Tax-Efficient Retirement-Saver Portfolios for Vanguard Investors

A mix of tax-managed, index, and munis should reduce the drag of taxes on all-Vanguard portfolios for accumulators.

/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

Vanguard has much to offer investors who are aiming to maximize their take-home returns.

The firm is synonymous with budget-conscious investing, of course; its funds are usually among the cheapest, if not the cheapest, in their categories. But Vanguard’s cost-consciousness extends to tax matters, too. The firm views tax costs as another line item that drags on investors’ returns, so it devotes research and educational efforts to matters of tax management. Many of its funds are designed with tax efficiency in mind. For example, the firm was an innovator in creating exchange-traded funds by making them share classes of already-existing index funds, a structure that enables shareholders in the firm’s traditional index equity funds to enjoy tax efficiency on par with their ETF counterparts. The firm also fields a top-flight lineup of tax-managed funds and municipal-bond funds.

Thus, it’s easy for tax-conscious investors—that is, investors investing in taxable accounts rather than inside of a tax-deferred wrapper like an IRA—to readily build well-diversified, tax-efficient portfolios consisting exclusively of Vanguard products. In addition to a broad suite of equity index funds, the firm’s tax-managed and municipal-bond lineups are also worthy building blocks.

About the Portfolios

I’ve used the Morningstar Lifetime Allocation Indexes to inform the portfolios’ asset allocations and the exposures to subasset classes. To populate the portfolios, I employed no-load, open mutual funds that received Morningstar Medalist ratings from Morningstar’s analyst team. Most of the funds earned Morningstar Analyst Ratings of Gold, though I’ve used Silver- and Bronze-rated funds in cases when suitable Gold-rated, no-load options that are accepting new investments are unavailable.

How to Use Them

My key goal with these portfolios is to depict sound asset-allocation and portfolio-management principles rather than to shoot out the lights with performance. That means investors can use them to help size up their own portfolios’ asset allocations and suballocations. Alternatively, investors can use the portfolios as a source of ideas in building out their own portfolios. As with the Bucket portfolios, I’ll employ a strategic (that is, long-term and hands-off) approach to asset allocation; I’ll make changes to the holdings only when individual holdings encounter fundamental problems or changes, or if they no longer rate as medalists.

