February CPI Report Showed Progress on Inflation Stalled, Fed Rate Hike Path Intact

Despite banking system worries, hot inflation means interest rates will head still higher.

/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)

A year after the Federal Reserve kicked off its aggressive path of interest-rate hikes, the February Consumer Price Index report showed that progress in lowering the rate of inflation has run out of steam.

In particular, the February CPI report showed continued upward pressure on prices paid for services, a segment of the economy closely tied to the jobs market, where hiring also remains strong.

And although much of the focus in recent days has been on worries about the banking sector in the wake of the collapse of Silicon Valley Bank, as long as the Fed’s efforts to contain the crisis are effective, that leaves officials on track to continue raising rates—and holding them at high levels—in order to make further progress in reducing inflation.

“Today’s report shows that progress in bringing inflation down has stalled for now,” says Preston Caldwell, chief U.S. economist at Morningstar. “This ensures the Fed will continue hiking interest rates for at least the next meeting or so, despite emerging signs of distress in the financial system.”

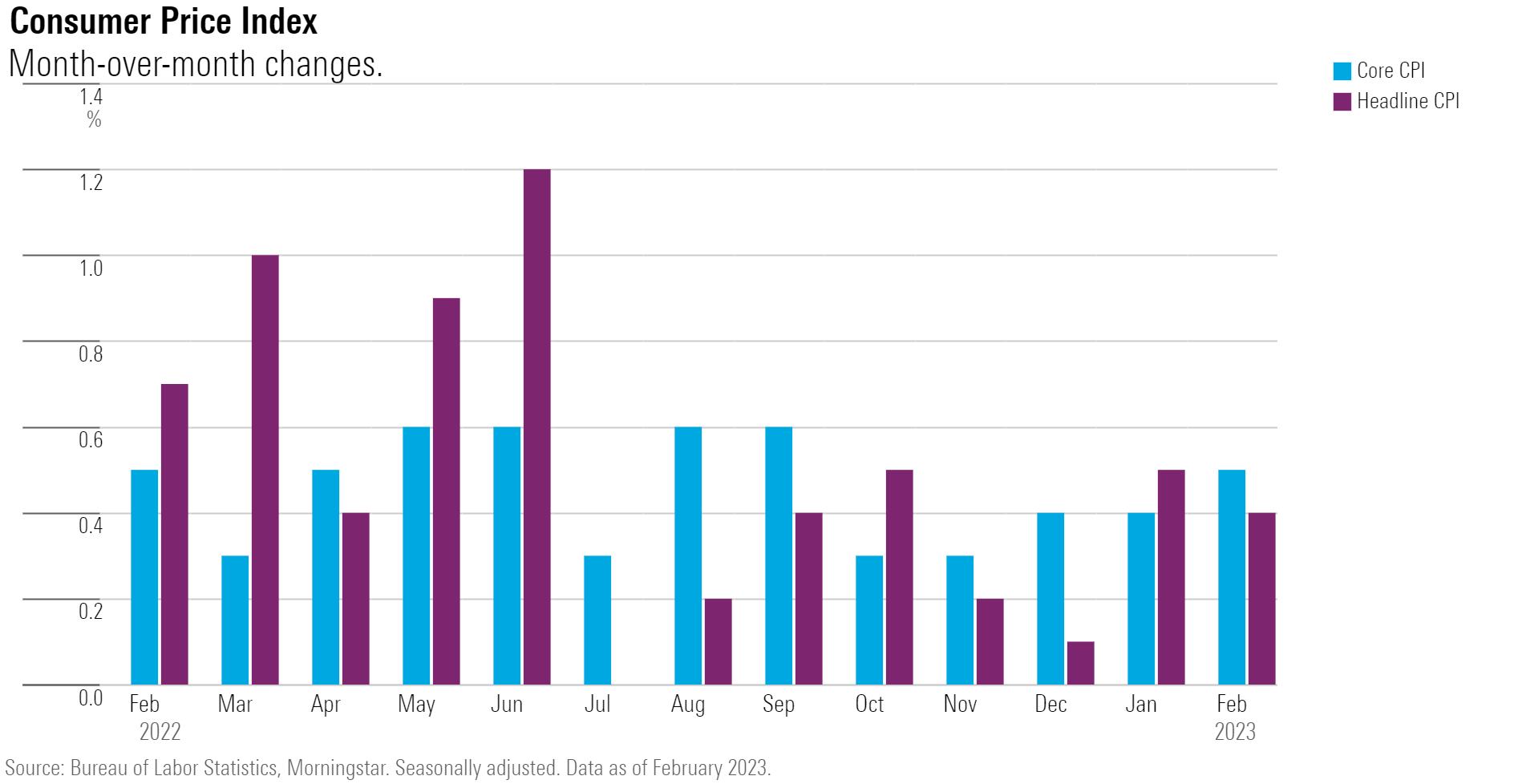

No Big Surprise From the February CPI Report

The Bureau of Labor Statistics reported an overall rise of 0.4% in the CPI for February, in line with consensus estimates, led by shelter prices, which contributed over 70% of the total increase. Rising food prices also contributed, while prices for energy decreased 0.6%.

Core CPI, which excludes the volatile food and energy components, rose 0.5% in February, just above forecasts. Drivers of the increase in core inflation in February included shelter, recreation, and airline fares. Prices for used cars and trucks, as well as medical care, decreased over the month.

February CPI Report Key Stats

- CPI rose 0.4% for the month versus 0.5% in January, in line with expectations.

- Core CPI (excluding food and energy) rose 0.5% for the month after rising 0.4% in January, just above forecasts.

