What Apple’s Cash ‘Problem’ Means for its Stock Investors

Another $90 billion stock buyback in place as Apple continues its push to be net-cash neutral.

/s3.amazonaws.com/arc-authors/morningstar/ed88495a-f0ba-4a6a-9a05-52796711ffb1.jpg)

Apple AAPL has a problem that most of us would love: It has too much cash.

Not only is the iPhone maker the world’s largest company, it’s also the world’s biggest cash machine, pumping out more than any of its mega-cap technology peers or any other company for that matter.

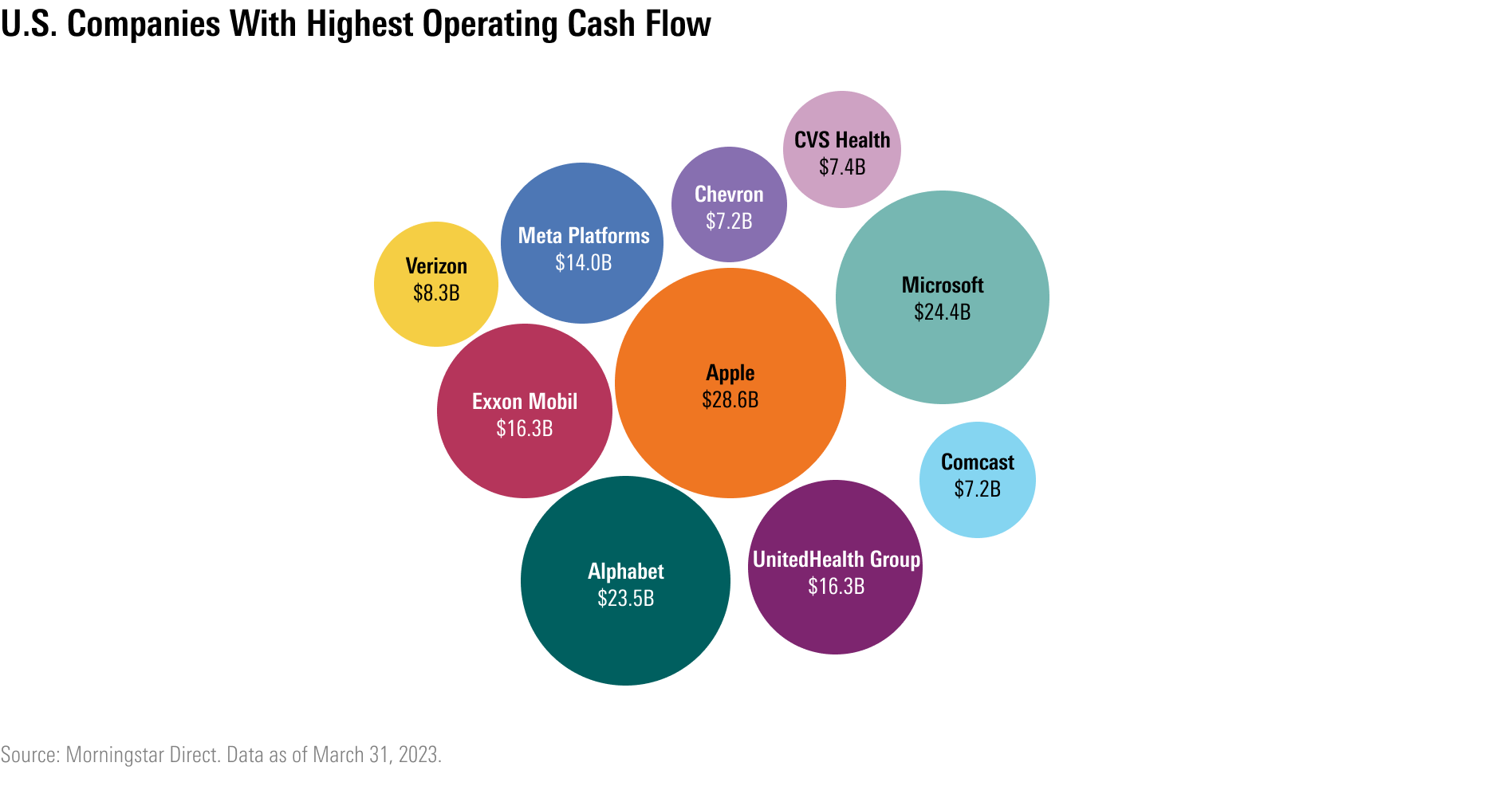

Operating cash flow totaled $28.6 billion in the latest fiscal second quarter compared with $24.4 billion at Microsoft MSFT, $23.5 billion at Alphabet GOOGL, and $13.9 billion at Meta Platforms META.