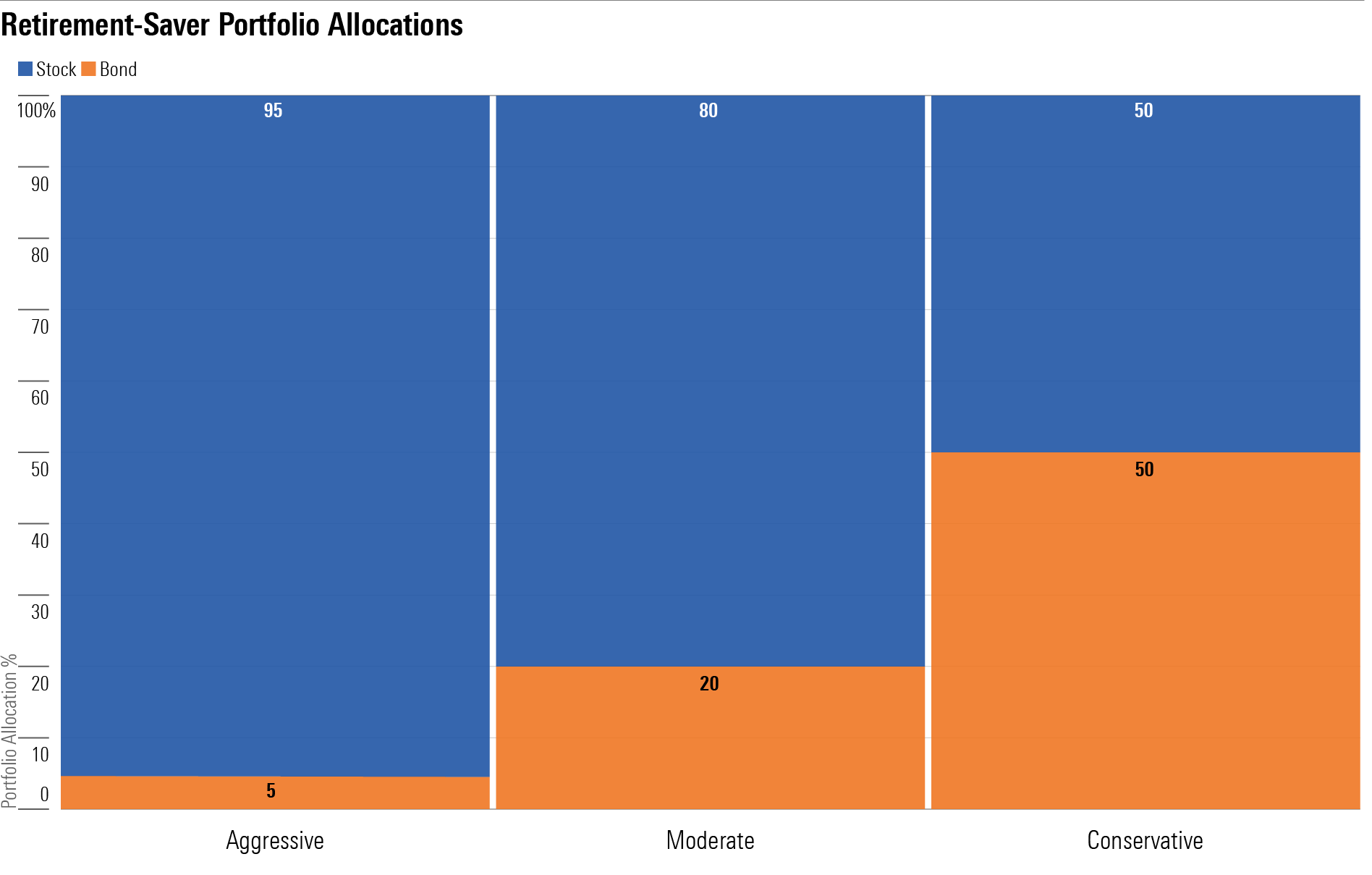

The portfolios vary in their amounts of stock exposure and in turn their risk levels. The Aggressive portfolio is geared toward someone with many years until retirement and a high tolerance/capacity for short-term volatility. The Conservative portfolio is geared toward people who are just a few years shy of retirement. The Moderate portfolio falls between the two in terms of its risk/return potential.

The portfolios are geared toward investors’ taxable accounts, so the holdings generally have good track records of limiting taxable income and capital gains distributions. Investors will also want to take a look at their tax situation when determining whether to invest their taxable portfolios’ bond positions in municipal-bond funds—which I’ve included here—or in taxable-bond funds. Most investors who are in a position to save in a taxable account—in other words, they’ve already maxed out their tax-advantaged options—are in a tax bracket where they’d benefit from holding municipal bonds versus taxable, but that’s not always the case.

Aggressive Tax-Efficient Retirement-Saver Portfolio for Vanguard Investors

Anticipated Time Horizon to Retirement: 35-40 years

Risk Tolerance/Capacity: High

Target Stock/Bond Mix: 95/5

- 45%: Vanguard Tax-Managed Capital Appreciation VTCLX

- 10%: Vanguard Tax-Managed Small Cap VTMSX

- 40%: Vanguard FTSE All-World ex-US Index VFWAX

- 5%: Vanguard Intermediate-Term Tax-Exempt VWIUX

Moderate Tax-Efficient Retirement-Saver Portfolio for Vanguard Investors

Anticipated Time Horizon to Retirement: 20-25 years

Risk Tolerance/Capacity: Moderate

Target Stock/Bond Mix: 80/20

- 40%: Vanguard Tax-Managed Capital Appreciation

- 8%: Vanguard Tax-Managed Small Cap

- 32%: Vanguard FTSE All-World ex-US Index

- 20%: Vanguard Intermediate-Term Tax-Exempt

Conservative Tax-Efficient Retirement-Saver Portfolio for Vanguard Investors

Anticipated Time Horizon to Retirement: 2-5 years

Risk Tolerance/Capacity: Low

Target Stock/Bond Mix: 50/50

- 30%: Vanguard Tax-Managed Capital Appreciation

- 5%: Vanguard Tax-Managed Small Cap

- 15%: Vanguard FTSE All-World ex-US Index

- 30%: Vanguard Intermediate-Term Tax-Exempt

- 20%: Vanguard Limited-Term Tax-Exempt VMLTX

The author or authors own shares in one or more securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LUIUEVKYO2PKAIBSSAUSBVZXHI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HCVXKY35QNVZ4AHAWI2N4JWONA.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)