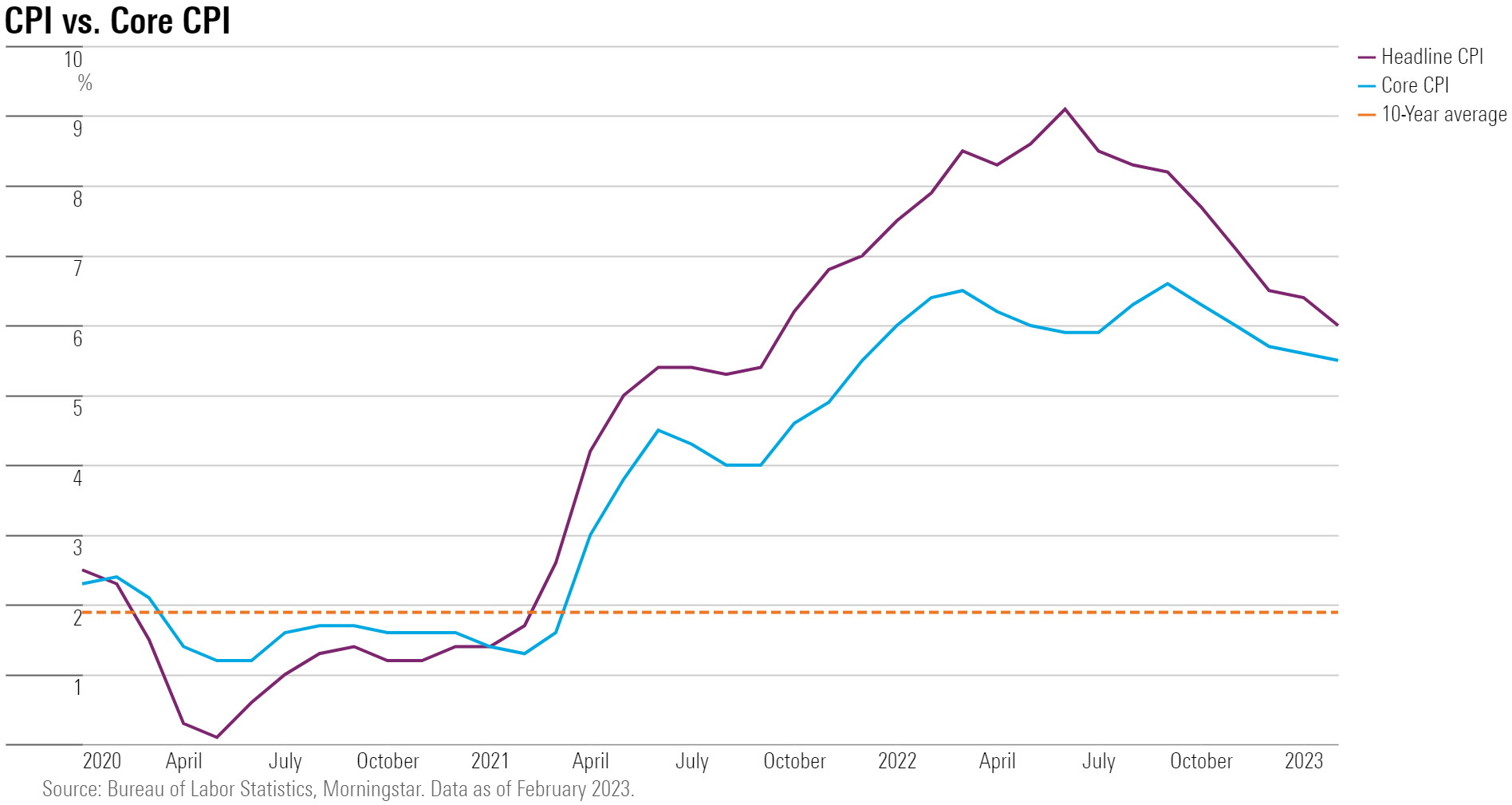

- CPI, year over year, rose 6.0% in line with expectations for the month after rising 6.4% in January.

- Core CPI, year over year, rose 5.5%, matching expectations after rising 5.6% in January.

