Finding the True Champion Dividend-Growth Funds

There is more competition among dividend-growth funds, making it harder to truly stand out.

There is more competition among dividend-growth funds, making it harder to truly stand out.

This article was published in the May 2014 issue of Morningstar FundInvestor. Download a complimentary copy of FundInvestor here.

It pays to take a harder look at actively managed dividend-growth funds.

Investors generally like dividends, and who doesn't like growth? Put them together in a stock portfolio or in the name of a fund and they convey stability, quality, sober management, downside protection, and a growing stream of income for retirement.

We grouped funds that invest in companies that pay dividends and have the business models and cash flow that enable them to continue raising them. We found those funds' returns have kept pace with the S&P 500 Index and the average domestic-stock fund from the market's October 2007 pre-financial crisis to the end of March 2014 with less volatility. We aren't the only ones to notice, as dividend-growth funds have attracted nearly $10 billion in net inflows in the past five years through the end of the first quarter of 2014.

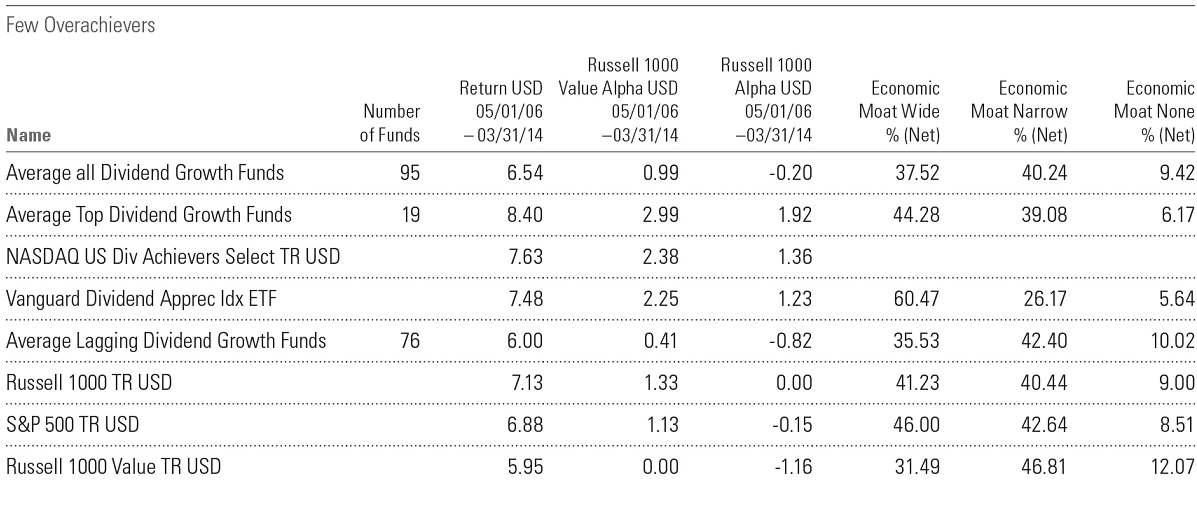

Raising the Bar

Not all dividend-growth fund records stand up to increased scrutiny. It's true many funds have been able to set themselves apart from traditional benchmarks such as the Russell 1000 and the Russell 1000 Value indexes by leaning toward stocks that pay sustainable and growing dividends, or at least declaring that they do so. Focusing on such fare has worked well over the long term for several funds in the Morningstar 500. Funds like T. Rowe Price Dividend Growth (PRDGX) have beaten the Russell 1000 and the S&P 500 by building portfolios with a better mix of dividend yield, valuation, and growth than those bogies. We raised the bar on the whole group by comparing them with dividend-growth indexes and index funds to see whether they add value above and beyond the passive options.

Besides the traditional Russell 1000 and Russell 1000 Value indexes, we measured funds versus the Nasdaq US Dividend Achievers Select Index. The trial screened for distinct large-blend and large-value funds with 12-month yields of less than 150% of the broad U.S. stock market (about 2.5% at the time of the test) that had the words "dividend" or "income" in their names--we threw out some that were more focused on yield, such as AllianzGI NFJ Dividend Value (PNEAX), and added a couple of others whose strategies were more dividend-growth-focused, such as American Funds Washington Mutual (AWSHX). It turned up more than 120 funds, about 93 of which had track records long enough for the measuring period.

The comparison examined the absolute and risk-adjusted performance of this group relative to the Nasdaq US Dividend Achievers Select Index from May 2006 to the end of March 2014. That's short in statistical terms but roughly the published life of that index and also a period encompassing a market peak, trough, and recovery. A lot of dividend-focused indexes have been rolled out in recent years to serve as the basis for new exchange-traded funds. We chose Dividend Achievers Select for its simplicity, longevity, and credibility. A fund tracking that benchmark, Vanguard Dividend Appreciation Index --available as an ETF and an open-end fund— also is a favorite of Morningstar's passive strategies analysts for its high-quality portfolio.