That leaves Apple with an unusual problem. What to do with all that cash?

On the one hand, it’s good to be cash-rich because it gives a company plenty of flexibility to manage its businesses in the best of times by investing in innovation and staying competitive. In uncertain economic times, a large cash stash creates what is sometimes known as a “fortress balance sheet,” which allows a company the stability to keep businesses running smoothly and returns to shareholders steady. For investors, this has been an important element of Apple stock’s appeal.

On the other hand, having an ever-growing pile of cash on a company’s balance sheet, just collecting interest, is often seen by investors as an inefficient use of capital.

In 2018, Apple set an ambitious goal to reach a “net-cash neutral” position, in which any excess cash is balanced by its total debt. While whittling down its cash hoard through stock buybacks and dividends payouts presents a windfall for owners of Apple stock along the way, it could mean an eventual paring back of buybacks.

How the Cash Hoard Benefits Apple Stock Holders

For now, however, Apple’s businesses are gushing cash.

At quarter’s end, Apple had a stash of $166 billion of cash on its balance sheet. After accounting for about $110 billion in debt, net cash totaled $57 billion.

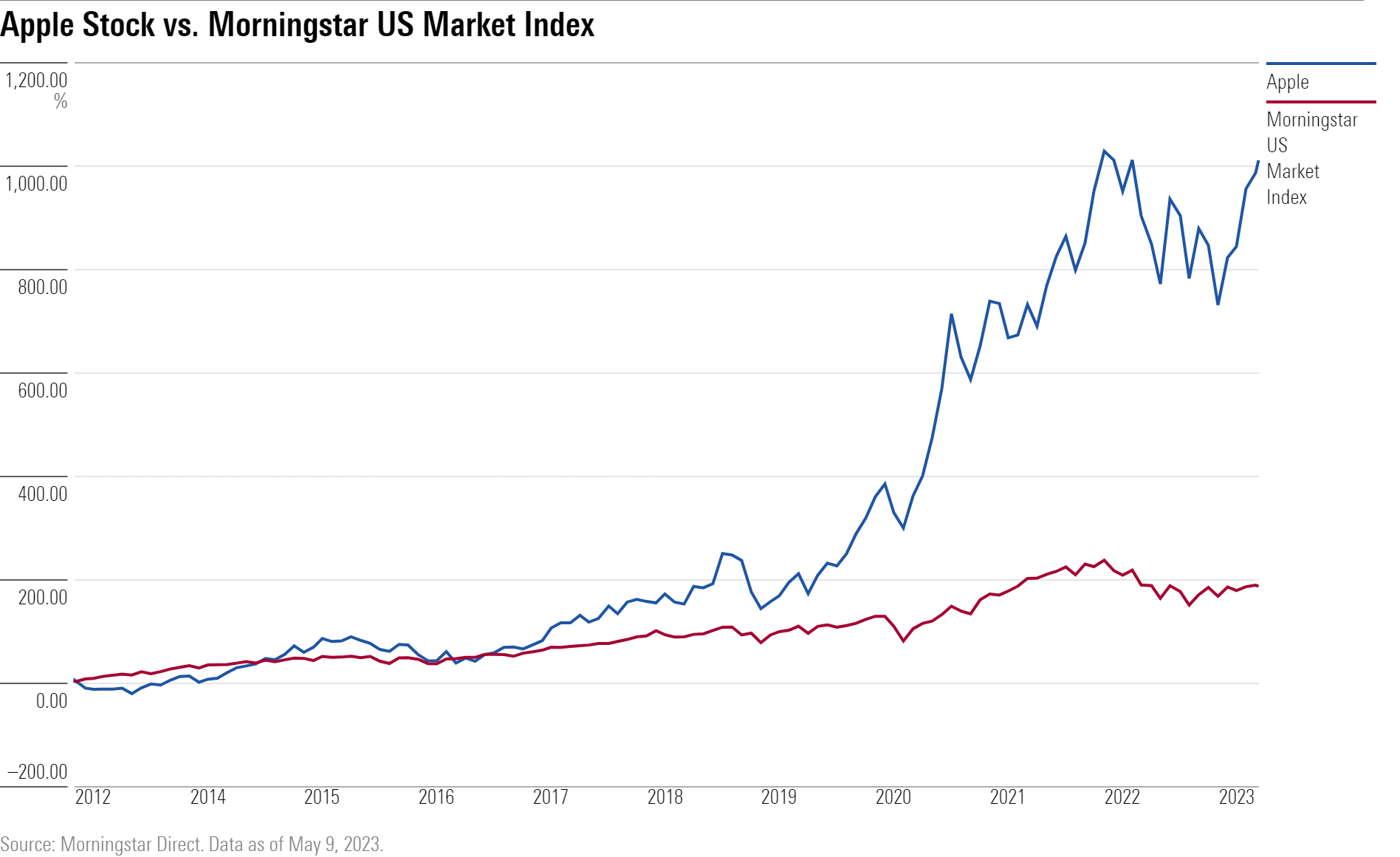

Owners of Apple stock have been the biggest beneficiaries of its happy cash conundrum. The company has returned nearly $732 billion to its investors through share buybacks and dividends since the start of 2013. In that time frame its stock price has soared 952.5%, compared with 180.4% for the Morningstar US Market Index.

During the latest fiscal second quarter, Apple spent $19.1 billion buying back 129 million of its shares and paid out $3.7 billion in dividends to investors.

It authorized an additional $90 billion share repurchase program, matching the level of the program it approved last year. The company also boosted its quarterly dividend by 4% to $0.24 per share from the previous $0.23 and said it planned annual increases to the dividend in the future.

In making the move, Apple chief financial officer Luca Maestri noted the “continued confidence we have in our business now and into the future.” Yet, he also restated the company’s goal of becoming “net-cash neutral.”

The company introduced its net-cash neutral goal in 2018 when it began to repatriate the cash it had long stockpiled overseas following tax reforms pushed through under former President Donald Trump at the end of 2017 in the Tax Cuts and Jobs Act.

