What’s The Surest Route to Investing Excellence?

Hint: It’s not about pursuing perfection.

/s3.amazonaws.com/arc-authors/morningstar/550ce300-3ec1-4055-a24a-ba3a0b7abbdf.png)

We don’t seek an “above-average” partner to spend life with. We aren’t pining for our kids to earn straight B’s in school. Nobody dreams of driving a Honda minivan. In these and so many other aspects of life we’re conditioned not to settle for good, but to strive for perfection.

It’s therefore no surprise that many of us apply that same mindset to investing. We seek to find the best-performing stocks or funds; to unerringly time our trades; to optimize our asset mix to our preferences and circumstances.

But whereas the pursuit of excellence in other realms can yield rewards—a fulfilling life and career for instance—in investing it often translates to lots of transactions, higher cost, greater complexity, and, ultimately, disappointment.

Here, I’ll walk through a handful of examples where it pays not to make the perfect the enemy of the good in investing.

Investing Versus Saving

Many of us embark on investing in hopes we’ll score huge gains and coast to a comfortable lifestyle and secure retirement. The reality is that saving, especially in the early years, is far more important to our long-term financial wellness and security than investment performance.

If you don’t tuck enough away and manage to beat the indexes for a few years, that could end up being a Pyrrhic victory—you’ve cleared one hurdle on the more difficult path you’ve chosen, one steeply pitched and strewn with obstacles. A healthy savings rate clears the way, even if it doesn’t earn one bragging rights the way a high-performing investment can.

Choosing Versus Diversifying

It’s only natural to conclude that successful investing is a matter of making a series of good choices. After all, that’s kind of how life works, where prudent decisions about education, family, and career tend to confer long-term benefits.

Investing doesn’t punish prudence—far from it. But it’s different in that the more choices we face ourselves with, the more we can put our plans at risk. Why? Some of the most difficult investment decisions we’ll face come at times of duress or uncertainty, when we might succumb to impulse, panic selling, or buying for fear of missing out.

Diversifying across assets is, by definition, imperfect. We’re forgoing the best return we could theoretically achieve. But we’re also taking a big risk off the table: us. That is, by widely diversifying, we face ourselves with fewer choices about what to buy, what to sell, how much, and when. And with that, we mitigate the risk of making rash choices that lead to poor outcomes.

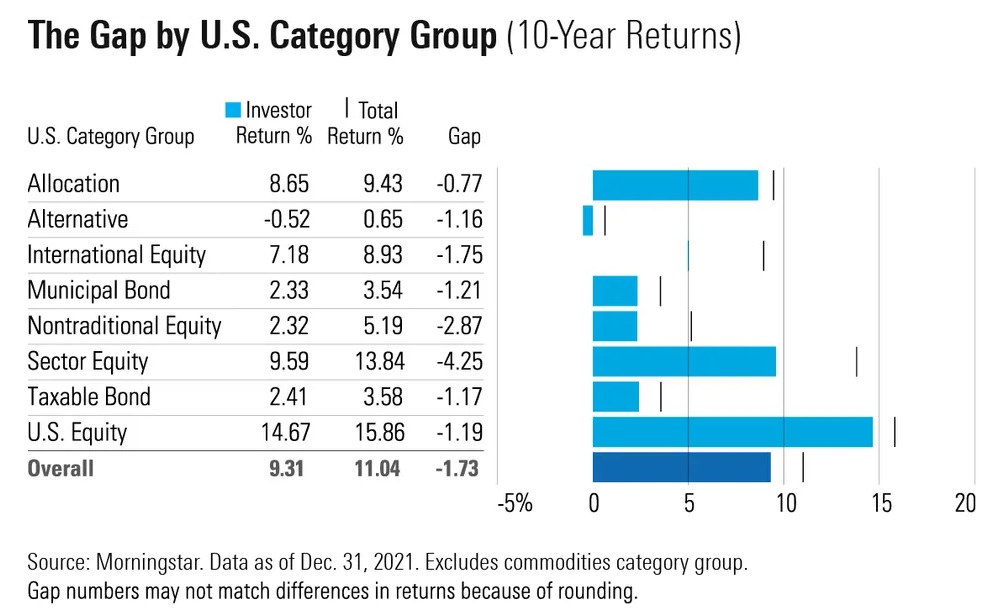

We can find evidence of that in research we’ve done examining the difference between funds’ reported returns and the average returns investors actually earned in those funds, that gap owing to mistimed purchases and sales. What we found is that the gap tended to be narrowest among more widely diversified allocation funds, meaning investors were capturing more of the funds’ returns.

