How Some Funds Give More Than 100% When It Comes to Asset Allocation

Long-short strategies and use of derivatives can push fund portfolios into exposure overdrive.

Question: The portfolio breakdown for one of the funds I own shows it having more than 100% long U.S. stock exposure. How is that possible?

Answer: It can be somewhat jarring at first glance to see that a fund you own has more than 100% exposure to anything. After all, there's such a thing as being fully invested--but how can a fund be more than fully invested in a particular asset type?

When a fund's asset-allocation breakdown shows it exceeding 100% exposure to an asset class, that's a pretty good indication that it's probably not your traditional long-only mutual fund or ETF. It may be that the fund is employing a long-short strategy or using derivatives to add leverage. Let's take a closer look at how each of these strategies can result in such a lopsided asset allocation.

The Long and Short of It Some funds hold both long and short positions in an effort to capitalize on stocks that the fund manager thinks will increase in value over time (long positions) as well as those the manager thinks will drop in value over time (short positions).

For those unfamiliar with how short-selling works, in a short sale the investor essentially borrows shares to sell at today's price while promising to replace the borrowed shares at a later date. If all goes according to plan, the price of the shares goes down and the short-seller realizes a profit on the difference between the original sale price and the price he or she pays to replace the borrowed shares. If the opposite occurs and the share price goes up, the short-seller loses money because he or she must pay more than the original sale price to buy replacement shares.

Some funds that employ long-short strategies use the cash generated by their short sales to buy more stock for their long sales (sometimes referred to as a "short-extension" strategy). One common approach is called a 130/30 strategy, in which the fund uses 130% long exposure and 30% short exposure for a net market exposure of 100%. This approach basically allows the manager to supercharge the long exposure, taking extra advantage of stocks he or she likes, while also potentially reaping the benefits of a short strategy for part of the portfolio. (Of course, figuring out which stocks will increase in value as well as which will decrease in value makes this strategy challenging, to say the least.)

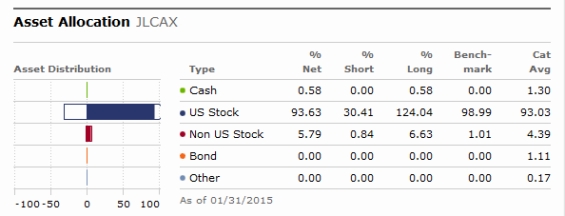

Below is the asset-allocation breakdown for JPMorgan US Large Cap Core Plus JLCAX, a large-blend fund that uses a 130/30 strategy. (The same chart type is available on all fund pages, under the Portfolio tab.)

Source: Morningstar

As you can see, the fund has a long exposure to U.S. stocks of 124.04% and a long exposure to foreign stocks of 6.63% for an overall long-stock exposure of 130.67%. Its short exposure is 30.41% (U.S.) plus 0.84% (foreign) for a total of 31.25%. Subtract the long-stock exposure from the short exposure and you get a net stock exposure of 99.42%. Add in 0.58% held in cash and you're at 100%. The bars to the left of the chart represent this range of exposures--both long and short.

In some cases, long and short exposure can be even more extreme. For example, the fund

Funds that employ long-short equity strategies are assigned to a Morningstar Category based on their beta to the S&P 500 Index, which denotes their sensitivity to the movements of the overall stock market (for example, a fund with a beta of 0.5 is sensitive to approximately half of the daily movement of the S&P 500). Funds in the Long/Short Equity category routinely use hedging or shorting strategies, resulting in betas in the range of 0.3 to 0.7. Funds that occasionally use short strategies or that use short-extension strategies but ultimately have net equity exposure of around 100% and a beta of greater than 0.7 are assigned to conventional equity categories based on their holdings style.

Leveraging Up Another fund strategy that can produce an allocation of more than 100% to a given asset class involves the use of leverage. To gain extra exposure to certain securities beyond what they can afford to buy outright, funds may use derivatives such as options and futures. Such derivatives allow funds to gain exposure to an asset without actually owning it and typically cost much less than it would take to buy the actual asset.

Morningstar's asset-allocation breakdown represents derivatives exposure as though the fund owned the underlying securities outright. Therefore, a fund that owns some shares outright and has exposure to others via derivatives will appear as though it owns all that exposure outright. To offset the potential cost of using the derivatives to purchase securities, the asset-allocation breakdown will show a negative cash exposure equal to the amount the fund would have to pay to purchase the securities. Therefore, if you see a fund with an unusually large equity exposure and an unusually large negative cash exposure, it's a pretty good indication that that fund uses derivatives.

As an example, Direxion Daily S&P 500 Bull 2X ETF SPUU is an exchange-traded fund designed to double the performance (up or down) of the S&P 500 stock index on a daily basis. Since it's not possible to own more shares outright than the ETF has in assets, it accomplishes this by owning derivatives that effectively simulate double exposure to the S&P 500. The asset-allocation breakdown on the ETF's Portfolio page shows it as having a roughly 200% long exposure to U.S. stocks and a negative 100% net cash exposure. It's an extreme example, to be sure, but it illustrates the point rather well. For more on how Morningstar's asset-allocation breakdown represents derivatives and long-short strategies, see "When Fund Asset Allocations Run Wild," and for more on the role of derivatives in funds, read "Derivatives Often Part of Fund Managers' Toolkits."

Have a personal finance question you'd like answered? Send it to TheShortAnswer@morningstar.com.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GQNJPRNPINBIJGIQBSKECS3VNQ.jpg)