Going Into Earnings, Is Disney Stock a Buy?

The prospects for Disney’s direct-to-consumer business and ESPN will be in the spotlight.

/s3.amazonaws.com/arc-authors/morningstar/fab4d3e1-7951-4575-a38d-fd2028ad4ae3.jpg)

Disney DIS is scheduled to release its first-quarter earnings report on May 10, 2023, after the close of trading. Here’s Morningstar’s take on what to watch for in earnings and Disney’s stock.

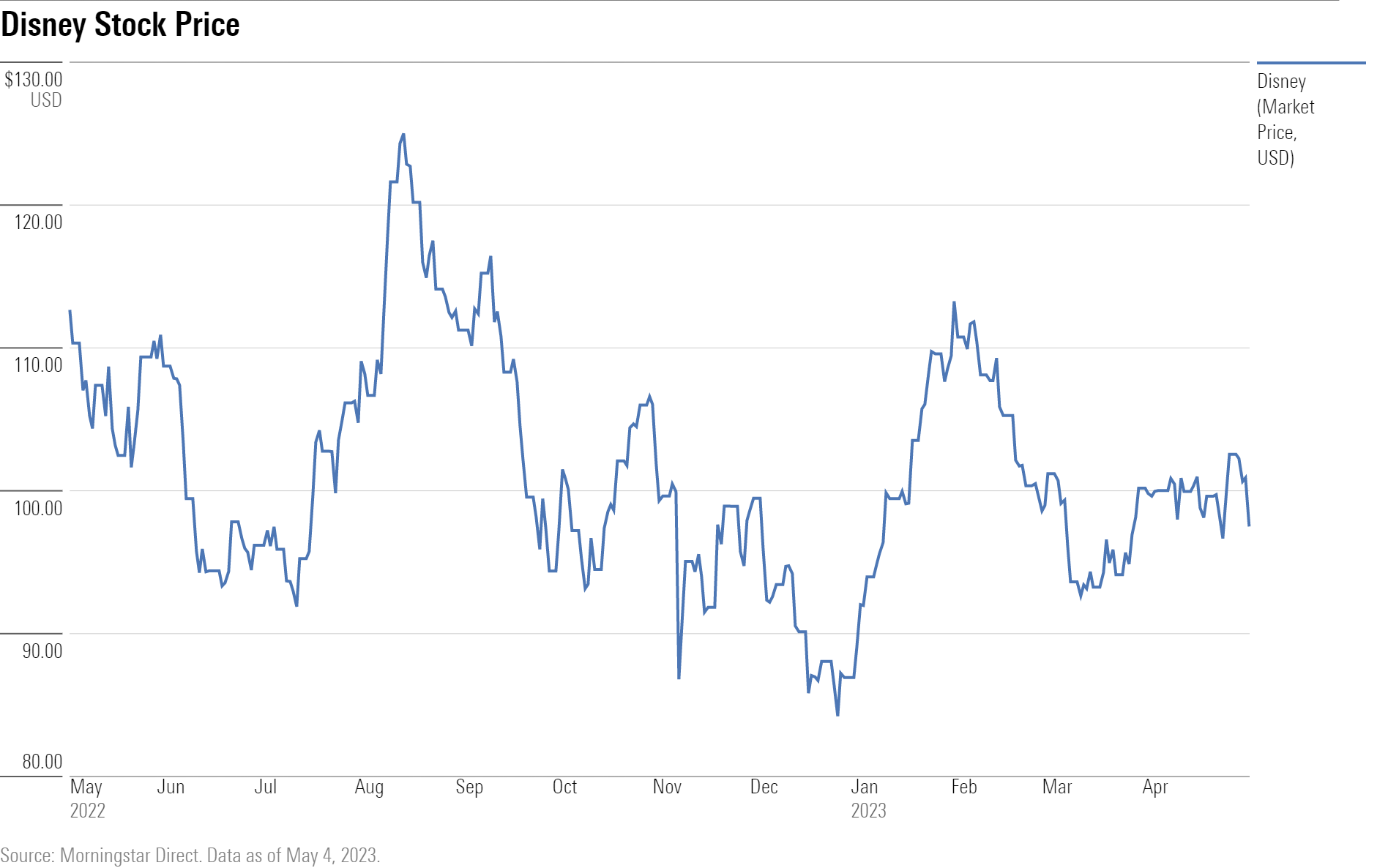

Disney Stock at a Glance

- Fair Value Estimate: $155

- Morningstar Rating: 4 stars

- Morningstar Uncertainty Rating: High

- Morningstar Economic Moat Rating: Wide

What to Watch for in Disney’s Quarterly Earnings

- For Disney’s direct-to-consumer businesses, what was the operating loss? Is it down sequentially and/or year to year? Is the direct-to-consumer business on a path to a breakeven quarter in fiscal year 2024?

