5 Undervalued Semiconductor Stocks

Chip stocks are on the rise after a disappointing 2022, but these names still look cheap.

/s3.amazonaws.com/arc-authors/morningstar/b6df6e65-17f1-42fc-b7b8-eb07615d9eef.jpg)

Semiconductor stocks have been flying high lately, fueled by optimism about demand for chips from the artificial intelligence boom.

However, with semiconductor stocks having gotten clobbered in 2022 amid lingering supply chain constraints, geopolitical sales restrictions, and rising interest rates, for long-term investors interested in adding semiconductor stocks to their portfolio, these headwinds still have stocks of several high-quality companies trading at discount-level prices.

As of May 30, 2023, the Morningstar US Semiconductor Index, which measures the performance of companies operating in the semiconductors industry, is up 32.7% for the trailing 12-month period. The broader market is up only 2.1% for the same period, as measured by the Morningstar US Market Index.

However, those gains in semiconductor stocks over the past year have come with a white-knuckle ride.

In 2022, the pandemic-fueled boom in demand for home electronics and personal computers—destinations for semiconductor chips—dwindled, leaving an oversupply of chips in its place. Then, fears of a recession led companies to reduce their spending on high-tech semiconductor products. On top of that, in late 2022, the U.S. Department of Commerce’s restrictions on the sale of semiconductors and equipment to China led to another slump for semiconductor stocks.

All this contributed to a loss of 37.7% for the Morningstar US Semiconductor Index in 2022, compared with a 19.4% drop in the US Market Index.

But it’s been a very different story in recent months, thanks in large part to AI. During the month of May alone, the US Semiconductor Index saw a 21.6% jump, and for the year to date through the end of May, the index is up 61.1%.

Morningstar Semiconductor Index

By far and away the biggest gainer has been Nvidia NVDA, which has seen its stock price rocket 160% this year. Nvidia stock had already rallied substantially ahead of first-quarter earnings on May 24, when the company’s reported results topped expectations and provided an outlook for growth that surpassed Wall Street’s expectations. During May, Nvidia stock rose 36%.

Other semiconductor stocks with big 2023 gains: Broadcom AVGO, up 46%, Marvell Technology MRVL, up 58%, and Advanced Micro Devices AMD, up 83%.

However, Nvidia and Broadcom are now trading at overvalued prices based on their Morningstar fair value estimate, and Marvell and AMD are fairly valued. (Find Morningstar’s take on Nvidia after its earnings report and big rally here.)

What Is a Semiconductor Stock?

Semiconductor companies design, manufacture, and market microchips and microprocessors. Big names in the space include Nvidia and Texas Instruments TXN.

Semiconductor Stocks to Buy Now

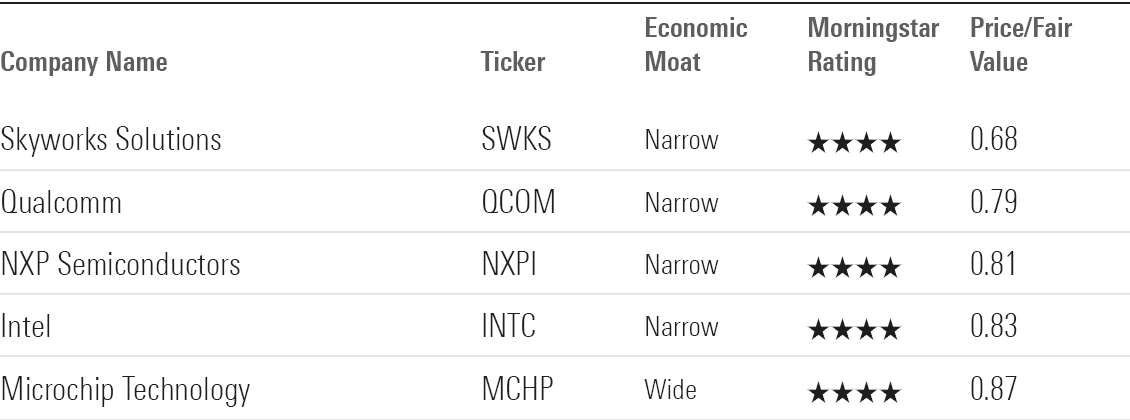

To look for undervalued stocks in the semiconductor industry, we screened the Morningstar US Semiconductor Index for names that carried a Morningstar Rating of 4 or 5 stars, which is determined by a stock’s current price, Morningstar’s estimate of the stock’s fair value, and the uncertainty rating of the fair value.