Bad News, Good News

The market-cap-weighted benchmark is based on the old Mergent Dividend Achievers list of stocks that have raised their dividends for 10 consecutive years. The index, however, uses some quality screens developed at the behest and with the help of Vanguard that weed out stocks with unsustainable dividends. The screens kicked out Citigroup (C), for instance, in 2006--two years before the bank slashed its dividend in the midst of the financial crisis (though it kept American International Group (AIG) and other financials).

- source: Morningstar Analysts

Click here for a larger image of the table.

The average fund in the custom dividend-growth sample edged the Russell 1000 Value in absolute terms and posted positive alpha versus that benchmark, but its results deteriorated versus the Russell 1000 and even more so against Dividend Achievers Select. The typical fund in the group lagged both more-corelike bogies and showed negative alpha when pitted against them. The typical sample fund also posted weaker results against risk-adjusted measures like the Sharpe ratio, the Sortino ratio, and Morningstar Risk-Adjusted Returns versus the Dividend Achievers benchmark.

That's bad news for dividend-growth strategies that are used to being compared with the Russell indexes, but good news for investors trying to separate the managers who are truly adding value from those who employ more-mechanical and easily duplicated approaches. In this test, Morningstar 500 denizens Amana Income (AMANX) and Vanguard Dividend Growth (VDIGX) emerged as candidates for the former group. Columbia Dividend Income (LBSAX) came close.

Small Successes

Broad-based stock-picking success helped Vanguard Dividend Growth and Amana Income. Neither portfolio had any home runs, but rather a series of small successes across industries during the period, including Nike (NKE), Bristol-Myers Squibb (BMY), and Microsoft (MSFT). Both funds did themselves a favor by avoiding financials during the crisis--Vanguard Dividend Growth by choice and Amana Income by structure. As an Islamic fund, Amana can't own financials or debt-heavy firms. Both funds have solid long-term strategies. Don Kilbride runs a more compact, almost exclusively large-cap portfolio at Vanguard, while Amana's Nick Kaiser will hold more stocks, including mid-caps.

Columbia Dividend Income lagged Dividend Achievers in absolute terms but looked competitive on some risk-adjusted measures. It had positive alpha and matched the index's Sortino and Sharpe ratios. Its larger-than-average helping of wide-moat, or competitively advantaged, companies compensated for stakes in financials like Citigroup and Lincoln National (LNC) that hurt the fund during the period, according to Morningstar attribution analysis. One of the fund's longtime managers recently retired, but remaining comanagers Scott Davis and Mike Barclay are familiar with the fund's process, which looks for a combination of yield, price, and dividend-growth potential.

- source: Morningstar Analysts

Click here for a larger image of the table.

Holding financials like Citigroup also restrained the returns of other large dividend-growth funds, such as T. Rowe Price Dividend Growth, T. Rowe Price Equity Income (PRFDX), and American Funds Washington Mutual, relative to the Dividend Achievers Index. Reasonable expenses, experienced management, and consistent processes still make these funds contenders, but so far the passive Vanguard Dividend Appreciation Index has won head-to-head.

A Tall Order

Vanguard Dividend Growth looks like the strongest for exposure to dividend-growth stocks. It has low expenses, and Kilbride has proved adept at mixing new dividend payers with old stalwarts, as well as avoiding dividend cutters. He sold AIG and Bank of America (BAC) in early 2008, for instance.

Three funds looked much worse compared with the Dividend Achievers Index: Fidelity Dividend Growth (FDGFX), Fidelity Equity-Income (FEQIX), and Fidelity Equity Dividend Income (FEQTX). It's not surprising that these funds would look erratic versus a dividend-focused benchmark. Fidelity managers historically have been more growth-leaning, and past leaders of these funds have interpreted their dividend mandates loosely. It has only been in recent years that the firm has tried to make these more than "dividend in name only" funds. All three have seen manager changes in the past three years and are, at best, works in progress. Fidelity Dividend Growth got a new manager, Ramona Persaud, on Jan. 1, 2014; Scott Offen and Jim Morrow have run Fidelity Equity Dividend Income and Fidelity Equity-Income, respectively, since 2011. Time will tell whether they stay dividend-focused and add value compared with passive dividend-focused options.

So far, evidence shows it will be a tall order. Few active dividend-growth funds have been able to consistently beat the Nasdaq US Dividend Achievers Select Index on an absolute and risk-adjusted basis. There are funds and managers out there that can, but, as with other types of investments, it pays to have high standards for manager experience, discretion, execution, and expenses.

{kind=link}

{kind=link}