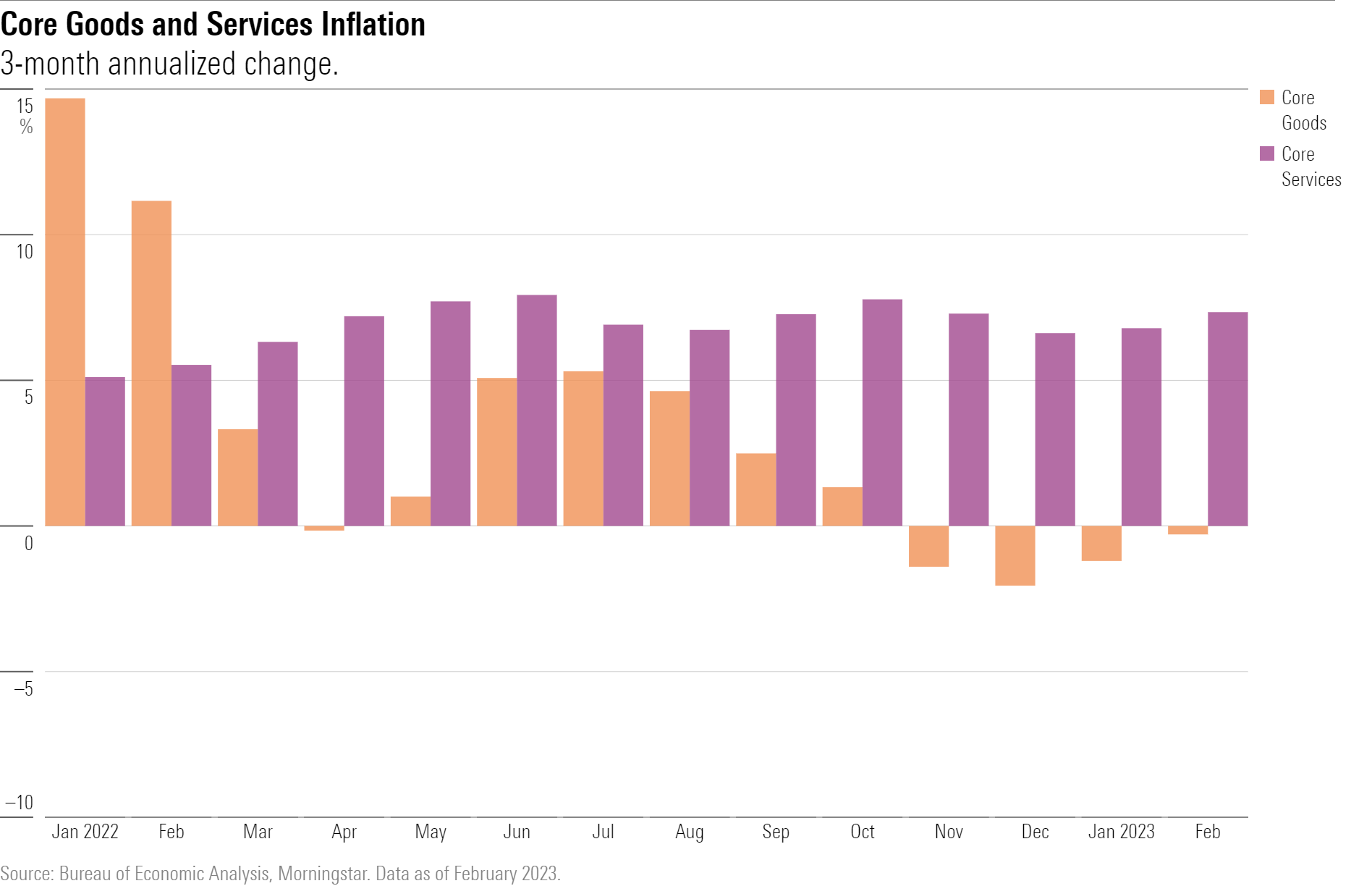

Core inflation has rebounded to a 5.2% average annualized rate in the past three months, compared with a 4.6% rate last month, according to Caldwell. “Most categories of the CPI participated in the uptick,” he says. “However, it’s still the case that core CPI ex shelter looks very much benign, running at a 2.1% annualized rate of inflation.”