Trading Versus Rebalancing

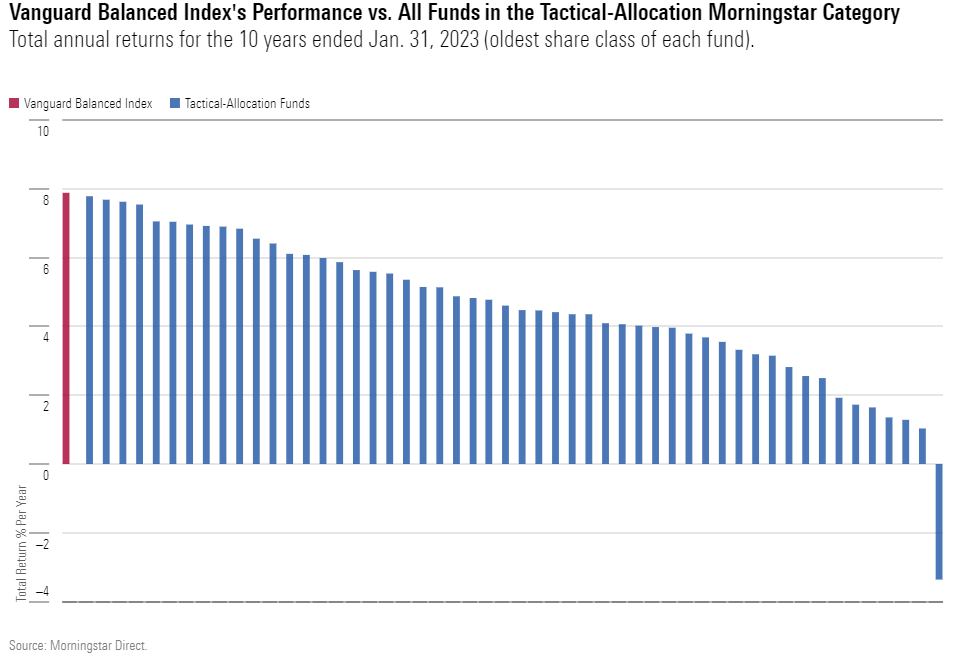

Diversification only gets us part of the way. There’s also the matter of ensuring that our asset allocation fits our risk/reward objectives. In an ideal world, we’d ratchet our asset exposures up and down in anticipating market gyrations, bagging gains and sidestepping losses. The world doesn’t work that way, though, as the dismal record of tactical allocation mutual funds well attests: Not a single tactical fund beat a simple 60% U.S. stocks/40% U.S. bonds portfolio over the trailing 10 years ended Jan. 31, 2023.

Rebalancing isn’t going to shield us from losses or maximize our gains. But by routinizing risk management, it should keep us out of the kind of trouble that could present a real threat to our longer-term financial security—that is, when we make sweeping changes to our asset allocation, permanently locking in losses or forgoing gains in the process.

