar Calculations

Higher inflation, unless combined with higher wage growth, is not great news for consumers or the general economy. Inflation remains our biggest worry in the year ahead.