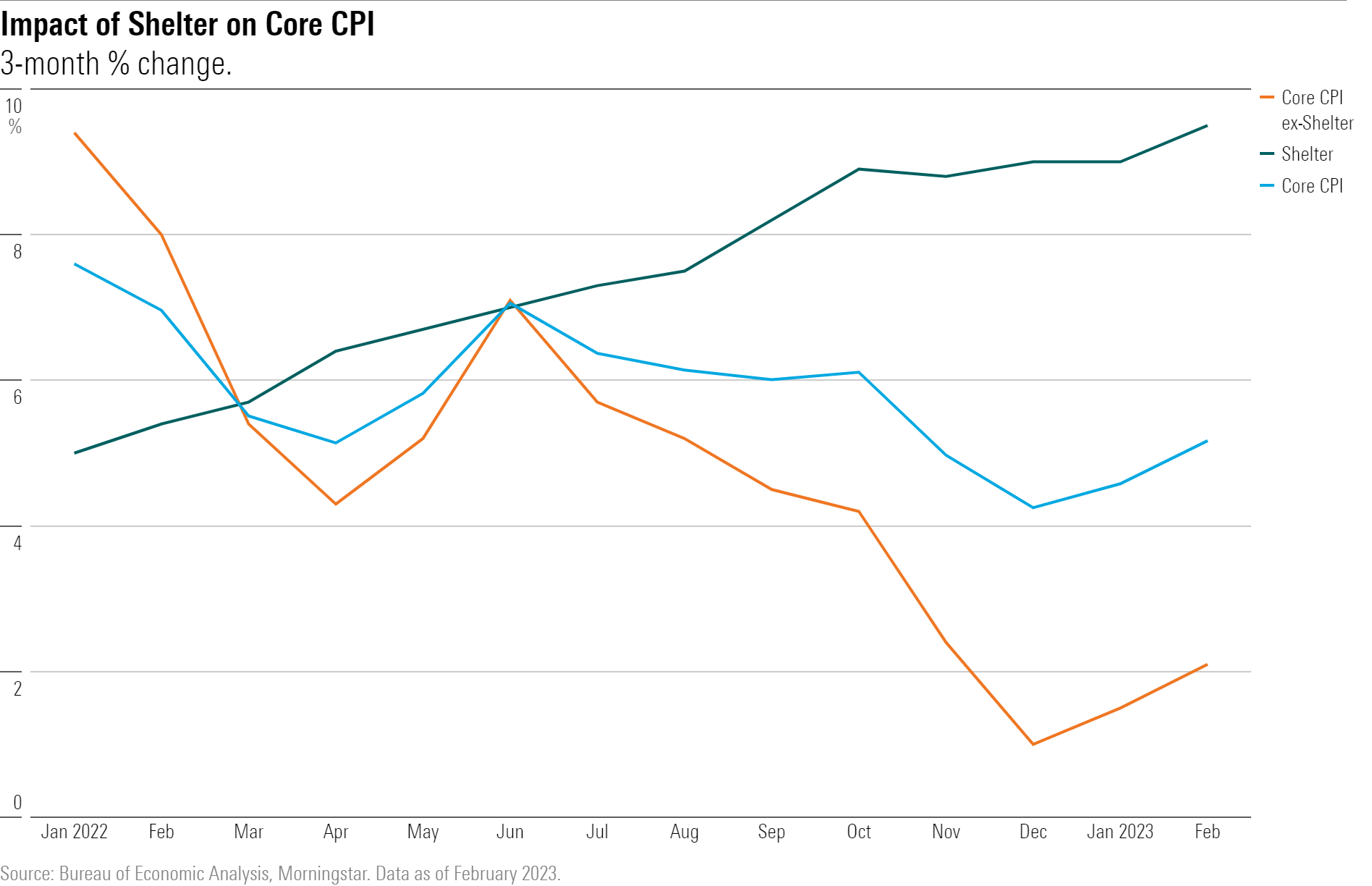

Shelter Costs Still Driving CPI Growth, For Now

“Shelter prices have continued to soar,” Caldwell says, “But the shelter component of the CPI responds with about a 12-18 month lag with respect to conditions of the actual market—where prices are flat or falling.”

Over the past three months, shelter prices have increased at a 9.5% annualized rate, according to Caldwell. Owing to the downturn in housing demand along with expanding supply, he says, home prices have moved down since mid-2022, and rents have been flat in the past several months. “This will eventually lead to a sharp deceleration in the shelter component of the CPI, helping to bring measured inflation back to normal.”