Apple Stock Dividend ‘Lackluster’

Indeed, the bulk of Apple’s capital returns to shareholders, $635.7 billion, has come since the tax change, which was designed to encourage companies to bring back money parked overseas and reinvest it in the U.S. Before the tax change, U.S. multinationals often chose to retain earnings at their foreign subsidiaries to defer paying taxes of up to 35% in the U.S. After the tax change, companies were subject to a one-time tax rate of 15.5% on repatriated cash, and 8% on any noncash or illiquid assets.

Since 2018, the company’s net cash position has shrunk by more than half from $123 billion.

While the company will eventually reach a net-cash neutral state, this could take years because of how much cash it generates, says Abhinav Davuluri, Morningstar equity and credit strategist. As Apple approaches its goal of cash neutrality, investors should expect the magnitude of share buybacks to diminish.

Of course, Apple could solve its excess cash problem in one fell swoop by making a big acquisition. But that would be out of character for the company, says Davuluri.

“Apple does not historically use their cash to buy other companies,” says Davuluri. “If they do, they are small acquisitions. Apple would rather build themselves than buy.”

He notes that Apple already heavily invests in research and development, has been ramping up its spending, and yet still has boatloads of excess cash.

“They have been increasing R&D pretty significantly, both absolutely and as a percentage of sales, from $8 billion in 2015, or 3.55 of sales to $26 billion in 2022, or 7% of sales,” says Davuluri.

With a yield of 0.56%, Apple’s dividend is “lackluster,” he says, though overall he considers the company’s capital allocation strategy “exemplary.”

Davuluri considers Apple overvalued. At its recent price of $172.82 per share, Apple stock trades at a 15% premium to his fair value estimate of $150.

Apple Stock at a Glance

- Morningstar Fair Value Estimate: $150 per share

- Morningstar Rating: 3 stars

- Morningstar Uncertainty Rating: High

- Morningstar Economic Moat Rating: Wide

The author or authors own shares in one or more securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MNPB4CP64NCNLA3MTELE3ISLRY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/F2S5UYTO5JG4FOO3S7LPAAIGO4.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/7TFN7NDQ5ZHI3PCISRCSC75K5U.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed88495a-f0ba-4a6a-9a05-52796711ffb1.jpg)