5 Most Overvalued Stocks Right Now

You may want to check your portfolio for these overpriced names.

Stocks may still be in the throes of a bear market, but there are still overpriced names for investors to be wary of.

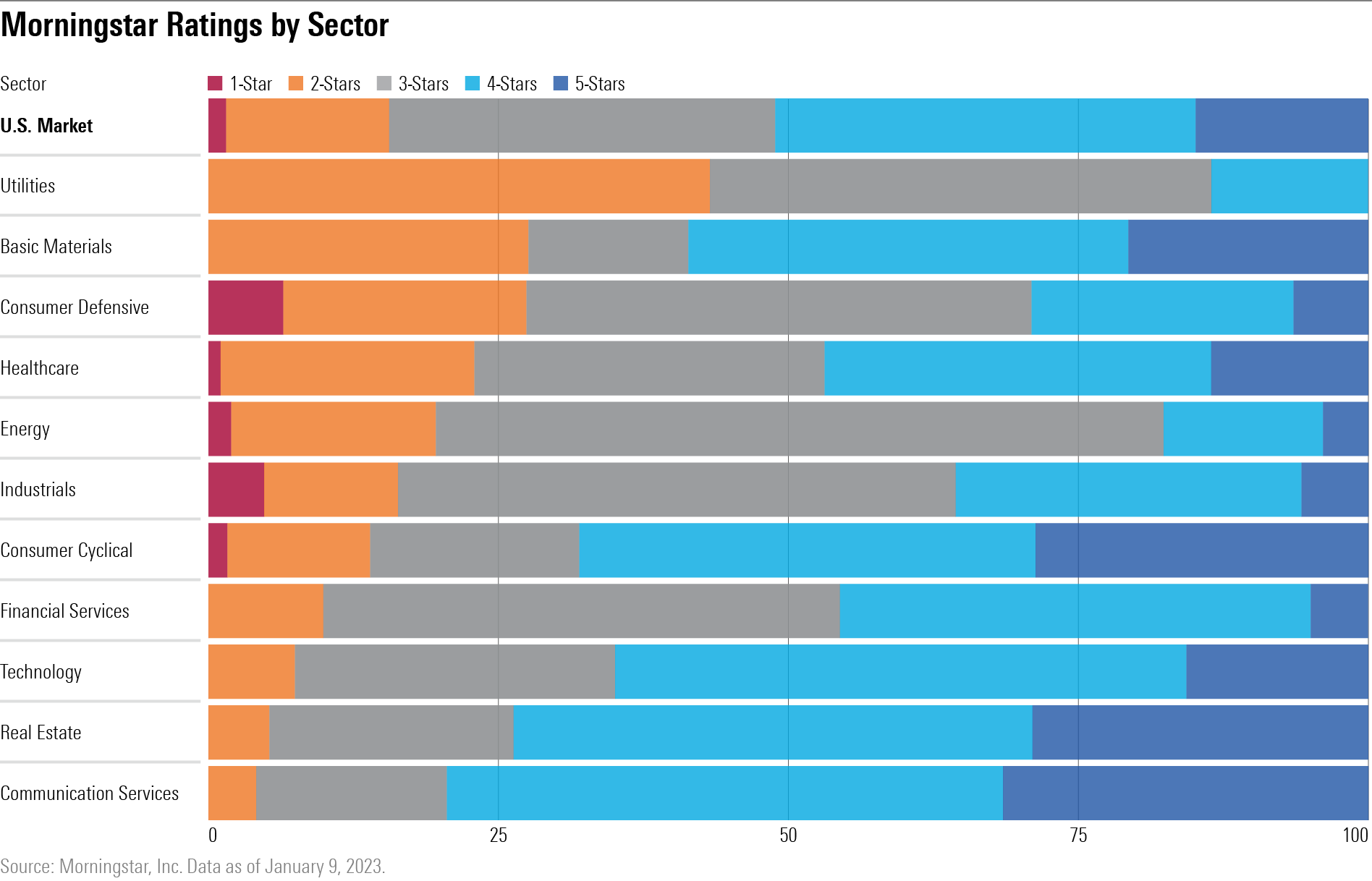

As of Jan. 9, 2023, 15%, or 130, of the 847 U.S.-listed stocks covered by Morningstar analysts are considered overvalued, having a Morningstar Rating of either 1 or 2 stars. A year ago about 30%, or 253 stocks, were overvalued compared with the fair value estimate set by Morningstar stock analysts.

In certain sectors, overvalued stocks are widespread, such as in utilities, where 46% of Morningstar’s coverage is overvalued, and another 43% at fair value. In other sectors, such as communication services and real estate, expensive stocks are much scarcer, with only 4% of communication services stocks considered expensive, and 5% of real estate.

To identify the most overpriced stocks covered by Morningstar, we ran a simple screen that sorted all 847 U.S.-listed stocks by their price/fair value ratio, a data point that divides a stock’s price with its Morningstar fair value estimate. Stocks with ratios that are greater than 1.0 are typically viewed as overvalued, while those under 1.0 are undervalued. The five most overvalued names on our U.S.-listed coverage list are:

Below, we highlight Morningstar analyst’s reasons for why they think these stocks are way too expensive. A list of the top 10 most overvalued stocks overall can be found at the end of this article.

TAL Education Group

- Morningstar Rating: 2 Stars

- Price/Fair Value Ratio: 1.65

After suffering harrowing losses due to Chinese regulations that restricted for-profit academic tutoring in the country during 2021, Chinese private education services provider TAL Education Group saw its shares surge and become one of the best-performing stocks of 2022. Cheng Wang, a Morningstar equity analyst, says the rally was driven by, “investor speculation of a policy reversal on K-9 academic after-school tutoring given the Chinese government reversed course on the real estate sector and loosened regulation on the tech sector.”