We also screened for companies that carried a Morningstar Economic Moat Rating of narrow or wide; the rating measures the degree to which the company has a durable competitive advantage. Historically, undervalued stocks with economic moats have performed better over time than less-profitable and more highly indebted counterparts. They also tend to protect against downturns and be less risky than lower-quality stocks.

These were the five most undervalued semiconductor stocks in the Morningstar US Semiconductor Index with wide or narrow moats as of May 30, 2023.

The most undervalued company on the list is Skyworks Solutions, trading at a 32% discount to the fair value estimate set by Morningstar analysts. The least undervalued on the list is Microchip Technology, trading at a 13% discount.

Semiconductor Stocks

Qualcomm

- Fair Value Estimate $140

- Stock Price $110.35

“Qualcomm is first and foremost the steward of patents associated with wireless communications technologies, originally in third-generation, or 3G, CDMA networks and, later, in 4G LTE and 5G networks commonplace today. Qualcomm’s treasure trove of patents in 3G, 4G, and 5G allows the firm to charge device-makers a royalty fee as a percentage of the price of each device sold. We view Qualcomm at the forefront in 5G network proliferation.

“In addition to licensing its IP portfolio, the firm designs chips used predominantly in smartphones and has historically held a competitive edge in baseband chips, which are critical to devices’ inherent ubiquitous connectivity. Qualcomm’s high-end Snapdragon application processors, which often integrate baseband chip functionality, are commonplace in high-end Android smartphones, though OEMs like Samsung have sought to replicate Apple’s strategy of developing in-house chips. Despite these threats, Qualcomm has retained technological superiority over many rivals, and we think there’s a good chance this will continue in the decade ahead, especially as more and more phones rely on advanced 5G connectivity.

“Outside of smartphone processors and baseband chips, Qualcomm has also gained traction in [radio frequency] front-end modules. The company is also pivoting into non-smartphone areas such as automotive and IoT, where we foresee a higher need for advanced processing power in these devices in the years ahead.”

—Brian Colello, director of technology equity research

Intel

- Fair Value Estimate $35

- Stock Price $29.00

“Intel remains the market share leader in the integrated design and manufacturing of microprocessors found in PCs and servers. Historically, the firm supplied the most powerful CPUs, though it has had several manufacturing missteps in recent years that has caused the company to lose market share. We think the company will eventually catch up with its rival Taiwan Semi (TSMC) for advanced manufacturing, but the turnaround will take some more time and we anticipate further share loss and downbeat financial results out of Intel for the next year or two.”

“As cloud computing continues to garner significant investment, Intel’s data center group has been an indirect beneficiary. Mobile devices are the preferred device to perform computing tasks and access data via cloud infrastructures that require large-scale server buildouts. This development has provided strong tailwinds for Intel’s lucrative server processor business over the past decade. However, given manufacturing issues, we believe Intel will lose market share in the data center in the coming years due to intense competition from AMD and customers designing their own ARM-based CPUs.”

—Brian Colello, director of technology equity research

NXP Semiconductors

- Fair Value Estimate $225

- Stock Price $181.18

“NXP Semiconductors is one of the largest suppliers of semiconductors for the automotive market and a significant force in the analog and mixed signal chip markets generally. We believe the firm has a durable position in the automotive, industrial, mobile, and communications infrastructure markets due to a combination of switching costs and intangible assets. Although the company sells into cyclical industries, the strength of these competitive advantages gives us confidence that the firm will generate excess returns over the cost of capital over the next decade.”

