The Myth of 'Where to Index?'

The evidence is mostly spurious.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Dunn's Law, Redux Millions of words have been written about where investors should index, and where they should not. Much of that advice has come from Morningstar, including (back in the day) some from me.

We were all wrong.

All right, I confess, there are a few useful things to say about the subject, which I will relate shortly. But for the most part, the analysis fails. The obvious error occurs with appeals to reason, when portfolio managers explain why their fund's investment arena is unusually well suited for active management. Many say such things; few can be correct. But appeals to data, while apparently more sound, fare little better. They might be conducted more objectively, and boast the virtuous glow of evidence, but they, too, deceive. Their results melt when put to the fire.

The problem is that funds rarely invest as the benchmarks do. In theory, comparing the returns of a specialized index to the returns of a fund category tells where active managers succeed, and where they fail. If most large-value funds beat the large-value stock indexes, and most large-growth funds trail, then indexing would seem to make more sense for large growth than for large value. However, that assumption only holds true if the index and funds fish in very similar waters. If they do not, which is the case with most funds and thus most fund categories, then the numbers tell false tales.

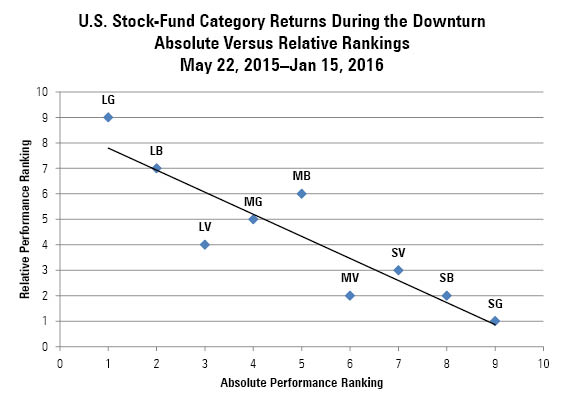

The recent market downturn offers a fine example.

Wednesday's column argued that active U.S. stock fund managers flunked their rainy-weather test; on the whole, their investors finished the eight-month stock market slump losing slightly more money than did index funds. What that column also showed, but did not much discuss, was that results differed by category. Small-company funds, in aggregate, kept pace with their index-fund competitors, but all flavors of large- and mid-cap funds trailed. Faring worst of all were large-growth funds, which lagged the Russell 1000 Growth Index for the time period by a sizable 2.29 percentage points.

In what will come as no surprise to those who read and remember September's "Dunn's Law" column, large-growth funds were the best-performing of the diversified U.S. stock-fund categories. Large-growth funds had the highest absolute returns of the nine categories, but the lowest returns relative to the index that it was benchmarked against. Meanwhile, small-growth funds had the very worst absolute returns, and the very best relative returns. Fancy that.

Best Is Worst (and Vice Versa) The overall picture looked like this:

Source: Morningstar.

That, per Dunn's Law, is the pattern that active management consistently follows. Those actively run funds that invest in the better-performing market segments tend to trail their indexes, because indexes are pure entities while actively run funds are not. In "leaving" the area of strong performance, active managers hurt themselves by being better diversified. The story is the opposite for the lagging investment sectors. In such a case, as with small-growth stocks more recently, actively managed funds benefit from diversification. For a U.S. stock fund, having fewer assets in the single worst-performing segment of the market will rarely be a bad thing.

This pattern does not depend upon the market's direction. Bull or bear, it does not matter. As long as different market segments have different returns (which they always do) and actively managed funds within a category hold a significant number of spillover assets (which they mostly do), then Dunn's Law holds. The successful active managers, per the numbers, are those managers who had the perverse good fortune of fishing in bad waters. They caught a few more fish than the index because they, unlike the indexes, also had a few lines in the good waters. The unsuccessful active managers had the opposite experience.

That, in brief, tells the story of "where to index." It is a tale that changes at each reading, because the winning and losing categories shift over time. It yields advice that should not be taken.

The Exceptions And now, the promised caveats:

1) Indexing does seem to be particularly suited for large-company U.S. stocks.

Even when Dunn's Law works in favor of large-company stock funds--that is, when blue chips fall behind the broad market--active large-cap managers don't fare well. At best, when the market tides are their most favorable (or, to continue the fishing analogy, their boats float in the most barren waters), actively run large-cap funds break even with the indexes, after expenses. Large U.S. stocks, it appears, are priced even more efficiently than are other assets.

2) Sometimes, the appeal to reason is correct.

Although I am skeptical of the breed, I do not dismiss all of its members. At some times, in some places, markets truly can be mispriced, and a diligent expert can prove very valuable. While often these tend to be niche opportunities, such as exotic corners of the bond market, it's worth noting that the mammoth U.S. housing market was widely misunderstood in 2006-07. So the mistakes can run large as well as small.

The difficulty is, how does one know at the time? As managers of all stripes will make the appeal to reason, and most are skilled at making the pitch, it takes a special talent to be able to sift through all those hopes and to identify the few claims that have some actual substance. I do not have that talent. Those who do, God bless.

3) Be careful of "lumpy" indexes.

In 1990, Japan accounted for more than 40% of the world stock market, ex-U.S. A few years later, Nokia was 70% of the Finnish stock market. An investor might have wished to purchase faithful, market-cap-weighted indexes that represented those positions. After all, those were the economic facts. But most would likely have preferred to own eggs that were not quite so large. If not at that time, then perhaps now--as both the Japan and Nokia investments were flops.

John Rekenthaler has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)