That rally took TAL Education from being one of the most undervalued stocks at the start of 2022 to now one of the most overvalued stocks of 2023, trading at a 65% premium to its $5.60 fair value estimate.

Wang thinks that the hoped-for tailwinds from a potential pivot in China’s after school tutoring policies may be unfounded. Although Wang believes that China’s regulatory environment will be more friendly to private education providers due to the government’s switch to an economic growth mentality, he thinks policies against for-profit K-9 academic tutoring are unlikely to be loosened as regulations in the technology and real estate sectors have been. “After-school tutoring is far less important than real estate to China’s economy,” he says.

Additionally, TAL Education has already transformed its business to focus on nonacademic tutoring, learning content, and learning technology, and has spun off its K-9 academic tutoring business. “Even if there is any regulatory ease, TAL will not benefit, unless the government allows the business to be for-profit again.”

Hess

- Morningstar Rating: 1 Star

- Price/Fair Value Ratio: 1.64

Oil and gas producer Hess’s stock nearly doubled in 2022, rising 94.1%. Higher oil prices helped improve operating margins to 33.1% during the third quarter of 2022, up from 22.8% for the same period a year earlier. Investors also cheered the firm’s efforts to reduce costs, which contributed to widening margins.

“Hess has done an exceptional job transforming the portfolio in the last few years, pivoting to low-cost resources in the Bakken and Guyana that garnered it a narrow moat rating in March 2021. These assets give Hess the potential to deliver robust capital returns in tandem with significant growth,” says David Meats, Morningstar’s director of equity research, energy and utilities.

Still, despite the company’s noteworthy performance, Meats still believes that the oil and gas producer is one of the most overvalued firms on Morningstar’s coverage list, trading at a 64% premium to his $88 fair value estimate.

“We think the good news is already priced in. In addition, the market apparently has rosier views on long-term commodity prices than we do. We agree that prices will remain elevated at least through 2023, but our long-term forecast for crude is still $60 per barrel [for] Brent. Even though the futures strip is backwardated [prices for oil futures are generally lower than recent oil market prices.], it does not fall below $70 by 2030,” he says.

Dick’s Sporting Goods

- Morningstar Rating: 2 Stars

- Price/Fair Value Ratio: 1.57

Dick’s Sporting Goods shares trade at a 57% premium to its $82 fair value estimate. The sporting goods retailer has undergone growth that Morningstar senior equity analyst David Swartz views as “anomalous.” Operating margins have more than doubled to 16.5% for the fiscal year ending in January 2022, from 7.7% in 2021.

“Although its sales have been very strong over the past two years, we believe a slowdown is likely, as growth in sporting goods retail has generally been minimal due to external competition,” says Swartz. Operating margins have already started to trend downward, falling to a trailing 12-month value of 13.4% as of Oct. 31, 2022.

“Moreover, inventories across the activewear industry remain high, which could necessitate more markdowns than presently assumed,” he says. Markdowns would continue to pressure margins.

Old Dominion Freight Line

- Morningstar Rating: 1 Star

- Price/Fair Value Ratio: 1.52

Old Dominion Freight Line is a less-than-truckload, or LTL carrier, that Matthew Young, a Morningstar senior equity analyst, sees as “the clear industry leader in terms of execution, freight selection, and service quality.” The company is also, “materially more profitable than any of its publicly traded peers.” As a result, it tends to trade at a meaningful premium compared with competitors.

Broadly, stock prices for trucking companies have started to ease off in recent months as expectations for freight demand and pricing softened. Still, Old Dominion Freight Line’s stock remains one of the most overvalued in Morningstar’s U.S.-listed coverage list, at a premium of 52% to its $201 fair value estimate.

“I suspect the market is differing with us in terms of our midcycle margin forecast. We take a more conservative stance, not because of execution but because LTL shipping is a cyclical, price competitive business,” says Young.

Cintas

- Morningstar Rating: 1 Star

- Price/Fair Value Ratio: 1.51

Shares of the dominant provider of uniform rentals and sales in the U.S., Cintas, are about 51% overvalued relative to its $292 fair value estimate, according to Morningstar senior equity analyst Joshua Aguilar. While the company has been reporting strong results, with revenue having grown 10.4% during fiscal 2022 and operating margins inching up to 20.2% from 19.5% in 2021, Aguilar expects recessionary pressures and energy costs to hinder the firm’s growth. “Around 40% of Cintas’ energy expense goes toward natural gas and electricity, of which the prices are rising,” he says.

Competition is also starting to grow. “Cintas has claimed that its products and services are of higher quality, but we continue to be skeptical that its offerings are indeed `better enough’ to outcompete other industry players.”

A recession could also potentially hurt the company’s performance, which Aguilar considers “highly cyclical” due to their core uniform services business being directly tied to U.S. employment trends.

During an earnings call, “management stated with confidence that Cintas has been able to attract new business clients during historical recessions because the value it provides to customers remains strong. However, we do not share the same optimism considering the uncertainties with the length, degree, and aftereffects of a potential recession in the U.S. and the global economy,” Aguilar says.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T5MECJUE65CADONYJ7GARN2A3E.jpeg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/VUWQI723Q5E43P5QRTRHGLJ7TI.png)

/d10o6nnig0wrdw.cloudfront.net/04-22-2024/t_ffc6e675543a4913a5312be02f5c571a_name_file_960x540_1600_v4_.jpg)