“The merger of Freescale and the former NXP in 2015 has led to a powerhouse in automotive semiconductors, which makes up about 50% of NXP’s total revenue. Like many of its chipmaking peers, NXP is well positioned to benefit from safer, greener, smarter cars in the years ahead. NXP is among the market leaders in automotive semis, especially in microcontrollers, that serve as the brains of a variety of electronic functions in a car. We’re optimistic about NXP’s development of products used in active safety systems, such as 77-gigahertz radar modules and battery management systems in upcoming electric vehicles, most notably from Volkswagen VLKAF.”

—Brian Colello, director of technology equity research

Microchip Technology

- Fair Value Estimate $90

- Stock Price $78.32

“Microchip Technology is a leading supplier of microcontrollers, or MCUs, which are semiconductors that act as the brains in a wide variety of common electronic devices, from garage door openers to electric shavers to home appliances like dishwashers and all types of products in between. We view Microchip as one of the best-run firms within the chip space and like the firm’s ability to generate free cash flow under virtually any economic scenario.”

“The businesses of MCUs and analog chips have many desirable features. Neither type of chip is overly dependent on leading-edge designs, so capital investments tend to be relatively low. These chips are selected based on performance rather than price, because they make up only a tiny portion of a product’s overall cost. Customers tend to be loyal, and chips have long product lives because switching to a competing MCU could involve redesigning the entire end product. Thus, MCU and analog firms are able to maintain high margins and returns on invested capital.”

—Brian Colello, director of technology equity research

Skyworks Solutions

- Fair Value Estimate $155

- Stock Price $105.05

“Skyworks Solutions is a leading supplier of a variety of radio frequency components to smartphone makers and other electronics manufacturers. Although the company faces an intense competitive landscape, it should succeed in the coming years as the handset industry focuses on 5G devices, which we expect to require higher radio frequency dollar content per phone.”

“Skyworks earns the majority of its revenue from mobile products, mostly from a variety of products that switch, filter, and amplify wireless signals in smartphones. Given the rise of advanced 5G-enabled smartphones, which use a wider variety of wireless spectrum and frequency bands than in prior generations of networks, RF content per phone has grown exponentially in recent years, lifting Skyworks and its RF competitors. 5G rollouts are in the early innings today and 5G-connected devices should be even more complex, making Skyworks’ expertise even more valuable to device makers. Meanwhile, Skyworks is one of the few RF firms with the scale to supply hundreds of millions of RF products per year, giving it a leg up on new entrants.”

—Brian Colello, director of technology equity research

Nvidia NVDA

- Fair Value Estimate $300

- Economic Moat: Wide

- Morningstar Rating: 2 Stars

“Nvidia is the top designer of discrete graphics processing units that enhance the visual experience on computing platforms. The firm’s chips are used in a variety of end markets, including PC gaming and data centers. Traditional GPU uses include professional visualization applications that require realistic rendering, including computer-aided design, video editing, and special effects. Nvidia has experienced success in focusing its GPUs in burgeoning markets such as artificial intelligence (deep learning) and self-driving vehicles. Hyperscale cloud vendors have leveraged GPUs in training neural networks for uses such as image and speech recognition, large language models (ChatGPT), and other forms of generative AI.”

—Brian Colello, director of technology equity research

“We are raising our fair value estimate to $300 per share from $200 per share, as we raise our forecast for Nvidia’s data center segment revenue to grow at a 30% [compound annual growth rate] over the next five years (up from 19% previously).

“The uplift is primarily driven by unsatiated demand for Nvidia’s latest H100 data center GPU. Relative to its predecessor, the H100 is 9 times faster in artificial intelligence training and up to 30 times faster in AI inferencing for transformer-based large language models such as Open AI’s ChatGPT (generative pretrained transformer). We believe AI models such as ChatGPT use thousands of GPUs to be trained, with competition between Microsoft, Google, and others supporting our updated growth projections.”

—Abhinav Davuluri, strategist

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IORW4DN3VVC3BC4JO7AQLSJTF4.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ODMSEUCKZ5AU7M6BKB5BUC6G5M.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TGMJAWO4WRCEBNXQC6RFO5TOAY.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/b6df6e65-17f1-42fc-b7b8-eb07615d9eef.jpg)