- For the new ESPN reporting segment, what data will the company provide, and what will the company say about the future of ESPN?

- We are looking for any discussion about the chief executive succession plan. Is any progress toward finding that person, or will Robert Iger stay on as CEO?

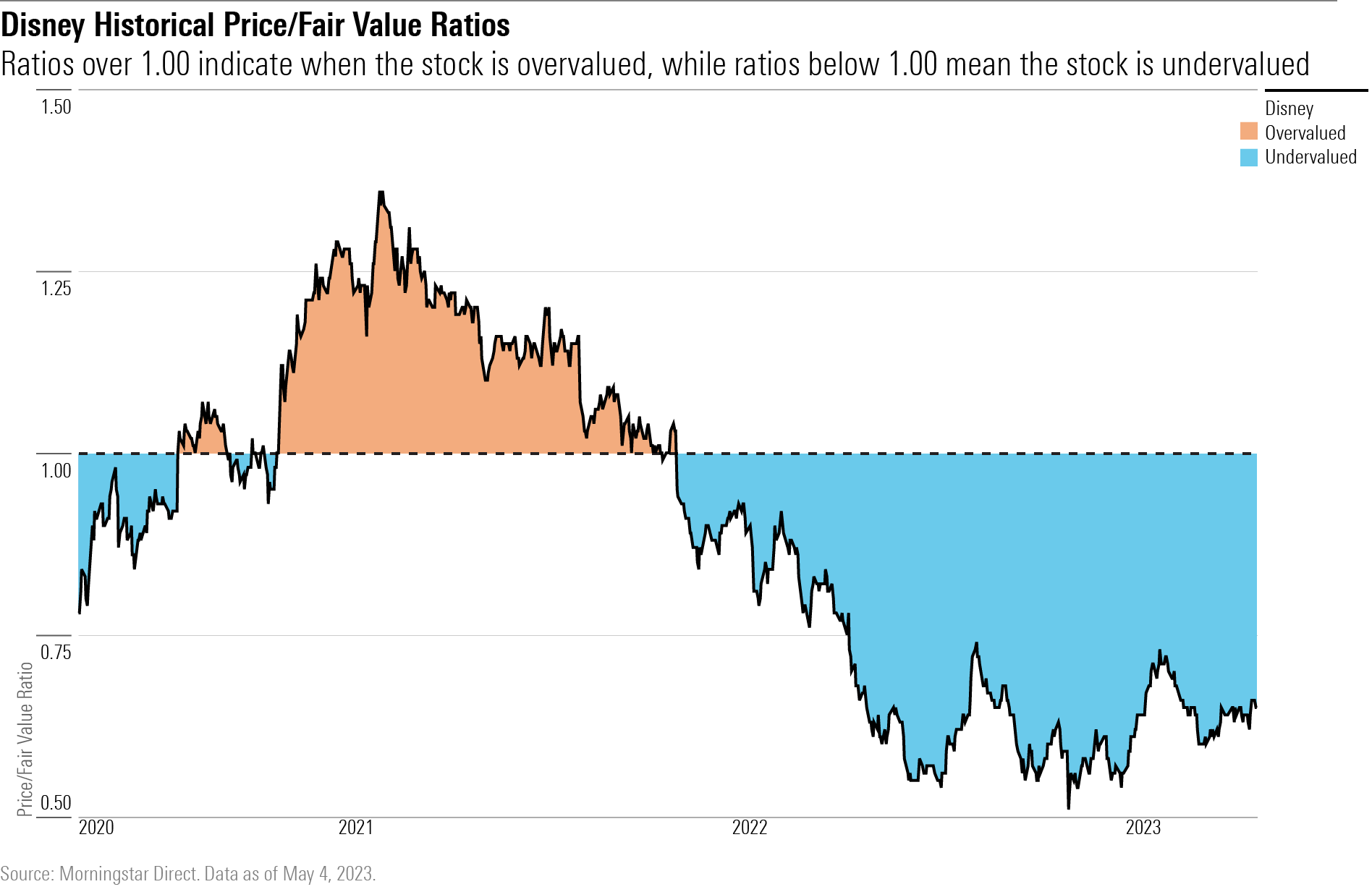

Fair Value Estimate for Disney

At a 4-star rating, we believe Disney stock is undervalued when compared with our fair value estimate.

