ETF Flows Break Records in 2012

ETFs now make up 13% of total ETF and open-end fund assets.

ETFs now make up 13% of total ETF and open-end fund assets.

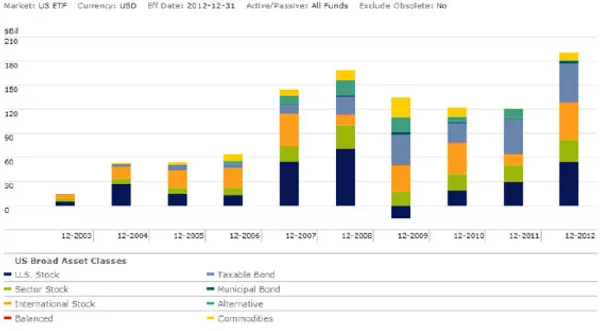

Exchange-traded fund flows reached a record $191 billion in 2012, surpassing the $169 billion flow in 2008. Unlike that year, which was dominated by strong flows into U.S. stock ETFs, 2012 saw record flows into international, fixed-income, and sector stock ETFs. Flows were pushed past the record by a strong showing of $37.7 billion in flows for the month of December.

Strong flows and market appreciation allowed total assets in U.S. ETFs to hit $1.35 trillion. ETFs now account for 13% of total ETF and mutual fund assets, excluding money market funds. ETF assets have more than doubled since the end of 2008, in part due to particularly strong flows into fixed-income ETFs. Taxable bond ETF assets hit $225 billion up from $53 billion four years ago.

After two years of trailing Vanguard, iShares took back the fund flows crown with nearly $61 billion in 2012 flows. Vanguard, which offers a series of low-priced, portfolio building-block ETFs has consistently gained market share, from 7% five years ago to 18% today. Meanwhile, iShares has seen its market share drop from 53% five years ago to 41% today. In response, the firm launched a new strategy in October that centers on a "core" series of low-priced, portfolio building-block ETFs. The launch was accompanied by an aggressive global marketing campaign. In absolute numbers, the 10 "core" ETFs represent less than 4% of iShares' lineup of 280 U.S. funds. However, after the October announcement, these 10 ETFs have accounted for more than 25% of the firm's total net inflows.

SPDR S&P 500 ETF (SPY) brought in more new cash than any other ETF, with $20 billion in flows, most of which came in December. Due its hyper-liquidity and the ability to trade SPY at low costs, traders tend to use it to rapidly place market bets, so flows into SPY are a good barometer of market sentiment.

PIMCO Total Return ETF (BOND) was the most successful new launch of the year, gathering just shy of $4 billion in flows. It is closely watched by the industry because it is the largest active ETF and has an expense ratio that undercuts the cheapest retail share class of the PIMCO Total Return (PTTRX) mutual fund.

| | ETFInvestor Newsletter | |

| Want to hear more from our ETF strategists? Subscribe to Morningstar ETFInvestor to find out what they're buying—and selling—in their portfolios. | One-Year Digital Subscription 12 Issues | $189 Premium Members: $179 Easy Checkout |