Alpha Versus Indexing

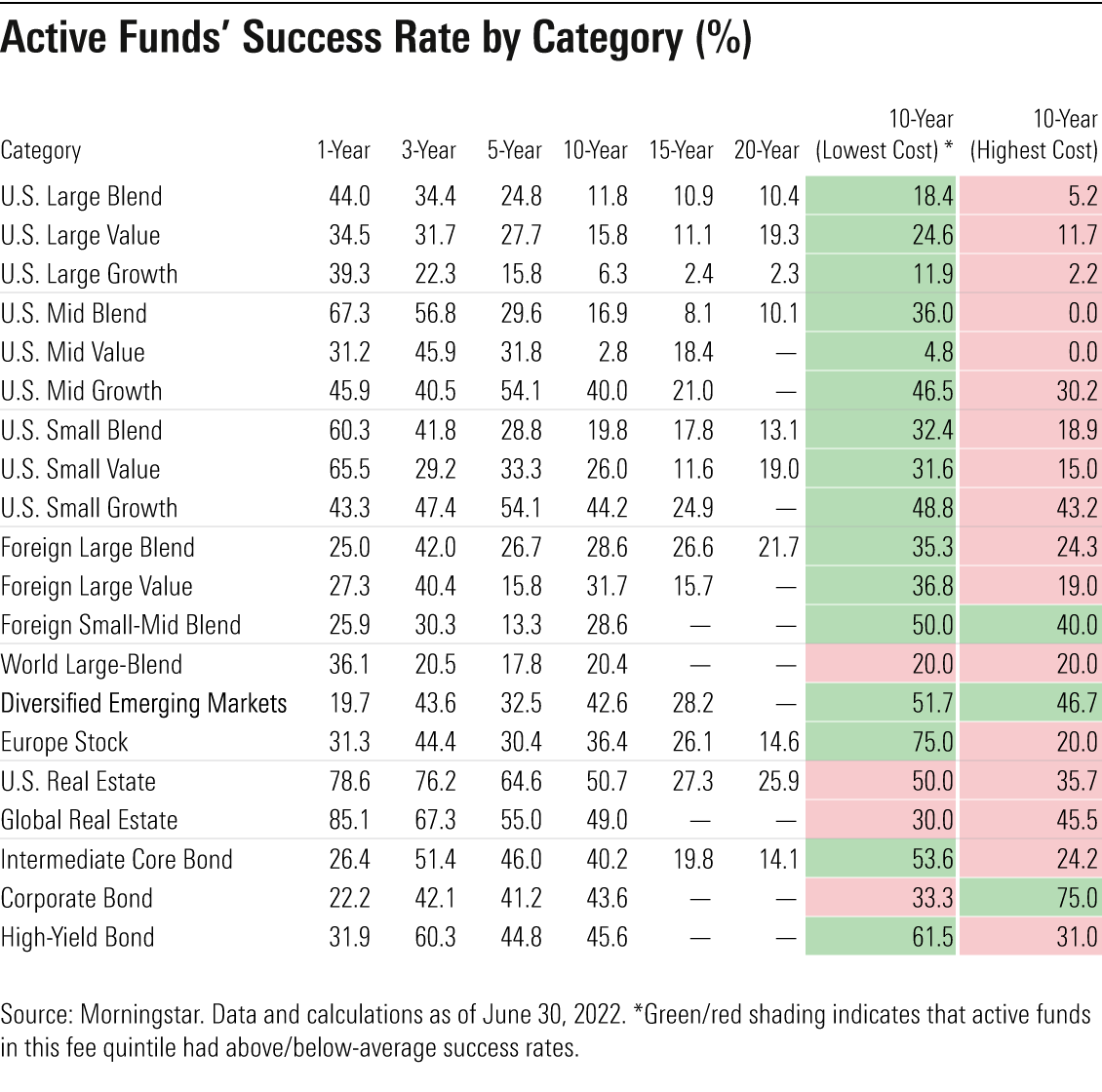

We know there are 10-bagger stocks and market-beating active funds to be had. But it’s also true that few if any of us will have the foresight to invest in them beforehand when it counts. Why? There are far fewer of these opportunities than one would think. Indeed, research has found that nearly all stocks and most fund managers underperform their indexes over longer time horizons.

Those long odds notwithstanding, some of us will press on anyway, believing we can zip from one outperforming security to the next before trouble sets in. Yet, higher costs and tax consequences are likely to bog down any excess returns we’re improbably able to eke out.

Indexing offers no more than the market return before fees, and in that sense it’s truly average. But when “average” handily exceeds what nearly all of us can reasonably expect to earn from active management after fees and taxes, it’s a no-brainer.

Yield Versus Total Return

In an ideal world, we’d own a basket of assets that throw off more than enough income to meet our needs and we’d reinvest the rest. This is especially enticing to retirees who are loath to dip into their savings to maintain their standard of living, instead seeking to offset spending with current investment income.

But for all its allure, investing for yield can be a trap. To obtain it, we might have to lock up our capital or subject ourselves to higher risk of loss from default, prepayment, or interest-rate movements. Or we might find the yield has been cranked higher through use of leverage, which risks big losses in the event borrowing costs rise or the underlying investments sell off.