Our updated $155 fair value estimate for Disney reflects the realigned segments and lower losses from streaming. We expect average annual top-line growth of 7% through fiscal 2027. We project average annual sales growth from the linear television networks to be just under 1% from fiscal 2023-27 (2% for affiliate fees and negative 1.5% for advertising) as our projections for U.S. pay-TV penetration assumes an ongoing decline. We project that certain international theme parks will remain capacity constrained or closed into 2023. Following a strong bounceback of 73% in 2022, respectively, we expect more normalized growth of 4% for the parks and consumer segment over the next five years. For fiscal 2023-26, we forecast the content segment will approach fiscal 2019 revenue but fall short as the overall theatrical business remains on a gradual decline. We estimate 18% average annual growth for the direct-to-consumer segment as we are modeling strong subscriber growth for Disney+ and Hulu along with further price increases. We project Disney’s overall operating margin will improve to 21% in fiscal 2027 from 8% in fiscal 2022 as the losses at the direct-to-consumer segment turn to gains and ongoing margin improvements at the theme parks.

Read more about Disney’s fair value estimate.

Economic Moat Rating

We assign Walt Disney a wide economic moat rating. Its media networks segment and collection of Disney-branded businesses have demonstrated strong pricing power in the past decade. The Disney networks remain important pieces in the traditional pay-TV bundle. The firm’s roster of networks provides distributors with not only general entertainment but also live sports at ESPN and news coverage at ABC, two genres that are keeping many subscribers in the pay-TV universe. The media network component also includes the Disney Channel, one of two dominant cable networks for children, which allows Disney to introduce and extend its strong content portfolio. Disney’s studio capabilities have been strengthened via the Fox acquisition, particularly on the television production side. The continued strength at the studios and media networks should help to drive continued success for the firm’s direct-to-consumer ambitions at Disney+, Hulu, and ESPN+. Disney has mastered the process of monetizing its world-renowned characters and franchises across multiple platforms. The company has moved beyond the historical view of a brand that children recognize and parents trust by acquiring and creating new franchises and intellectual property. Disney uses the success of its filmed entertainment not only to drive Disney+ subscriptions, but also to create new experiences at its parks and resorts, merchandising, TV programming, and even Broadway shows.

Read more about Disney’s moat rating.

Risk and Uncertainty

On the basis of competitive linear and streaming media markets that Disney operates in, along with the level of advertising and parks revenue that is exposed to the economy and economic cycles, we believe a High Morningstar Uncertainty Rating is currently more appropriate than Medium to better reflect the volatility we expect Disney investors will face relative to our global coverage. Disney’s results could suffer if the company cannot adapt to the changing media landscape. The company’s ad-supported broadcast networks, along with the theme parks and consumer products, will suffer if the economy weakens. Disney’s labor relations remain one of the company’s largest environmental, social, and governance risks. Disney and its subsidiaries have been subject to a number of lawsuits alleging racial and gender discrimination, sexual assault/harassment, and wage gap/discrimination.

Read more about Disney’s risk and uncertainty.

DIS Bulls Say

- The parks and resorts segment will rebound strongly from the pandemic as families still view the parks as a prime vacation destination.

- Disney+ has a long runway for growth available in both the United States and internationally. The firm’s original series and the deep and constantly expanding library will drive the growth.

- Although making movies is a hit-or-miss business, Disney’s popular franchises and characters reduce this volatility over time. Additionally, the firm’s annual slate does not generally rely one big picture, reducing the downside from a flop.

DIS Bears Say

- The business model for the media networks division depends on the continued growth of affiliate fees. Any slowdown in the growth of these fees, as pay-television subscribers continue to decline, could tremendously hit profitability.

- The streaming space is becoming increasingly crowded. Disney may need to continue to fund losses at this segment beyond fiscal 2024.

- Developing mass-market hit programs can be unpredictable, especially as media fragmentation continues. The race to attract and retain talented creatives has been and will remain very competitive and expensive.

This article was compiled by Maggie Guidici.

Get access to full Morningstar stock analyst reports, along with data and tools to manage your portfolio through Morningstar Investor. Learn more and start a seven-day free trial today.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WC6XJYN7KNGWJIOWVJWDVLDZPY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HHSXAQ5U2RBI5FNOQTRU44ENHM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/737HCNGRFLOAN3I7RKGB7VPEKQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/fab4d3e1-7951-4575-a38d-fd2028ad4ae3.jpg)