While poor timing decisions continue to drag on investor returns in most fund categories, the data suggest that automatic 401(k) enrollment and dollar-cost averaging have benefited target-date fundholders over time.

Tim Strauts: A fund's published total return reflects a buy-and-hold strategy. But not all investors buy and hold. Investors move their money in and out of funds as they search for the best return.

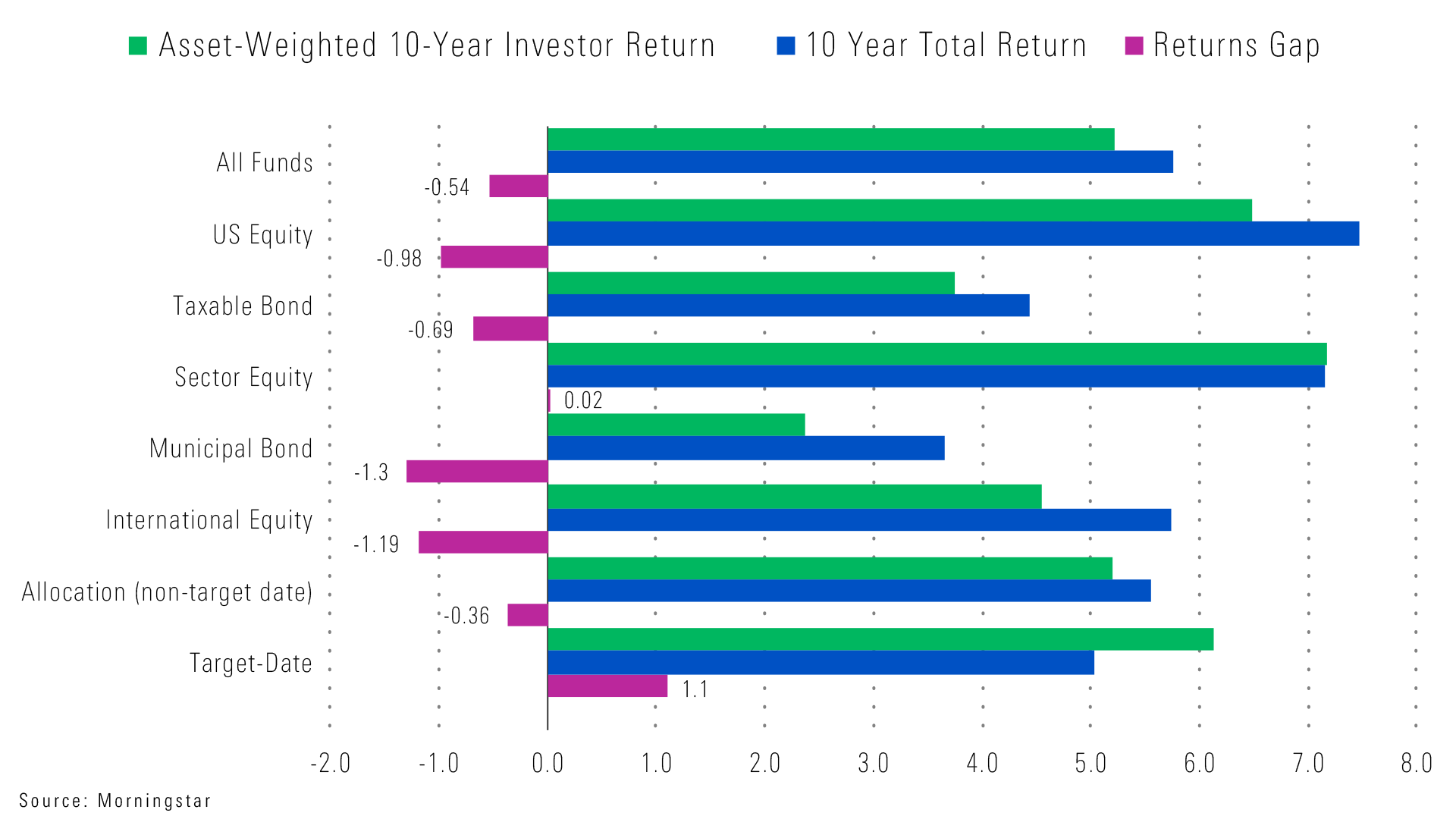

In contrast to total returns, investor returns account for all cash flows into and out of the fund to measure how the average investor performed over time.

In this week's chart, we compare 10-year total return versus 10-year investor return for the major fund categories. We then calculate a returns gap, which is the difference between the two returns.

Investors are poor market-timers because, on average, they lose half of a percent per year to poor timing decisions. Investors tend to chase performance, which leads them to buy at the top and sell at the bottom of the market cycle.

The primary goal of most investor education programs is to teach people to not market time and to dollar-cost average their money. Those efforts don’t seem to have had a big impact.

However, investors in target-date funds outperform the total return by over 1% per year. Target-date funds are used in company 401(k) plans and in many cases are the default option.

Investors who use target-date funds are investing their money on a regular basis, and they don’t seem to be trying to time the market. Many of the investors who are getting stronger investor returns are probably people that were automatically enrolled in their 401(k) and have never changed the default option.

This is a lesson to active investors that they should avoid chasing performance and try to dollar-cost average whenever possible.

{kind=link}