Healthcare: Drug Reform Worries Are Overblown

Concern over unlikely U.S. drug pricing reforms has led to favorable valuations in healthcare.

/s3.amazonaws.com/arc-authors/morningstar/a90c659a-a3c5-4ebe-9278-1eabaddc376f.jpg)

- A major factor driving down healthcare stocks is the increasing political rhetoric coming from the U.S. presidential campaign calling for lower drug prices, but we expect pricing power for drug and biotech companies to remain strong.

- Adding some floors to healthcare valuations (especially smaller potential healthcare targets), mergers and acquisitions continue at a rapid pace as large conglomerates look for growth avenues and opportunities to cut costs and taxes, while cash levels continue to build.

- Excellent clinical data in specialty-care areas such as oncology and immunology are showing an increase in the productivity of drug and biotech companies.

Democratic presidential candidates' potential drug policy reforms have pressured drug stocks, and ongoing political campaigns are likely to continue to create volatility despite the Republican-majority Congress and the low probability of reforms passing into law. Among all the reforms, dual-eligible legislation--offering mandatory Medicaid-level drug rebates to some Medicare Part D beneficiaries--looks the most likely, and most impactful (5% earnings cut on average). However, if eventually passed, we expect most drug firms to be sheltered from a strong impact, either by global diversification, high exposure to biologics, or a focus on drugs that serve a younger demographic. Further, flawed bills and a U.S. culture focused on freedom of drug choices set up low chances of major drug price reforms.

Healthcare firms continue to redeploy capital for mergers and acquisitions. Firms are largely focusing on increasing their growth potential through creating scale, cutting costs and taxes, and focusing on key strategic areas. Further, the persistent low interest rates are also fueling merger and acquisition trends, because cheap capital is available to fund acquisitions. One of the largest acquisitions in the healthcare space is

Within the core innovation element of healthcare moats, new data continues to emerge, particularly in specialty-care areas such as oncology and immunology, which should lead to the next generation of drugs. Development in these areas of treatment is important because these drugs tend to carry strong drug pricing, a more accommodating stance from regulatory agencies, and steep launch trajectories. For example, the recent immuno-oncology drug launches from

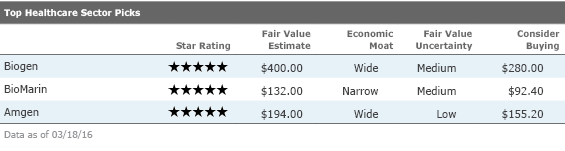

Biogen

BIIB

Biogen is the leader in the multiple sclerosis market, with a range of options for patients seeking injectables (Avonex and Plegridy), orals (Tecfidera), or high-efficacy treatments (Tysabri). Competition in MS is heating up, but we still think Biogen has a dominant portfolio that can withstand this pressure, and we assign the firm a stable, wide moat rating. We remain bullish on upcoming clinical data over a longer time horizon (2016-18) and think the firm has a promising collection of neurology-focused pipeline candidates. Recent prices appear to be giving the firm little credit for two key pipeline programs, Alzheimer's drug aducanumab and a novel MS therapy targeting Lingo. Also, the spinal muscular atrophy program (partnered with

BioMarin

BMRN

BioMarin focuses on ultrarare diseases, and its products have strong global pricing power because of the severe and rare nature of the genetic diseases they target. While Kuvan, Naglazyme, and Aldurazyme are more mature, the ongoing Vimizim launch is poised to make it BioMarin's biggest product. A very productive pipeline has kept research and development expenses high and prevented profitability, but we think the firm should be able to leap from four key marketed products to seven by the end of 2017, securing sustainable profitability at that time. While there is risk around the timing of drisapersen's approval in Duchenne muscular dystrophy, BioMarin's shares trade at enough of a discount to our fair value estimate to make the stock look undervalued regardless of our view on this regulatory outcome. Three other pipeline programs in PKU, Batten disease, and achondroplasia could reach the market by the end of 2017, and outside of DMD, BioMarin lacks competition.

Amgen

AMGN

Amgen has several innovative biologic therapies that have turned into blockbuster products and generated consistently high returns on invested capital, and we think Amgen's pipeline turnaround will continue to support the firm's wide moat. Although Amgen has heavy exposure to biosimilars--close to 40% of total sales are at risk to biosimilars over the next five years--we think the firm is well-positioned to grow throughout upcoming U.S. biosimilar launches. In the near term, fast-growing approved drugs like Prolia/Xgeva and Kyprolis, as well as Amgen's emerging cardiovascular drug Repatha, will counter biosimilar pressure. In the long term, we expect better pipeline productivity (via the deCode human genetics database) and an internal biosimilar pipeline will drive stronger growth. We expect the firm's reputation for quality biologics manufacturing and large biosimilar pipeline will allow it to gain a more than 10% share of the global biosimilar market.

More Quarter-End Insights

Stock Market Outlook: Stocks Start to Look More Attractive

Credit: Corporate Bond Markets Recuperate

Basic Materials: The Recent Commodity Rally Shouldn't Give Investors Hope

Consumer Cyclical: China Growth Concerns Present Buying Opportunities

Consumer Defensive: Lofty Valuations Persist, but a Handful of Bargains Remain

Energy: Don't Expect a Quick Recovery for Crude Prices

Financial Services: Global Bank Rout Is Overdone

Industrials: An Uneven Start to 2016, but Compelling Values Remain

Real Estate: Companies With Enduring Demand Will Persevere

Tech, Telecom & Media: Long-Term Opportunities Amid Software's Storm

Utilities: Dividends Still Attractive, but Headwinds Remain

MORN DODFX VINIX VWILX TSVA EGO WU Brightstart429plan MRO VZ MOAT T NKE CMCSA GOOG

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GQNJPRNPINBIJGIQBSKECS3VNQ.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a90c659a-a3c5-4ebe-9278-1eabaddc376f.jpg)