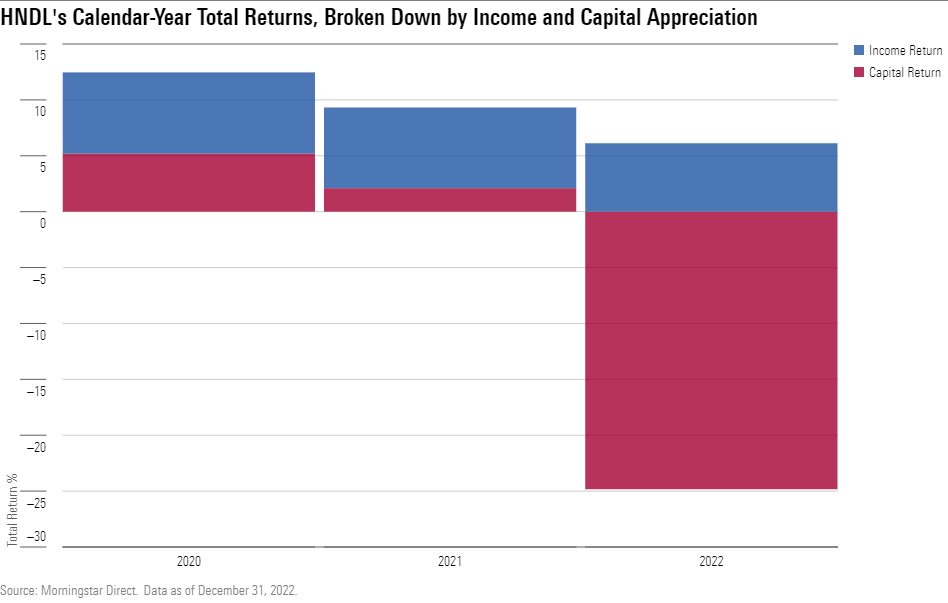

A case in point is an exchange-traded fund called Strategy Shares Nasdaq 7Handl ETF HNDL, which aims to maintain a 7% annual yield by investing in a mix of stocks and bonds while employing generous dollops of leverage. The ETF has more or less made good on delivering the yield advertised (albeit with some returns of capital sprinkled in along the way), but it also experienced wrenching downturns along the way, the downside of using borrowed money to goose its income payouts.

Investing for total return, in contrast, allows us to achieve a healthier balance of risk and return. We can pair income-producing assets like bonds with stocks, thereby lessening our exposure to credit and interest-rate risk and unlocking potential upside through capital appreciation. This can also boast greater tax efficiency, as less of the return stream is taxed at ordinary income tax rates, capital gains can be deferred, and there are opportunities to harvest losses to offset income and gains.

Building Versus Buying

It can be appealing to build a portfolio brick by brick: some stocks here, some bond ETFs there, and perhaps an alternatives strategy or two on the side for good measure. We’re our own architect and contractor, constructing our well-laid plans.

For some this approach will work just fine, provided there are clear guidelines around the roles these different holdings play and we avoid tinkering or otherwise straying from the plan. For many others, though, it’s the investing equivalent of too clever by half: a theoretically cohesive portfolio whose complexity drives us to distraction and ultimately leads to bad choices that foil our plans.

For those prone to distraction or who simply don’t have the time, it’s often better to buy than build: Invest in a single diversified holding like a target-date or target-risk fund. These strategies are no less diversified than a portfolio that’s been built one holding at a time. But with fewer moving parts, they’re less likely to jangle nerves. And given their mechanized rebalancing, these funds allow us to sit back and watch, so long as they continue to fit with our plans.

Conclusion

Investing can be confounding because it doesn’t bend to our will the way the world at large might. Try as we might to invest in the best stocks or funds, or build a portfolio that exquisitely balances risk and reward, the end product might be something we can’t succeed with.

Investors are usually better off keeping things simple and within their control, by saving, widely diversifying, and keeping costs low, while regularly rebalancing and focusing on total return—not yield alone. The approach isn’t theoretically perfect, but the reality of investing is that theoretical perfection is usually unattainable or more trouble than it’s worth. The perfect investment plan is the one that’s good in practice.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GQNJPRNPINBIJGIQBSKECS3VNQ.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/550ce300-3ec1-4055-a24a-ba3a0b7abbdf.png)