What You Need to Know About 'Strategic Beta'

As these sometimes complex new funds continue to grow, investors need to be selective, writes Morningstar’s Ben Johnson.

/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)

Morningstar's global manager research team recently published "A Global Guide to Strategic-Beta Exchange-Traded Products," its second-annual landscape report about strategic-beta ETPs. The report examines trends in asset growth, asset flows, product development, and fees by region; assesses the origins of strategic beta and the various types of risk that these strategies look to control; and provides a practical guide to analyzing strategic-beta ETPs. Below is an excerpt from this report; investors can download the complete report here.

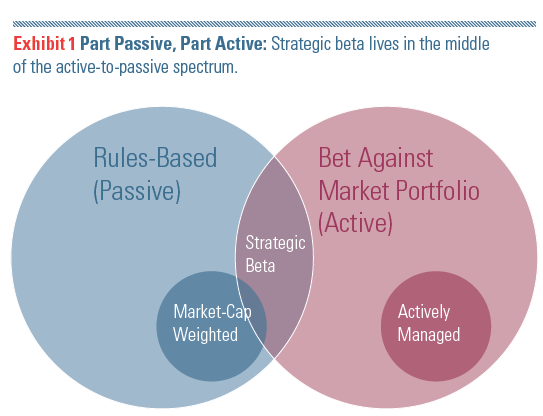

"Smart beta," "alternative beta," "enhanced indexes," "quantamental indexes"--at this point, the list of monikers describing the fast-growing middle of the active-to-passive spectrum extends long enough to put it just a few syllables shy of making a lunar landing. It's an arena that has further blurred the lines between active and passive management (see Exhibit 1), and one which is at the leading edge of the most recent wave of product proliferation within the global exchange-traded products landscape.

What Morningstar is deeming strategic beta is a broad and rapidly growing category of benchmarks and the investment products that track them. The common thread among them is that they seek to either improve their return profile or alter their risk profile relative to more-traditional market benchmarks. In the case of equity products, which account for the overwhelming majority of assets in this arena, the result is typically one or more factor tilts relative to standard market indexes.

As new products have continued to roll off asset managers' assembly lines, their sales and marketing departments have been working tirelessly to position these new models within an increasingly competitive field. The result has been a ratcheting up of the level of complexity of the indexes that form the raw stuff of these benchmark-based investment products and, in some cases, a growing disparity between how they are pitched by their sponsors and the actual investment results they produce. Investors are faced with a complex task as they navigate this landscape, and Morningstar is working to provide the compass they need to do so.

A Brief Historical Detour The proverb "There is nothing new under the sun" applies to this "new" corner of the asset-management arena. Academics distilled investment returns into their component factors decades ago. And others, most notably the eponymous founder of Barr Rosenberg Associates, had recombined these basic drivers of investment returns into investable products. In fact, Rosenberg's "bionic betas" landed him on the cover of the May 1978 issue of Institutional Investor magazine.

So why is this time different? First, there have been major advances in information and investment technology since the mid-1970s that have given asset managers the horsepower necessary to efficiently manage more-complex index strategies, to repackage them into the newest generation of strategy-delivery vessels (such as ETPs), and to deliver them at a low cost to investors. The past four decades have also been marked by steady secular growth in index investing. Since the first index fund was launched in 1975, the portion of U.S. mutual fund and ETP assets accounted for by index-tracking products has grown from nothing to nearly 30% today. All told, the investment world of today is far more ready for these sorts of strategies than it was 40 years ago, when some people, as John Bogle has reported, were calling the concept of indexing "un-American."

What's in a Name? The need to define this space, to measure it, and to police it has grown and will continue to grow with time. At Morningstar, we are positioning ourselves to meet these needs, all with the goal of helping investors make better-informed investment decisions. For our part, we have decided to tag this realm with the label strategic beta. Why strategic beta? First and foremost, we are eager to do away with the positive connotations that may be inferred by the "smart" in smart beta. Not all of the strategies included in this arena are smart, per se. The term strategic is meant to draw attention to the fact that the benchmark indexes underlying the ETPs, mutual funds, and other investment products in this space are designed with a strategic objective in mind. These objectives primarily include attempting to improve performance relative to a traditional market-capitalization-weighted index or altering the level of risk relative to a standard benchmark.