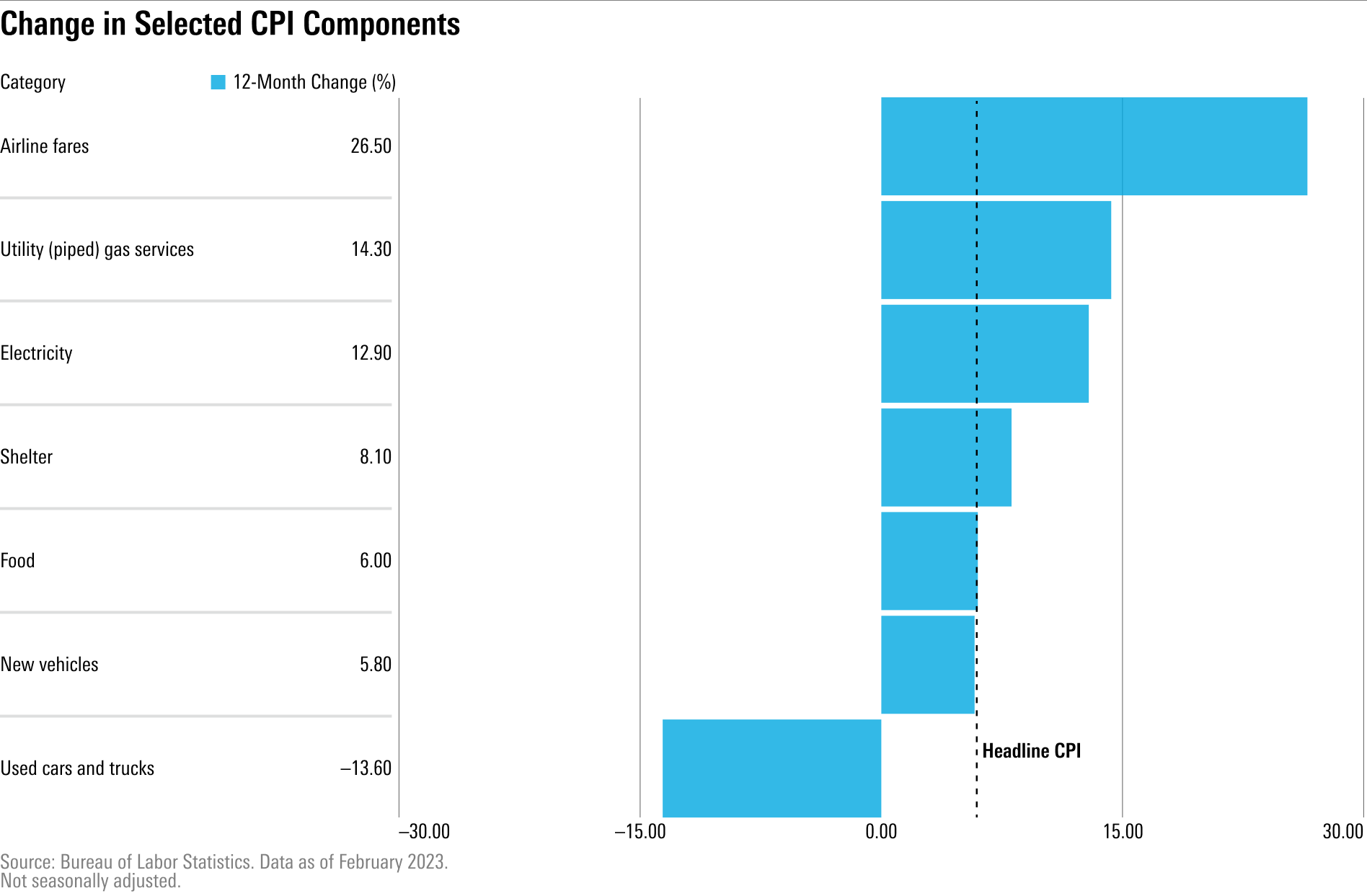

In February, energy prices fell 0.6% over the month as utilities prices fell 8.0% and fuel oil prices fell 7.9%. Gasoline prices rose 1.0%.

In terms of core goods and services, apparel prices rose 0.8% for the month after rising just as much in January. Transportation services prices rose 1.1%.

Prices fell for used cars and trucks, down 2.8% over the month.

Services Inflation Remains Concerning for Now

“The most worrying component of the CPI remains core services excluding shelter and healthcare,” Caldwell says. Core services ex shelter and healthcare inflation has averaged a 6.8% annualized rate in the past three months, according to Caldwell, “and shows no signs of falling.”

The category has been highly sensitive to labor costs historically, Caldwell says, “but the rate of inflation in this category surpasses recent wage growth of 4.6% year-over-year as of February.”

“This suggests that we should see inflation fall soon in this category as well.”

Interest-Rate Hike Expectations Moderate

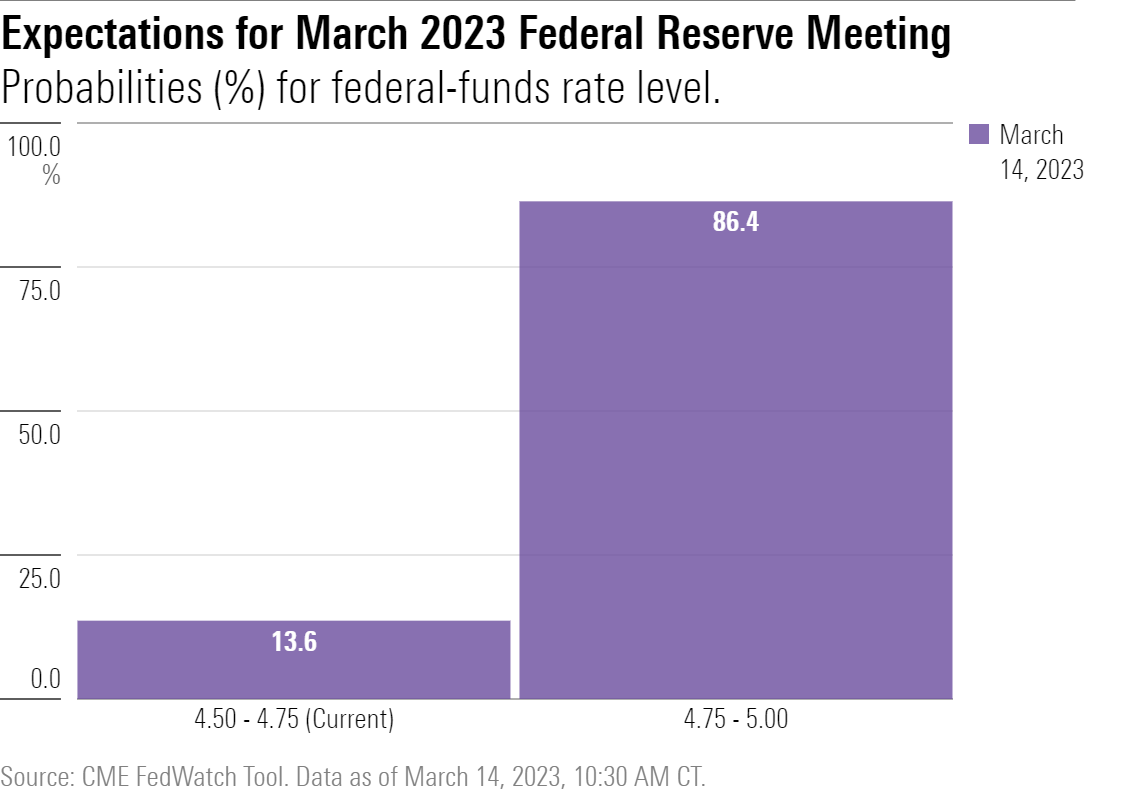

Despite the data showing that inflation remains well above the Fed’s 2% target, expectations for Fed rate hikes have diminished amid concerns about the knock-on effects of the emerging bank crisis.

The majority of market participants now expect the federal-funds effective rate target to rise just 0.25% to a range of 4.75%-5.00% at next week’s Fed meeting on March 22, according to the CME FedWatch Tool. In addition, 13.6% of market participants see the Fed keeping interest rates unchanged at their current target of 4.50%-4.75%.

A week ago, prices suggested that no one in the futures market was expecting the Fed to hold rates unchanged at their March meeting: 30.2% of the participants foresaw a 0.25-point raise, and the remaining 69.8% expected a larger 0.5-point increase. The latest softening in expectations for interest rates comes alongside the bank stock selloff triggered by SVB Financial’s liquidity crunch.

Further out, the majority of market participants now see the Fed pausing its rate hikes in June or July of this year and cutting rates soon after.

But Caldwell thinks the current expectations for a lower path of interest rates will prove unfounded.

After a year of relative quiescence, the financial system is now being rocked by outbursts of distress, including the failure of Silicon Valley Bank. Bond markets crashed in response to these events, with the five-year U.S. Treasury falling about 70 basis points initially. This implies a substantially lower path for the federal-funds rate. However, given the fact that the Fed and other authorities have moved very aggressively to contain the damage from Silicon Valley Bank and other episodes, we see less of a need for a lower path for the federal-funds rate to soothe financial distress. A 50-basis-point rate hike for the March meeting should (and very likely will) be off the table, as the Fed needs to move slow. But bank failures do not inherently mean the economy is about to plunge off into a recession, which would be the only reason for the Fed to abruptly shift course in monetary policy.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/54RIEB5NTVG73FNGCTH6TGQMWU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MNPB4CP64NCNLA3MTELE3ISLRY.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)