As for the beta in the name, it is not meant to imply beta in the strictest, most academic sense of the term (a measure of a security or portfolio's sensitivity to movements in the broader market). Instead, it is to highlight the fact that this is a group of index-linked investments, all of which have the goal of achieving a beta equal to 1 as measured against their benchmark indexes. Strategic beta may not roll off the tongue as easily as smart beta, but we believe it is a more accurate descriptor--one that doesn't imply that this universe is the index world's equivalent of Lake Woebegon.

It should be noted that these are merely attribute tags and not new fund categories, just as we do not have a "passive" or an "active" category. The portfolios of strategic beta funds exhibit a variety of investment styles. Our purpose in creating these descriptions is to help investors rigorously analyze this breed of funds, facilitating comparisons between those with similar strategies as well as within the context of their traditional Morningstar category.

A Motley Crew In delineating the boundaries of the strategic beta space, we have tried to be as inclusive as possible, including products that may have a variety of different processes but yield fairly similar end products, and all of which deviate in some meaningful way from their traditional broad-based index peers.

Also, it is important to note that our definition differs from some others' in that we include products tied to benchmarks that first screen candidates for a variety of attributes (value, growth, and dividend characteristics, for example) and subsequently weight the eligible securities by their market capitalization (

Our resulting universe includes a diverse range of products, spanning from the

- They are index-based investments.

- They track nontraditional benchmarks that have an active element to their methodology, which typically aims to either improve returns or alter the index's risk profile relative to a standard benchmark.

- Many of their benchmarks have short track records and were designed for the sole purpose of serving as the basis of an investment product.

- Their expense ratios tend to be lower relative to actively managed funds.

- Their expense ratios are often substantially higher relative to products tracking "bulk beta" benchmarks like the S&P 500.

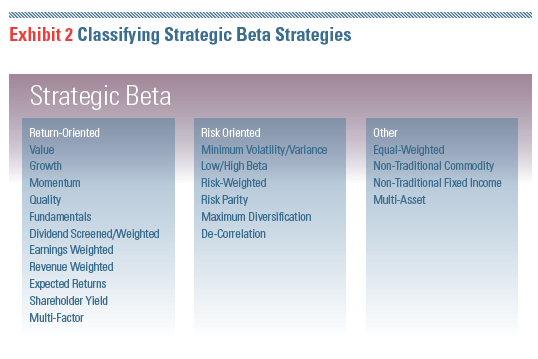

Better Returns, Less Risk? Having defined the strategic beta space in very broad terms, Morningstar makes a second cut of the universe, tagging products on the basis of the overarching strategic objective of their underlying benchmark. These objectives fall into three buckets: return-oriented strategies, risk-oriented strategies, and a catch-all "other" classification.

Return-oriented strategies look to improve returns relative to a standard benchmark. Value- and growth-based benchmarks are prime examples of return-oriented strategies. Other return-oriented strategies seek to isolate a specific source of return. Dividend-screened or weighted indexes, such as those followed by iShares Select Dividend (DVY) and SPDR S&P Dividend ETF (SDY), are the chief examples of this type of return-oriented strategy.

Lastly, "other" encompasses a wide variety of strategies, ranging from nontraditional commodity benchmarks to multiasset indexes. This second cut allows investors to classify strategic beta instruments along very broad lines.

The Devil Is in the Details The third and final cut involves classifying products with similar strategic objectives at a more granular level. Here we group products tracking dividend-screened or weighted, value, low/minimum volatility/variance, nontraditional commodity, and a variety of other benchmarks together. This is intended to facilitate more-precise comparisons between products with very similar underlying methodologies. Exhibit 2 outlines our strategic beta taxonomy in full detail.

What Comes Next? One year on, the space has continued to grow faster than the broader ETP market as well as the asset-management industry as a whole. Growth has been driven by new cash flows, new launches, and the entrance of new players—some of which are traditional, dyed-in-the-wool active managers. We expect these trends will continue and may accelerate as newer ETPs tracking new and unproven benchmarks season and more new entrants make their way into the market. This process of growth and maturation will ultimately lead to a culling of the herd, which has already begun in some geographies, albeit to a limited extent. An increasingly crowded and competitive landscape will also put pressure on fees. We have already seen instances of aggressive fee reductions for strategic-beta ETPs. We anticipate that cost-competition in this space will become more prominent in the years to come.

Disclosure: Morningstar, Inc.'s Investment Management division licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/24UPFK5OBNANLM2B55TIWIK2S4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/04-18-2024/t_34ccafe52c7c46979f1073e515ef92d4_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)